Oil Tankers Already Sailing Into The Sunset Of Peak Oil Demand

Support CleanTechnica's work through a Substack subscription or on Stripe.

A global shipping logistics contact, Steven De Jaeger of Remant Transport Architects, reached out to share a very interesting data point and article with me. It seems no one is ordering new oil tankers these days.

“The numbers are stunning. The ratio of crude tanker capacity on order to crude tanker capacity in service is now down to an all-time low of 2.7%, according to Clarksons Securities.

“For very large crude carriers (VLCCs; tankers that carry 2 million barrels of crude), it’s a mere 1.7%. VLCCs are vital for transport of crude exports from the U.S. Gulf and the Middle East. There will be 910 VLCCs of all ages on the water by the end of this year. The number of new VLCCs to be delivered in 2024? Zero. The number to be delivered in 2025? One.

“The situation is almost as severe on the product tanker side. The orderbook-to-fleet ratio for product tankers is down to just 6.1%.”

The claims made in the article are interesting, but there are a lot of what appear to be excuses surrounding the primary cause, which is that peak oil demand is coming likely later this decade and so buying a 25-year lifespan capital asset is likely to lead to it being stranded. In the case of oil tankers, literally stranded, not just fiscally as will be the case with the Trans Mountain Pipeline tripling.

For context, Norwegian oil giant Equinor, fossil-fuel heavy consultancy McKinsey, and the International Energy Agency have all published scenarios that include peak oil demand between 2025 and 2030, with a combination of COVID-19 and the European energy crisis accelerating the shift away from a high-carbon economy. Peak coal was 2013, with a return to those levels briefly in the 2022 energy crisis. Peak natural gas I project as likely around 2035.

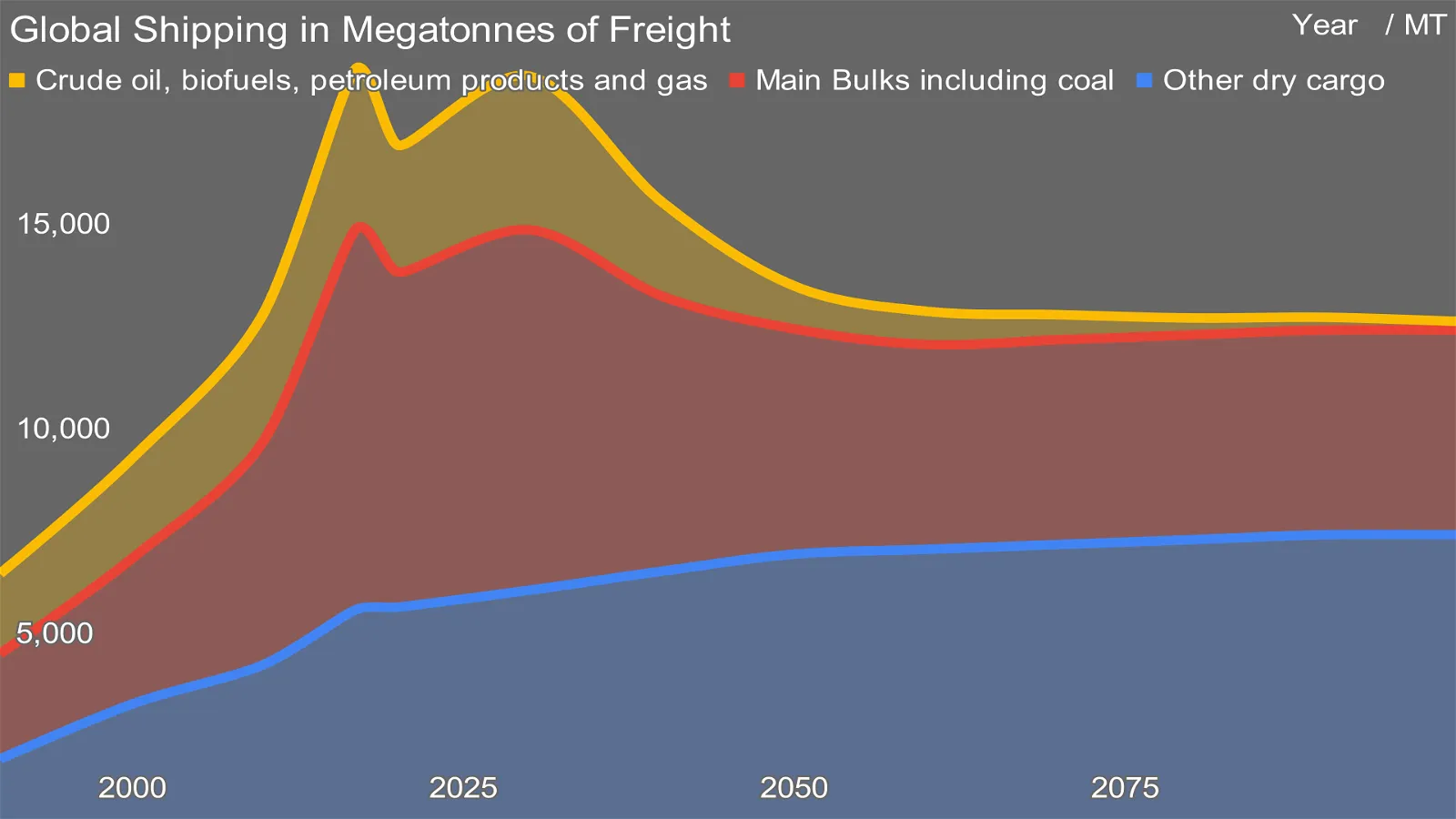

In my maritime shipping projections of tonnage, energy requirements, refueling with batteries and biofuels, and related carbon curves, this results in a return to roughly 2017 levels by 2030, about 3,000 megatonnes of oil and gas, then a decline by a third each decade through 2050, followed by a slower decline to roughly 200 megatonnes in 2090 and 2100. 40% of bulk shipping is coal, oil, and gas, and that’s mostly going away. Another 15% is raw iron ore and that’s going to diminish with more scrapping and more local processing. As always, through a glass darkly, big error bars, etc.

This isn’t exactly a difficult projection to make, although the oil and gas industry doesn’t want to talk about it, the IEA has challenges with it, the US EIA has similar challenges with it, and the maritime shipping industry has been pretending it’s not going to occur. Many are pretending that peak oil demand will result in a decades-long plateau, but that’s wishful thinking. Why?

80% of fuel demand is for ground transportation, and that’s all going to electrify. That’s low-hanging fruit. As I published recently, India is at 83% heavy rail electrification with a target of 100% within years. China is at 72% and climbing. Europe is at 60% and climbing. China’s 600,000 electric buses and 500,000 electric trucks make it clear that all but niches of off-road will be electric. Pipelines will see dwindling crude, gas, and diesel loads, with bankruptcies and consolidation, done strategically and well in some jurisdictions, and badly with fuel shortages in others.

Western countries’ new car sales are dropping, not rising. In a recent review of the statistics, I saw only one country, Germany, with any rise at all year over year, and that was 1%. Asian purchases are rising, especially in China, but China is already buying well over 60% of plug-in vehicles annually. Electric airplanes and electric ships will eat into fuel requirements for those segments steadily over the next 30 years, and biofuels will eat most of the rest.

One of the excuses made in the article for the empty order book is that dual-fuel ships are expensive and no one knows what will end up being the replacement. I am of the opinion that batteries and biodiesel that’s plug compatible with today’s engines will dominate. Maersk and the global methanol industry are betting on green methanol, which I think is a pretty poor idea for cost comparisons to biofuels, dual bunkering logistics in ports, 2.2x tank sizes in ships, and higher health concerns. Green ammonia is other organizations’ preference, but that has mostly worse challenges than methanol and much higher health risks.

The Global Center for Maritime Decarbonization is running big projects to test safe ammonia bunkering, on-ship carbon capture and biofuel sourcing and bunkering. As I said to Lynn Loo, CEO of the organization recently, it’s great that the work is being done, as concrete results showing that ammonia and shipboard carbon capture aren’t viable will shut down those faint hope pathways more effectively than people like me pointing out the obvious, and sourcing and validating biofuels requires back tracing supplies that needs to be operationalized.

So there’s truth to the shipping industry’s complaint about lack of certainty. But the real issue is stranded assets. No one is willing to sign long-term contracts for crude deliveries to guarantee paying off the ships in seven or eight years of service because everyone is staring at the cliff’s edge.

Big ships these days are $60-$120 million. They have lifespans of 20-25 years. There are already 910 very large crude carriers (VLCC) plying the waters and canals carrying crude, and many of them could be extended for a few years of extra life. And new ships are going to get more expensive.

Regardless of potentially $15 million more, over 10%, for dual-fuel engines and on board fuel storage, an unlikely requirement in my opinion, there’s a different issue at work. In the past several days I’ve published a new decarbonization projection, global steel demand, supply technologies, and carbon emissions through 2100. There’s a good news story there, including a massive rise of scrapping of steel we’ve already made to 75% globally, along with proven technologies for decarbonization. Scrap steel with electric arc furnace minimills powered by renewable electricity won’t be more expensive, but new steel from direct reduction using green hydrogen, biomethane, and renewable electricity likely will be.

And big ships use a lot of steel. A VLCC uses about 40,000 tons of steel, and there are 910 of them. That’s 36.4 million tons of future scrap steel right there, or about 40% of the steel the US uses in a year. Less than US pipelines it turns out, which have four years of steel for the country if scrapped. And that’s just one category of ship. Ships have become more expensive to build in recent years, and a rise in the cost of steel is a large factor in that.

Steel prices going up. Oil futures at risk. No idea what fuel combinations to buy engines and tanks for. Risky bets on fuels costing $15 million per ship. It’s a bit of a perfect storm, and it’s sinking the order books of maritime shipping industry, at least for this category of ship. The major shipyards of the world are full of container and LNG ships, and a growing number of electric retrofits and new builds, so it’s not hurting them yet, but it will be.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy