World EV Sales Now Equal 17% Of World Auto Sales

Support CleanTechnica's work through a Substack subscription or on Stripe.

Global plugin vehicle registrations were up 23% in September 2023 compared to September 2022, rising to 1,291,00 units. That’s a new all-time record. In the end, plugins represented 17% share of the overall auto market (12% BEV share alone). The market share could have been even higher if the overall ICE market hadn’t also been recovering to pre-COVID levels…. It seems that economic crisis or not, people are still buying cars.

This means that the global automotive market is firmly in the Electric Disruption Zone*. Add the fact that plugless hybrids represented 12% of total automotive sales in September, and we have 29% of global registrations having some form of electrification! (*People have asked me what the “Electric Disruption Zone” is. Basically, it is the steepest part of the tech adoption S-curve. Between 10–20% and 80–90%, market share growth will accelerate, and then it will slow down on the way to 100%.)

Full electric vehicles (BEVs) represented 69% of plugin registrations in September, keeping the year-to-date tally at 70% share.

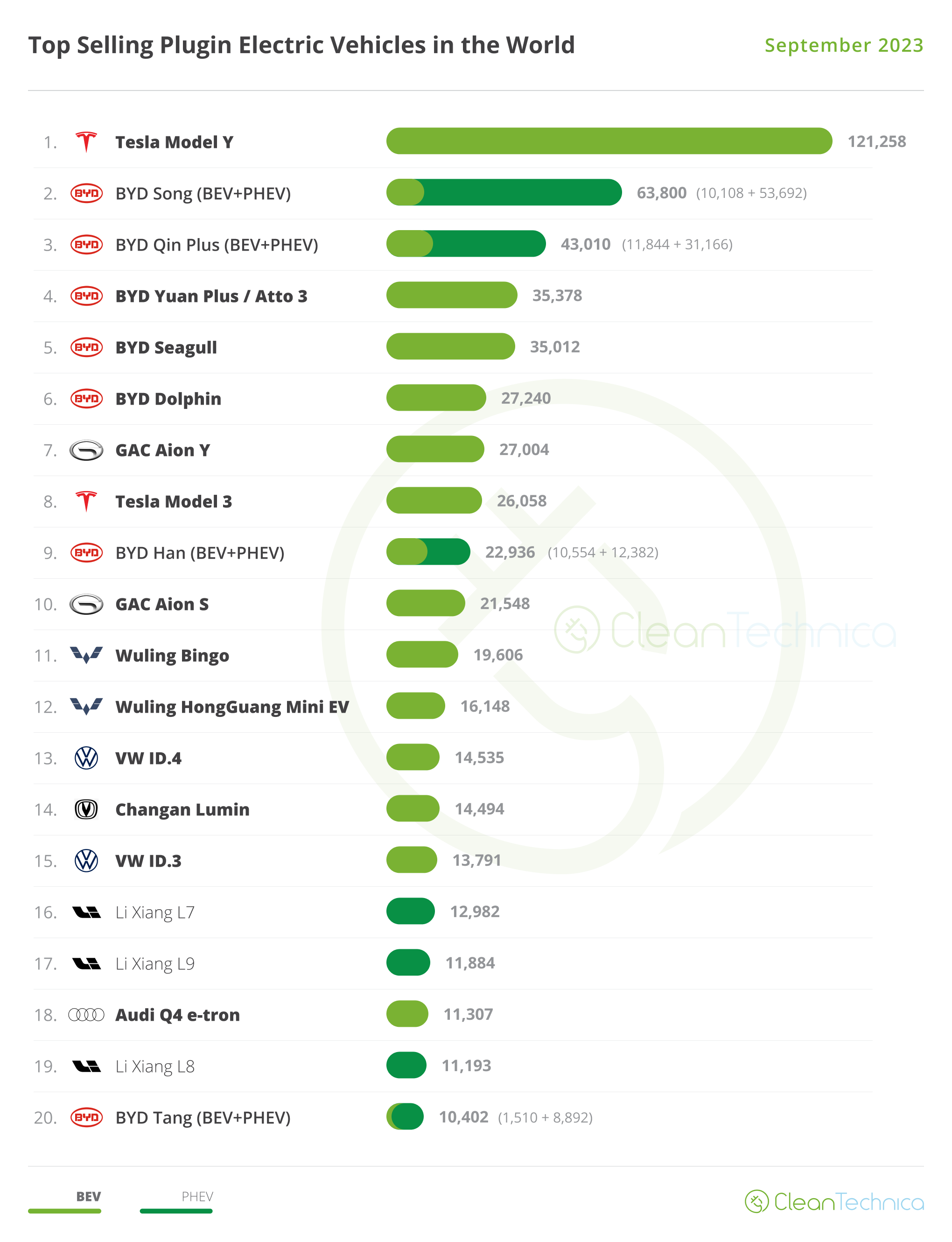

20 Best Selling EV Models in the World in September

Looking at September best sellers, there were no surprises at the top. The Tesla Model Y was high above everything else despite not hitting a record performance in September, which could mean two things — first, the peaks and valleys over the course of the quarter are being flattened, and second, we might be witnessing the first signs of flattening sales. It will be interesting to see how the next few months will fall out, and if the refreshed Model 3 sales recovery will affect its unrefreshed crossover sibling.

Behind it, with the Tesla Model 3 experiencing its worst month since July 2022 (just 26,058 registrations) due to the expected production change to the new refreshed model, we have a true BYD armada — 5 models coming from the Shenzhen make. Medal positions went to the usual suspects, with the Song in the runner-up spot and the Qin Plus closing the podium. An interesting note on the BEV version of the Qin Plus: the BEV version of the sedan is on its fifth record month in a row, with this record streak meaning that BYD is slowly tilting towards the BEV side, even in models where both powertrains are available.

Still on the top half of the table, we have a record performance to celebrate, and in this case, it wasn’t (thankfully) coming from either Tesla or BYD. The #7 GAC Aion Y had a record 27,004 registrations. It was the best selling NTNB (non-Tesla, non-BYD) on the table. The Aion Y even managed to outsell the #8 Tesla Model 3 and #9 BYD Han….

With its sedan stablemate GAC Aion S in #10, with 21,548 registrations, it looks like GAC is the only automaker that could run at the same pace as the top two. The Aion Y and the Aion S are in fact the best selling NTNBs on the table.

Elsewhere, the second half of the table saw two models hit record results. The #17 Li Xiang L9 scored its 2nd record in a row, 11,884 registrations, and the #18 Audi Q4 e-tron scored 11,307 registrations. Add the Audi’s record performance to the 13th position of the VW ID.4 and the 15th spot of the VW ID.3 and we have Volkswagen Group placing three models in the top 20 for the first time in … a long time. (See, Volkswagen — for the right price, people still love you.)

Outside the top 20, there is plenty to talk about. Going from biggest to smallest, the Chinese Porsche Zeekr 001 got 8,701 registrations, an encouraging sign for a model that should do a lot for the brand’s overseas plans in 2024.

BYD also launched a car in the full size category, for those who think the Han is too … classic/Mercedes-like/Grandpa’s car. The brand launched the Seal PHEV, essentially a Han PHEV with a more interesting design. With 7,444 registrations right in its landing month, the Shenzhen make could have another winner in its hands.

In the midsize category, the main highlight is the rise of Changan’s Deepal S7, the make’s take on the Tesla Model Y recipe. The Deepal S7 reached another record score, this time 10,244 registrations, in September. Could this new model become the brand’s best selling vehicle soon?

A mention goes out to the good scores of the Ford Mustang Mach-E (9,173 units), Geely Galaxy L7 (10,007 units), Leapmotor C11 (9,071 units), and BMW iX3 (7,04o units, a year best). Also, the XPeng G6 reached 8,132 units in only its 4th month on the market, so expect the startup’s take on the Model Y formula to start knocking on the door of the top 20 soon.

As for the compact category, we salute the record performance from the value for money king, the MG4. It scored 10,229 registrations this month. Still in this category, we salute the return to form from Great Wall’s Ora Good Cat, which got 9,915 registrations, the hatchback’s best result since December 2021.

Finally, in the tiny city EVs category, Geely’s take on the Wuling Mini EV, the similarly named Panda Mini EV, registered another five-digit result, 10,221 sales.

Top 20 EV Models YTD

In the year-to-date (YTD) table, the BYD Song profited from the Tesla Model 3’s skin change slowdown, gaining a precious advantage over it in the race for the 2nd position in the ranking. With October possibly still allowing some extra advantage, expect the Chinese SUV to stay in the runner-up position for a couple more months, but December will be a close call, as the Model 3 should have an extraordinary high tide in the last month of the year.

Below the podium, another point of interest for the last quarter of the year is around the 8th position. The Wuling Mini EV is now at a slower cruising speed, at around 15,000–20,000 units per month, and the #9 BYD Han and #10 GAC Aion Y have a real chance to surpass the diminutive EV. And considering the current strength of the Aion Y, it wouldn’t be surprising if the crossover-MPV ended the year in 8th, just below its Aion S sibling.

Things are even even more interesting in the lower half of the table. The BYD Seagull climbed another position, to #12, with the city model poised to join the top 10 by the end of the year — and maybe (who knows?) reach the 8th position.

A few positions below, the VW ID.3 was also up one spot, in this case to #16. The last positions on the table had a complete reshuffle, with Li Auto’s L7 jumping two positions to #18 while its 7-seat sibling, the Li Xiang L8, joined the table in #19. And in #20 we now have the Audi Q4 e-tron, which replaced the Volvo XC40 on the table.

In Q4, expect both of these Li Auto models to go after the #17 Denza D9, all while the German crossover does its best to resist the advances of Li Auto’s third Musketeer, the L9 Escalade, which is just 3,000 units below it.

Top Selling Brands

In September, BYD continued its never-ending record streak, thanks to a 273,000-unit performance. It was the 5th record in a row for the Shenzhen make. On the other hand, Tesla only delivered 154,000 units, a 19% drop YoY. This was the make’s worst drop since October 2019 (excluding the COVID-derived 26% drop of May 2020). Expect this to be just a bump in the road due to the Model 3 production changes, but the real test for both Tesla and BYD will be in 2024, as both should see their growth rates decrease significantly — for different reasons, but more on that later….

Below the top two galactics, GAC Aion again ended the month in 3rd, banking on its dynamic duo to stay ahead of the competition.

#9 Li Auto went from strength to strength, with yet another record month, its 6th in a row. Li Auto had over 36,000 registrations thanks to strong results across the lineup. With the startup brand still supply constrained, expect the high-end brand to continue beating records regularly in the remainder of the year. But the real fun will start when the midsized L6 SUV and L5 sedan land sometime next year. Oh, and the cherry on top of Li Auto’s cake is a certain bullet train Mega MPV … with mega specs.

Just below it, #10 SAIC also hit a record month, much thanks to the MG4, which scored its first five-digit month ever. The Shanghai-based OEM is compensating for a somewhat discreet career in its domestic market with a wide-ranging presence in overseas markets. It is the most successful Chinese OEM in export markets!

But one of the biggest surprises of the month was #16 Toyota(!), which had its second record result in a row(!!), this time 17,068 registrations. The company had strong results across its several operations (RAV4 & Prius in North America and Japan, BZ4X and RAV4 in Europe, BZ3 in China). Yep, Toyota is late to the game, but it is still too early to say the company is history….

Another OEM on a record streak is Leapmotor. Thanks to the success of its C11 SUV, Leapmotor scored its second record score in a row, 16,891 registrations. One can say that Stellantis has made a good choice, eh?

Another startup on the rise is #20 XPeng, which thanks to the G6’s success got 15,433 registrations, its best result since June 2022. Will XPeng’s take on the Tesla Model Y theme be the one that will save the company? One thing is certain — the crossover has a lot going for it.

Outside the top 20, the highlight was #21 Peugeot, with 14,470 registrations, thanks to the strong month of the Peugeot e-208.

In the YTD table, there isn’t much to report regarding the podium. BYD is well ahead of Tesla, and both are in a galaxy of their own. The two makes together are responsible for more than one third of the global plugin vehicle market.

This situation could change next year, as both should grow below the market average. Now, before people come with torches and pitchforks, let me explain:

BYD is reaching the natural limits in its home market, with the Shenzhen brand already #1 in its home market. Even if the Seagull provides a fraction more share, thanks to its incursion in the city car segment, the only way for BYD to grow is to start exporting in massive volumes, and that will only happen with local production. With BYD’s plants in Thailand and Brazil becoming operational in 2024, expect both to only hit their expected cruising speed of 150,000 units/year each in 2025, and with Europe sales limited by tariffs and logistic costs, I expect BYD to only export in large volumes by 2025 once Thailand and Brazil plants are fully operational. (And a European plant also may be starting around that time?)

Tesla has a different challenge, with the US brand already well established in the main global markets, its problem comes from the lack of fresh product. While the Cybertruck is expected to ramp up throughout 2024, that will be a model focused on North America, with a small contribution (100,000 units?) to the overall tally. So, what is left for the rest of the world is a lineup where the most recent model dates back to 2020. So the lineup is already in complete maturity, with both the Model Y and 3 close to their natural limits of consumer demand. And while Tesla will benefit from the global increase in EV share, and the refresh of both the Model 3 and Y could inject some freshness to the make’s best sellers, the truth is that Tesla will be, probably for the first time ever, more worried about not losing ground to its competitors than increasing the already large advantage it has over the competition. And while it could drop prices even further, the truth is that a) it doesn’t have as much margin as it had in the past, and b) that could destroy even further residual values, making leasing deals less interesting, and in the long run nullifying the effect of the price drop.

But back to September 2023. Far below these two, which are really in a league of their own, you have the hot GAC Aion, which has confirmed its status as the NTNB best seller. Don’t expect others to reach the Chinese make anytime soon. It seems this year’s podium is already decided: #1 BYD, #2 Tesla, #3 GAC Aion.

Elsewhere, the first half of the table does not have a lot to talk about, with the main point of interest being the 10th spot, where #10 Geely could be pressured in Q4 by a rising SAIC. SAIC climbed one spot in September, to #11, at the expense of Volvo.

The remaining highlights were #14 Kia closing in on #13 Hyundai, and Ford climbing to #17, surpassing Jeep in the race for best selling US legacy OEM.

Looking at registrations by OEM, leader BYD was comfortable at 21.9% share, up 0.1%, while Tesla was down by 0.4%, to 14% share.

3rd place is in the hands of Volkswagen Group (7.2%, down from 7.3%), which is keeping itself a good distance ahead of #4 Geely–Volvo (6.1%).

As for #5 SAIC (5.4%), the share drop stopped, for now. #6 Stellantis was also stable in September, at 4.6%.

Below the multinational conglomerate, things are more interesting. While #7 BMW Group (4.1% share) kept its position, Hyundai–Kia (also 4%, down from 4.1%) lost the 8th position to a rising GAC (4.1%, up 0.1%). Maybe BMW will be next in GAC’s list? Perhaps even in October?

Looking at where the ranking was a year ago, we can see that both of the top two brands gained share, 4.6% in the case of BYD and 0.7% in the case of Tesla. The other beneficiary was Geely–Volvo, which in the meantime surpassed SAIC and added 0.4% of share on the way.

On the losers side, Volkswagen lost 0.8% share YoY, while SAIC dropped almost a third of its share, from 7.6% a year ago to its current 5.4%.

Another interesting comparison is looking back at where we were in March of this year, or 6 months ago. From then to now, BYD seems to have slowed its gains, earning just an extra 0.6% share. This proves that the time of insane growth is coming to an end at the Shenzhen OEM. Tesla was a full 2.5% share above from where it is now, as Q1 was the period when the price cuts made the biggest effect on the careers of both the Model Y and Model 3.

In the same period, Volkswagen Group lost 0.2% share and SAIC 0.1%, which means that the Shanghai OEM seems to be stabilized around the 5.5% share mark. The same can be said about #4 Geely–Volvo, but in this case, it is around 6% share. #6 Stellantis continues to hover around the 4.6% share score. So, all of these three OEMs seem stable in this period of the EV transition.

Looking just at BEVs, Tesla remained in the lead with 20.1%, down from 20.6% in September. The US make has a comfortable lead over BYD (15.9%, up from 15.7%), making it unlikely the Chinese automaker will be able to remove Tesla from the BEV throne this year. The US automaker gained a precious advantage in the first half of the year. Next year, however … It isn’t much a question of “if,” but more of “when.” I do not expect it to happen in Q1, as the Chinese market will have new year festivities that will surely slow down BYD’s sales, but Q2 should probably signal the inflection point where BYD surpasses Tesla in the BEV race.

In the last place on the podium, Volkswagen Group (7.7%, down 0.1%) lost some ground over SAIC (7.5%). Expect an entertaining race between these two in the remainder of the year.

In 5th, GAC continues to grow (5.7%, up from 5.6% in August) — without much media attention, it is quickly becoming a force to be reckoned with.

Comparing BEVs to where they were a year ago, things roughly follow the trends in the PEV market — BYD (+4% share) and Tesla (+1.6%) were up, SAIC (-2.3%) was down, but in this case, Volkswagen Group instead of losing share actually gained 0.3% share YoY, which can only be explained by the fact that the German OEM is ditching PHEVs and becoming a more BEV-based company. Good for you, VW!

Finally, comparing the current picture with what happened 6 months ago, Tesla’s drop is even more evident (-3.5% share), and while BYD’s market gains are relevant (+1.2%), GAC’s market share grab (+1.1%) is definitely more impressive, as it starts from a much smaller base.

Finally, a few small notes on the state of the global EV market and the health of each of the major automotive blocs….

A healthy market is one where there aren’t monopolies, and diversity breeds innovation.

With the Chinese EV market owning over 50% of the total market, this is not a healthy situation, nor is the fact that the top two OEMs, BYD and Tesla, own 36% of the total market.

Looking at the Chinese EV industry, the fact is that the pace of innovation, not only regarding batteries, but also digitalization, costs. And the remaining aspects of a cars are unparalleled, even by Tesla.

Stellantis (Leap Motor), Volkswagen Group (XPeng, SAIC), Renault (Geely), and Mercedes (NIO) moves toward finding partners in China are logical steps, because “if you can’t beat them, join them.” While in the past, joint ventures were put in place in China for local automakers to learn the business from big foreign OEMs, now it is the other way around! These partnerships will allow these OEMs to shorten the learning curve and assure that their products remain competitive in an EV-based automotive market.

Tesla already has one foot in China, thanks to its Shanghai operations, but US legacy OEMs seem to be oblivious to the needs of the day. Instead of doubling down on EVs globally, they are delaying their targets. That can only be explained by some sort of ideological blindness, preferring to look back at a comfortable past instead of forward into an uncertain future.

This is especially difficult to understand in the case of General Motors, because it could profit immensely from its JV in China with SAIC, namely by selling its own label models like the Wuling Bingo, that would be a perfect fit in markets in Latin America, where GM is risking losing its status as a major player due to this refusal to engage with mass-market EVs.

Another aspect where the US EV industry is lagging behind China is the number of EV startups. Let’s imagine if a “Dieselgate” kind of scandal hit BYD. The Chinese EV industry would have literally dozens of brands step up to replace it, starting with all of the local startups — Li Auto, NIO, XPeng, Hozon, Leap Motor….

The USA does not have such a rich ecosystem. If anything happened to Tesla — let’s call it a hypothetical “FSD-gate” — who would step up? The market has two legacy OEMs in denial, a third half-foreign one (which ironically might actually save it from the same ideological blindness that the other two suffer), there’s one brand that looks promising but is still in early-startup stages (Rivian), and there are two others in their infancy (Lucid and Fisker).

While the Legacy OEM issues are more a political thing than anything else, the small size of the startups is significant, the product of a eucalyptus called Tesla that in true Silicon Valley style dries up everything around it. This is partly due to the fact that Tesla started much earlier than anyone else, and the VCs, media, and “influencers” were aboard since almost day 1.

Because they came later, Rivian and the others didn’t get the same attention, which is delaying their development and preventing the US EV industry from having good alternatives to Tesla in case something happens to it. It’s like having LeBron James playing in a team with two old-timers and a bunch of high-school players.

In Europe, the picture isn’t much better, not because the local legacy OEMs are helpless. They are not. Actually, most of them have credible plans for the EV transition, even at a cost of some cozying up with Chinese OEMs.

No, the weak point in the European EV industry is that all of their EV startups (Sono, Lightyear, etc.) have either died before they got to market, or are in seemingly eternal limbo. This lack of innovation in Europe is worrying, as it is the fresh blood that comes from these startups that will eventually trickle into the big OEMs and make them less square and more open to new opportunities. As it is, without local talent being properly developed (the exception being from Mate Rimac — a younger and, dare I say — a better — Elon Musk-type of entrepreneur), it is left to the legacy OEMs to learn the EV business the best they can with their Chinese partners.

(A final note on Mate Rimac: if Volkswagen Group was smart, they would hire him as the group CEO in a few — perhaps 10 — years.)

It’s a bit like those football leagues where there are strong teams but the large majority of players are foreign born.

Hyundai–Kia should be safe. They could have been more ambitious regarding production targets, but with top-notch technology and an abundance of battery makers right next door (LG, Samsung, SK …), they only need to push costs down, and production targets up, to transition into the EV era without major drama.

Finally, there’s Japan. While Toyota could become a smaller player after the EV transition than it is right now, it won’t go bankrupt, like many like to say. Toyota could be forced to make a deal with BYD, yes, but hey, there are far worse things than cozying up with BYD.

The remaining OEMs do not have it so easy. While Subaru could survive by staying close to Toyota, Suzuki can benefit from its Indian operations, and Nissan can benefit from Renault’s association with Geely, Mazda and Honda do not have an easy way out of the EV conundrum. The former is too small, and too engrained in ICE, to make a swift transition, while the latter has just broken up its EV partnership with GM and one wonders with whom Honda could partner now. It’s not going to be easy….

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy