EVs Take 24.5% Share In Germany — Enyaq Comeback

Support CleanTechnica's work through a Substack subscription or on Stripe.

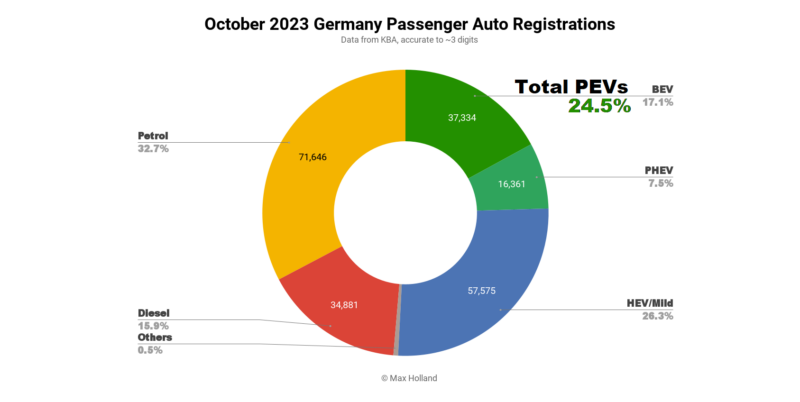

October 2023 saw plugin EVs take 24.5% share of Germany’s auto market, down from a 32.5% share in October 2022, and amidst a hangover from September 2023 incentive changes. Full electrics nevertheless saw sales volume slightly increase YoY, whilst PHEV volume declined. Overall auto volume was 218,959 units, up some 5% YoY. The best selling full electric was the Skoda Enyaq.

October’s combined plugin share of 24.5% comprised 17.1% full electrics (BEVs), and 7.5% plugin hybrids (PHEVs). These compare YoY with figures of 32.5%, with 17.1% BEV, and 15.4% PHEV.

Recall that October 2022 saw the start of pull-forward sales (especially of PHEVs), ahead of significant incentive cuts on January 1st. October 2023 was additionally in another hangover for plugin sales in the shadow of more recent incentive cuts, enacted from September 1st.

These perturbations (clear in the market evolution graph below) mean that the long term trends are being temporarily muddied by short-term disjunctures.

Despite this, the actual volume of BEV sales still increased YoY in October, up 4.3% to 37,334 units. Taking a step back, 2023 YTD BEV sales — at 424,623 units — are also up by 37.7% compared to the same period in 2022. This growth rate is equivalent to almost doubling volume every 2 years, a healthy trajectory.

As I mentioned last month, there are more incentive cuts coming in January 2024, so the disjunctions in market volume and share are not over yet.

Meanwhile, combined combustion-only vehicles were once more under 50% of the market, and from the second half of 2024, should remain in that range going forwards.

Germany’s Best Selling BEVs

The best selling BEV in October was the Skoda Enyaq, with 2,579 units, a great result, and its first time to take the top spot.

The runners up were the Audi Q4 e-tron (1,867 units) and Fiat 500e (1,760 units).

The Enyaq debuted on the German market in March 2021, and reached a previous high of 3rd spot, way back in September 2021. In recent months it has typically hovered around 4th or 5th spot, and stands in 5th place in YTD cumulative sales (averaging 1,673 per month). Good to see it finally hit the top spot.

The MG4 also put in a decent performance to take 4th position, at 1.45x its recent typical volumes.

Likewise, the BMW i4 saw 2.1x its typical volumes, and took 7th spot. Further down the rankings, its newer sibling, the BMW i5, continued to ramp volumes, seeing 261 units in October.

In terms of newcomers, October saw the Fisker Ocean debut in the German market, with a decent 96 units.

Another newcomer was the Kia EV9, with 33 initial units. At lower volume, and only really symbolically relevant, the Rolls Royce Spectre also made its debut, with 9 initial units.

Perhaps the most significant, the new Fiat 600e also debuted in Germany in October, albeit at a modest 6 units. The 600e is the bigger brother to the popular Fiat 500e (Europe’s 8th bestselling BEV in 2023 YTD, and 4th in Germany).

Under the skin, the 600e is an engineering twin to the Jeep Avenger, also part of the Stellantis group. It has a decent range of 409 km WLTP, with good fast charging (26 mins, 10-80%), and is priced from €36,490 in Germany. Let’s see how it gets on.

What’s happening in the 3-month rankings?

As in many of the other large European markets, the Tesla Model Y is Germany’s clear volume leader, despite being in a logistics low ebb in October. The Volkswagen ID. 4/5 is in second place, and the Skoda Enyaq is in 3rd.

Recall that August saw a huge pull-forward, with some brands more prepared to push high volumes that month, and others less prepared. Thus we see the Opel Corsa in a rare 5th place from August-October, but can expect it to fall back to the lower parts of the top 20 in the near future. The Ora Funky Cat is a similar story.

Let’s take a look at the manufacturing group performance:

Here, Volkswagen Group is still dominant, though share is down by 3.5% from the previous period (May to July). What Volkswagen Group lost, Stellantis gained, up by 3.5% from the prior period. The gains are partly because Stellantis grabbed the August pull-forward with both hands.

Further back, Tesla dropped from 13% share, to 9.4%, and fell from 3rd to 5th. Hyundai gained 1.6% share and stepped up to 3rd. Note though that the 3rd to 6th spots are very close — it could still go in any direction for the remaining months of 2023.

Outlook

Despite the bump in auto sales, Germany’s economy is at a negative 0.3% year on year growth rate, as of the latest Q3 figures. Interest rates are at 4.5%, the highest level since 2008–2009. Inflation continues to fall, to 3.8%, from 4.5% in September. Manufacturing PMI improved slightly to 40.8 points, from 39.1 points, but is still very weak.

In the long term, the total cost of ownership advantages are firmly on the side of BEVs, so no doubt the transition will continue. With incentive changes still ongoing, there will be some more ups and downs in market share over the next few months, but the longer term trajectory will still be upwards and onwards.

What are your thoughts on Germany’s EV transition? Please join in the debate below.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy