Dismissal Of Methanol As Marine Fuel Leads To Pushback

Support CleanTechnica's work through a Substack subscription or on Stripe.

A few days ago I assessed Methanex’ claims that its methanol-fueled sailing across the Atlantic was carbon-neutral. My opinion after looking at what they were doing? Greenwashing. But a couple of challenges have emerged to my thesis dismissing methanol entirely as a replacement marine fuel, and one of them was even polite and informative.

As a reminder about the Methanex claims, the company had sourced perhaps 5% methane from biological sources which they asserted would have otherwise been vented to the atmosphere, mixed it with 95% natural gas, and then ran it through their normal methanol manufacturing process. That’s steam reformation to create a synthetic gas which they distill into methanol. Anything which burns 95% natural gas is not climate neutral, and expanding biomethane anaerobic digestion is a poor idea from a climate perspective, so I gave this effort a negative assessment.

Further, I asserted that methanol wasn’t a great marine fuel, as normal methanol costs about twice what diesel would cost, takes up over twice the volume for the same distance reducing cargo capacity, and had virtually the same carbon emissions as diesel when independent CO2e numbers for methanol were used and the more than doubling of fuel was factored in. When we consider synthetic methanol, built up from hydrogen, oxygen, and carbon in well understood processes, it would be about four times as expensive and would be multiplying whatever the carbon debt of the electricity used by several multiples, a key problem with hydrogen and synthetic fuels.

So I scratched my head over Maersk’s preference for the fuel as well. That marine shipping giant has bought a bunch of dual-fuel ships and has sourced enough greenish methanol to power them for perhaps 1-2% of their annual sailings. The rest of the time they would run on the waste leftovers from crude oil refineries that aren’t used to pave roads. I haven’t assessed each of Maersk’s methanol sourcing agreements and processes to be more than suspicious that they likely have more of the shell game handwaving Methanex is using. Perhaps I’ll cast a jaundiced eye over each of Maersk’s purportedly green methanol acquisitions now that I know how odd the accounting can be.

The methanol for shipping assessment attracted attention. A general manager of global marine and ground-based power engine manufacturer Wärtsilä commented, not particularly civilly, on LinkedIn with various at least partially reasonable objections. The CEO of a purveyor of methanol for energy provided some useful and less useful objections, but very nicely. A decarbonization representative of Swedish ship manufacturer and operator firm Stena Sphere was appreciative of the science- and economics-based assessment. The CEO of the global methanol trade and lobbying association was understandably in disagreement, but less understandably uncivil in his comments (pro-tip for trade association heads: your job is PR and lobbying, not being rude on the internet to analysts). Methanex and its shipping subsidiary were silent, but perhaps as the 800-pound gorilla in the global methanol industry, they simply gave the lobbying association head his marching orders.

While my optimistic September assessment of the silver lining of the European energy crisis being a pivot to actually low carbon generation and HVDC interconnects for strategic energy interdependence had vastly more readership, about 500,000 last time I checked, it’s clear that the methanol piece attracted senior eyes despite perhaps a 20th of the readership in various forms.

Most of the arguments were trivially discounted. One person claimed that methanol was a viable shipping fuel because it had been used to cross the Atlantic, ignoring the environmental and economic feasibility and comparisons I’d made. People invested fiscally, emotionally, or both in hydrogen and synthetic fuels claimed I was biased against hydrogen and e-fuels, ignoring all of the physics, economics, and carbon workups I’ve published. Others claimed that all shipping fuel was toxic, so just don’t drink it, ignoring the organ damage that can result just from having it on your skin. Methanol is more of a human health concern than resid or diesel, although not nearly as bad as ammonia, and moving away from safer choices to less safe choices is typically a bad idea and fairly easily dismissed. Same same, as they say in Singapore.

But there were three points worth deeper assessment.

Air Pollution

The first I’ll buy out of the box, that methanol burns cleaner than diesel or resid. That’s true. It’s an alcohol and pure alcohols do burn cleaner than fossil fuels. There are three considerations here for me. The big one is that I’m projecting all inland and two-thirds of near shore shipping will move to battery-electric, only the longest journeys will requiring burning a fuel of some sort, that those journeys will diminish substantially due to the near elimination of bulk shipping of fossil fuels and reduction of raw iron ore shipping, and so pollutants from any marine fuel will be much less globally and much further from people. The second is that my preferred route, biofuels, also burn cleaner than fossil fuels, so it’s a continuum of pollution. As a result, without delving into this much more, I don’t consider it a significant advantage.

The Wärtsilä GM was the one who brought this up, and as I discussed with that firm’s global VP of energy storage and optimization, Andrew Tang, a while ago, about half of the firm’s business is onshore power generation units, so it’s understandable why the firm would be hoping to replace diesel with something else for that market. Sorry, Wärtsilä, your land-based power generation unit business is in for rocky times in the coming years. Tang’s business line will dominate your energy division instead, and your marine engine business is going to be hurting as well with electrification.

Cost Of Energy

The next point raised was a claim from the methanol lobbying CEO that I’d assumed the wrong baseline for price of methanol vs diesel. I’d looked over historical prices for both, not the weird ones in the past couple of years, and found that they were both roughly $1.80 per US gallon or $0.48 per liter on average. I’m comfortable that the sources I looked at were accurate, but to be clear, they were each single, comparable sources for the US, did not cover wholesale purchases by the metric ton and did not look at variances in different global markets. If my sources were too narrow and the geography was an outlier, then my cost assessment would be wrong.

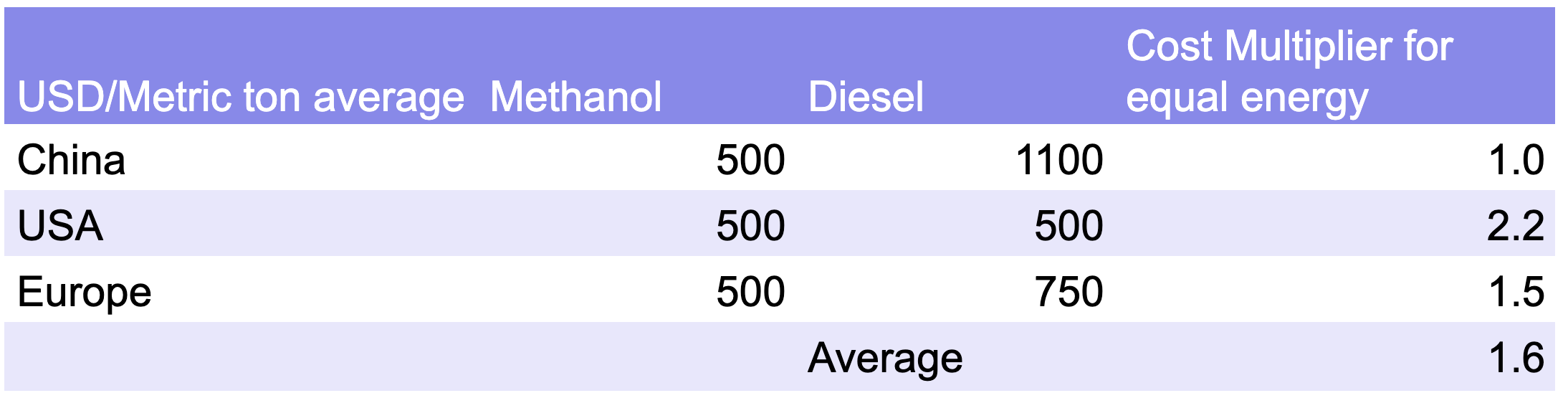

The comparison I’ve worked up is for contracted metric tons of methanol and diesel in three geographies: the US, Europe, and China. Spot market prices fluctuate and are typically cheaper, but bunkering ships requires hundreds of thousands of tons of fuel daily in major ports, so spot prices aren’t the appropriate measure. I’ve attempted to get an apples to apples comparison here, but it’s challenging across processed commodities, especially when one is always a fuel and the other is virtually always an industrial feedstock. As always, if this is an inappropriate assumption or you have better sources, let me know.

The best source for methanol prices in bulk I was able to find was from the Singapore consultancy MMSA. They showed average prices in North America, Europe, and China tracking one another at an average of about $500 per metric ton from 2001 to 2020. As virtually all methanol is made from natural gas, the price unsurprisingly spiked in the fall of 2022 with the global natural gas price spike.

As I have pointed out a few times, natural gas prices have moved from being stable and low-cost from the early 2000s to roughly 2020 to climbing above the rate of inflation and being more volatile, as the shale oil and fracking revolutions have become challenged by overly debt-laden business models and global oil price wars aimed at higher priced unconventional extraction such as shale oil, which typically comes with a benefit of marketable natural gas. Expect methanol prices to rise above the level of inflation on average, and be spikier as a result.

There was no comparable source for diesel, and so multiple sources were aggregated. EIA data has the US average wholesale price of diesel at $500 per ton, close to identical to methanol, as my original assessment had reported. Assembling data from a couple of sources (current, 2018-2019, 2017) for China suggests a wholesale price of diesel of about $1,100 per ton on average over the past several years. Various sources (one, two, three) suggest the European average bulk price per metric ton is around $750.

As a note, this is an interesting counter-point to China’s 40% purchasing power parity advantage over Europe and the US, something I was discussing in a dialogue with Tsinghua University in Beijing’s PBC School of Finance recently. It might be a driver of China’s significant advantage over those geographies, but especially the US, in road and rail electrification.

My original assessment used US prices, and clearly at bulk the ratio remains the same. The cost per unit of energy is 2.2 times higher with methanol, as noted. For Europe, the spread is lower, so it would only cost, on average, 1.5 times as much to fuel a ship with methanol as with diesel. China was an interesting outlier. It’s unclear why its diesel is so much more expensive on average in bulk than in Europe or the US, but triangulating as best I could within that always data-opaque country, it appears that there would be cost parity for unabated methanol and diesel.

Note that these prices are for the ‘best’ diesel typically, lower sulphur, cleaner burning variants suitable for use near humans. But most maritime shipping runs on resid, the cheap and dirty waste from refining crude oil after everything of higher value is fractioned off. It’s basically liquid asphalt. Replacing resid is economically challenging for any alternative, but as this shows, methanol is going to be more costly regardless in most places.

So that challenge was worth digging into. What it shows is that with fossil-sourced methanol, there is no price advantage in any market over diesel, so no economic reason to switch. As I pointed out, fossil-sourced methanol would still emit 97% of CO2e as diesel, so there’s no merit in switching there. It’s more toxic, so that’s a strike against it. And its advantages in terms of air pollution diminish with battery electrification of almost everything near people and diminishing of longer haul shipping.

While the cost variance wasn’t as high globally as I’d expected, this was a useful exercise in comparing bulk potential energy sources globally, so at least for that I can thank the CEO of the methanol lobbying association, if for nothing else including the lack of civil interactions.

Biosourced Methanol

The other challenge worth considering is biological pathways to methanol. I had a suspicion going in that all pathways would lead through high global warming potential biomethane, and it seems that suspicion was well-founded.

The first pathway is one I’d already looked at, Methanex’ claim of using biologically sourced methane in its standard methanol manufacturing process, albeit at such homeopathic dilutions that made it complete greenwashing. There are multiple sources of biomethane, and there’s a great hope on the part of the natural gas industry that they’ll be considered a suitable replacement for fossil methane, but I’m opposed to expansion of this market.

Methane emissions occur due to our human economic systems in a few places. Unsurprisingly, fossil fuels are the big problem and eliminating their use except for industrial feedstocks that aren’t burned is job one. As a note, blue and black hydrogen from coal and natural gas would perpetuate these methane emissions, a key problem. As a second note, the percentage from natural gas is undoubtedly low-balled in this, as the past three years has seen a litany of reports and studies showing much greater leakage in the US and indeed around the world from natural gas than was historically understood.

Cattle, goats, sheep, and buffalo have gut microbes that break down the vegetation they eat and release methane. That methane vents to the atmosphere when the animals belch. That’s a problem that is not reasonable to try to capture. It’s far too diffuse. Minimizing emissions is the reasonable strategy there, and there are multiple dietary supplements and strategies that will assist with that. It’s also worth noting that while we have a lot of these animals domesticated globally, there used to be vast wild herds of many of them prior to our involvement. Determining the variances is difficult. At one point I calculated that there were only three times as many cattle in the US in modern times as bison and other ungulates in historical times prior to our arrival, but other calculations show greater numbers. Calls to reduce meat consumption from these sources are reasonable to understand, but fail one of my basic filters for solutions, in that it would require human nature to change globally. We’re going to be stuck with some of this going forward.

Manure management is another significant source aligned with belching livestock. Piles of cattle manure and ponds of pig manure decompose anaerobically — without the presence of oxygen — to create methane as well. Free range cattle manure also decomposes in part this way, but there’s a lot more oxygen for aerobic decomposition that creates carbon-neutral CO2 instead as well, so it’s lower as a ratio.

There’s a bunch of work being done to maximize the production of methane from manure. That’s right, to maximize it. There’s a type of technology called an anaerobic digester. Put animal manure or other waste biomass into it, and it eliminates oxygen from getting at it, so the only form of digestion is anaerobic, and the gas that comes out is very high global warming potential methane.

More creation of biomethane through this route is, in my opinion, a really bad idea. There are processes which go directly from anaerobic decomposition to make liquid fuels without leakage which are better. A well designed, and well operated biological process that collects biomass and feeds it through a sealed industrial system that produces biologically sourced methanol could be a reasonable choice.

The global market is currently 170 million tons of methanol, and job one is to decarbonize that, not create a new methanol market where none exists. As I pointed out in the initial article, CO2e emissions from current methanol manufacturing are in the range of a quarter of a billion tons annually, which is significant. A virtuous and tightly sealed biomethanol pathway that pushed animal dung through to liquid methanol for industrial use would be a good pathway.

But, of course, pathways that go directly to biodiesel and biokerosene, higher energy density fuels that are plug compatible with the entire maritime and aviation fuel industries, exist today. Requiring capital expenditures for lower energy density, equal CO2e, more expensive, more toxic fuels seems to be contraindicated.

Landfills are another big source of anthropogenic methane. Pile a bunch of stuff including a lot of biomass in a pit and cover it over, and that results in anaerobic decomposition. That’s a concern, and there are three pathways to deal with it. The first is to stop putting biomass in landfills, and instead divert it to composting and biomass feedstocks for low-carbon processes like biodiesel and biokerosene. The second is to burn it locally, preferably in smaller power generation units. Converting the methane to CO2 reduces its global warming impact by 29-86 times, and generates useful electricity. The vast majority of methane from landfills is from biomass that’s modern, not fossil fuels, so converting the methane back to CO2 is much closer to carbon neutral. Third, just flaring it off, burning it without doing anything else, would be better, but flaring data shows that the amount of methane converted to CO2 is much lower than historical estimates.

And fourth, it’s reasonable at first blush to assume that putting a methanol manufacturing plant on a big landfill has a reasonable pathway to decarbonize part of the methanol supply. It’s worth noting that a ton of methanol requires 0.6-0.7 tons of methane, so that 170 million tons annual supply requires about 110 million tons of methane. Contextually, US landfills produce about 4 million tons of methane annually, and it’s a very high waste society. A single modern, high-efficiency methanol plant requires about 3,000 metric tons of methane a day, or about a million metric tons every year, a quarter of the US total. There are over 1,200 big landfills in the US, so none of them come close to fulfilling the needs of a single high-efficiency methanol plant. Methane emissions from landfill would have to be collected through a diffuse and permeable set of collection devices to aggregate enough of it to warrant efficient biomethanol production. Replacing one set of dense sources of methane and a high-efficiency distribution system that leaks with a brand new set of tiny, inefficient and undoubtedly leaky pipes and collectors is not a solution.

Landfill methane should be diminishing annually as a problem and or resource, depending on how you look at it, and that’s what US data shows. And while biomass fermentation pathways to biofuels does produce CO2, it’s obviously a fraction of the global warming concerns of methane.

My strong preference is to eliminate anthropogenic methane emissions as much as possible, and to use or downgrade the GWP of the rest. Making biomethane a shipping fuel would be going in the opposite direction. As I noted in my original assessment, even with electrification of much of shipping and decline in bulk shipping, if methanol were the shipping fuel of choice, then methanol volumes would triple annually, hence the global lobbying group and Methanex’ interest in having that come true.

Any energy pathway that goes through methane is likely a global warming emissions leakage problem, but there’s another problem with it as well. Up through 2022, biomethane was twice as expensive as natural gas. As methane is the primary cost driver for methanol, doubling the cost of the primary input jacks the price of methanol up as well.

Non-Methane Gas Pathways

There are non-methane pathways to methanol. A civil commenter pointed out Enerkem’s process. It takes mixed solid, plastic, and biomass waste and puts it through a proprietary thermochemical process that produces syngas, ethanol, and methanol. The proprietary nature of the technology makes it hard to assess, but Paul Martin is strongly dismissive of this category of technologies, pointing out that the vast majority of units of energy from them are from plastics made from fossil fuels. As a reminder, this type of chemical engineering plant is exactly what Martin has been designing and building for clients for 30 years: he is an expert in this field. Making fossil fuels into plastics and then turning waste plastics into methanol to burn in marine shipping is not a virtuous cycle. It’s unclear what the price point is for this methanol, but at least one claim is that since dumpers have to pay to put garbage in landfills, the feedstock is essentially free.

Another approach the same commenter pointed to is power and biomass to X (PBtX) technologies. But as the linked meta-analysis paper shows, in order to get significant economic value out of it, you have to electrolyze a bunch of water to create hydrogen to supplement the process, and with the optimistic assumptions still results in significantly more expensive methanol. Is this a viable pathway to decarbonize the existing quarter billion ton CO2e methanol climate problem? Possibly. Is it a pathway to tripling methanol volumes to fuel maritime shipping? Unlikely.

It’s worth noting one other thing about the above pathways to methanol: they aren’t used by the vast majority of methanol manufacturers. They manufacture methanol from natural gas with a steam reformation process powered by burning more natural gas to create syngas which is distilled into methanol. None of that is proprietary. Not much of it is useful in terms of creating actually low-carbon methanol. The methanol industry may greenwash itself with them, but it’s not embracing them.

As always, it was great to get pushback from informed people regarding my efforts. And as always, I took the challenges seriously and worked through the ramifications.

I remain unconvinced that methanol is worth considering as a shipping fuel compared to the alternatives. Its high-carbon price point remains above that of current fuels. Its lower-carbon alternatives are either greenwashing or much more expensive than other biofuels. Most of the processes for methanol still go through methane with its high global warming potential, and something which must be substantially diminished as job one, not maximized. Animal dung and other biomass waste can be converted into biodiesel as readily as into methanol and without a methane phase which increases risks of leaking. I am convinced that job one with methanol is to decarbonize existing uses before inventing new ones.

And so, I’m back to batteries and biofuels — but likely excluding biomethanol — as the marine shipping energy sources of the future.

UPDATE: We reached out to Wärtsilä with the following question, and their Corporate Communications department responded:

Q: Given that you are selling electric drivetrains for marine shipping and batteries for ground-based storage, what percentage of your revenues do you project from these actually low-carbon solutions in coming years?

A: Wärtsilä doesn’t give guidance on our revenues. Our strategic target is to achieve 5% annual organic growth and energy storage and power system optimisation solutions are one of the key drivers behind that growth.

Wärtsilä is leading the transition to 100% renewable energy systems — we are in the top three energy storage providers globally and deliver grid balancing power plants, hybrid solutions and optimisation technology to accelerate decarbonisation. We recently opened our Sustainable Technology Hub in Finland to expand our development of engines capable of running on sustainable fuels.

Our work in the maritime sector includes batteries and hybrid solutions, which play an important role in decarbonisation – as part of a flexible approach that includes technologies running on a range of low and zero carbon fuels. Battery and hybrid technologies can’t meet the power requirements of all vessels, particularly deep-sea shipping, given the size of batteries needed to produce sufficient power. In the foreseeable future, decarbonised shipping will require a range of technologies – with electrification working alongside new fuels.

Vessels on order today and over the next several years will likely rely on a multi-fuel solution. Green methanol, hydrogen, and ammonia, as well as sustainable biofuels and other synthetic fuels, and energy efficiency technologies, will all have roles to play in different segments and different regions. We’re working to enable customers to keep pace with technology – to maximise the value of these new fuels as quickly as possible, as well as clean technologies such as batteries.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy