The Big ICE Meltdown — May’s China EV Sales Report

ICE model sales crash 39% in May

High gas prices and a never ending wave of new models has allowed May to reach record EV market share, with plugins reaching a record 63%!

However, while record market share was achieved in the past thanks to strong EV sales, this time, the record achievement is thanks to a significant ICE (internal combustion engine) crash. The overall market dropped 22% year over year (YoY), to around 1.5 million sales. ICE-powered models were at the epicenter of this disruption, crashing 39% YoY, but plugin hybrids (PHEVs) also didn’t do much better, dropping 25% in May.

The only thing that grew in May? Pure electrics. Despite having fewer incentives, BEVs were up 4% YoY, to 637,000 sales. This meant that BEVs scored a record 42% BEV share in China!

Adding PHEVs (21% share) to the tally meant that in May a record 63% of all cars sold in China had a plug!

This result pulled the 2026 share past the 50% mark, to 52% (the 2025 share was 54%). BEVs on their own were up to 34% (33% in 2025). And with the first week of June already presenting 67% EV share, expect another amazing result by the end of June….

At this pace, I expect the final number for 2026 EV share in China to be above 60%, with BEVs alone north of the 40% mark. Furthermore, I expect the whole Chinese passenger car market to be fully electrified by 2030. And when the largest global automotive market gets fully electrified … then it’s game over for the ICE industry elsewhere.

(Which means that investing money in R&D for ICE technology today is throwing money out the window, as there won’t be enough time to pay back the investment costs.)

Another interesting statistic is that the breakdown between pure electrics and plugin hybrids is shifting, to the profit of BEVs. At the beginning of the year, PHEVs were profiting from the incentive-derived BEV drop, but pure electrics are returning with a vengeance. May showed a 67% vs. 33% breakdown, to the benefit of BEVs, which has improved the 2026 average to 66%/34%.

Breaking down EV sales by domestic and foreign brands, there is a stark contrast — the EV share among domestic brands stands at 81% share! So, among local brands, ICE vehicle sales are going the way of the dodo quickly. Many probably still have them just because of export markets, while foreign makes are the only ones trying to milk what they can from a quickly dwindling market.

All of these disruptions are visible in the overall ranking. In the first months of the year, ICE models were populating the top positions, but May saw the first ever all-EV top 10 in the overall market, seven of them being pure electric models!

Looking at the best sellers in several size categories, EV disruption is also quite visible — all size categories had 100% plugin podiums, and only two models were not 100% BEV, the #2 BYD Song midsizer and the #2 Fang Cheng Bao Tai 7 full size model. And it should be noted that both dual powertrain models are in a process of increasing their BEV share, thanks to the new flash-charging versions.

Having a quick look at the five size categories, the highlight is the leadership of Changan’s Qiyuan Q05 crossover in the compact category, a welcome surprise for a model that became 100% BEV in this new generation.

Also, a note regarding city cars: they were the most affected by the subsidy cut, with the category having dismal results since then. Only the Wuling Mini EV is selling in decent numbers. Just to give an idea of the sales drop, this month’s second placed Geely Panda Mini scored fewer than 3,000 registrations, while in the same month a year ago, the same model had 17,000 registrations … and was only 3rd! Maybe it would be a good idea to create some kind of Kei-car category to revive sales of city cars?

Here’s more info and commentary on May’s top selling electric models:

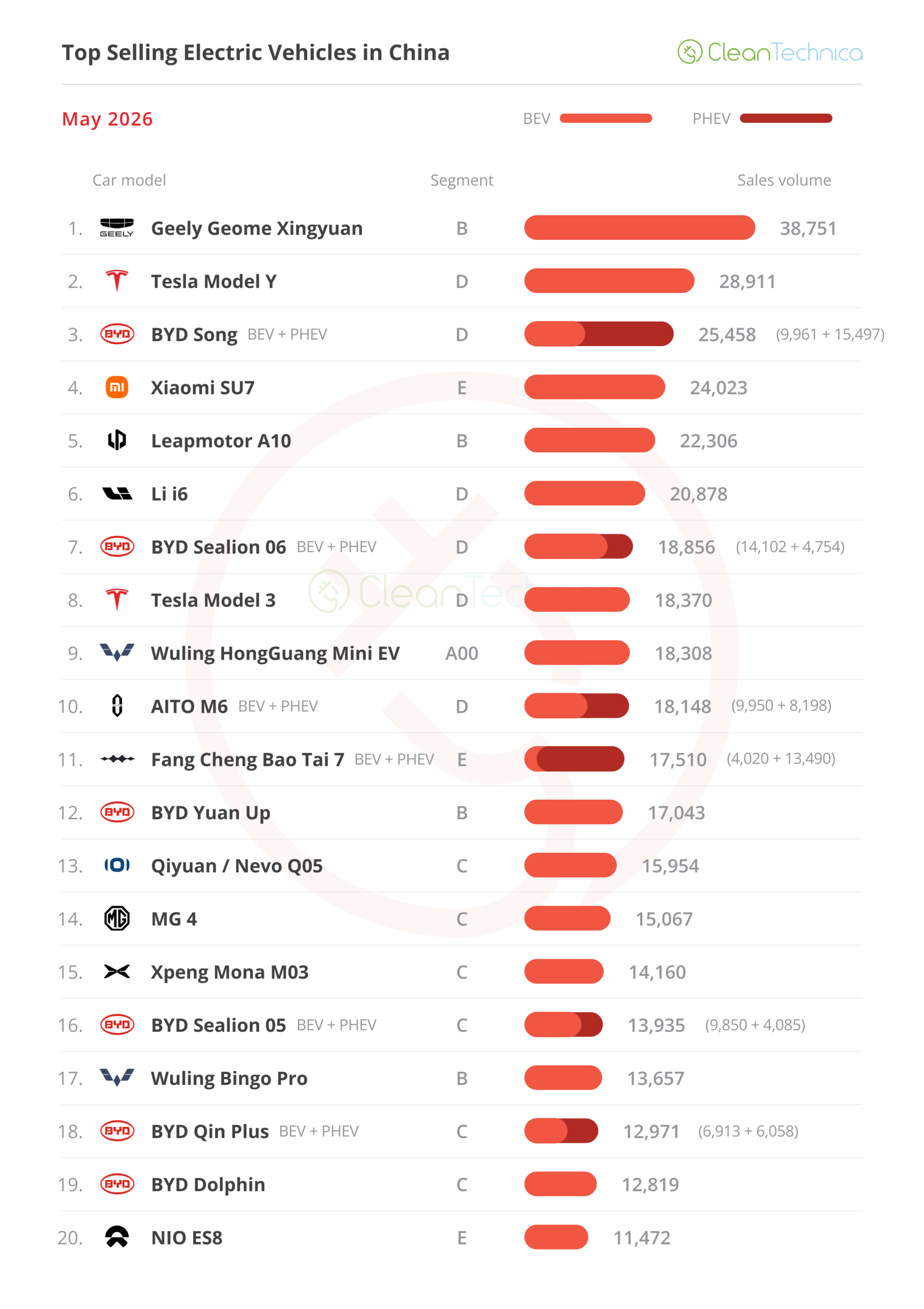

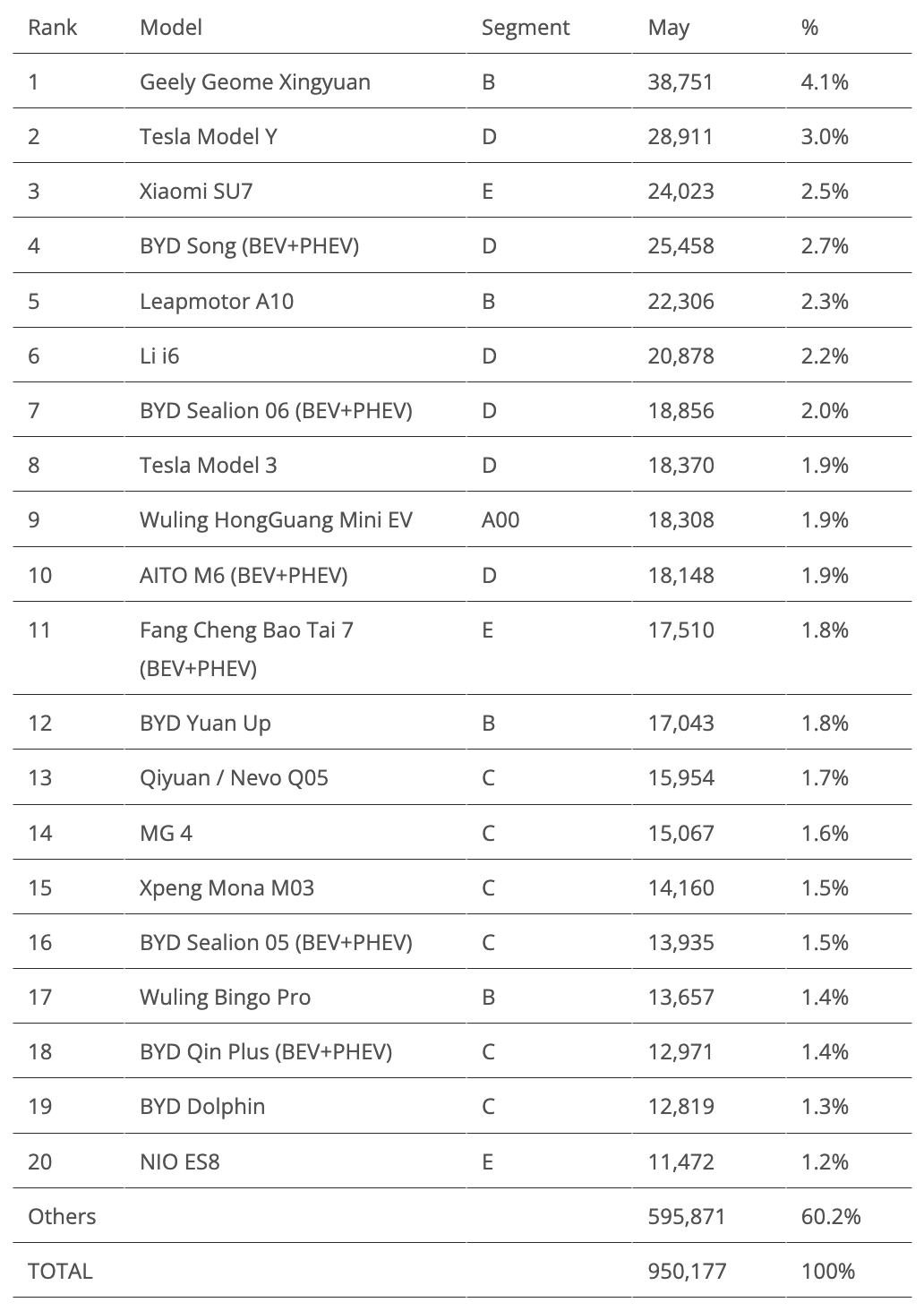

#1 — Geely Geome Xingyuan

A BYD Dolphin for BYD Seagull money ($10,000 USD). At least, that’s how Geely’s internal memo might have described the Geome Xingyuan when developing its latest hatchback. And it’s got an interesting name, as Xingyuan translates as “wishing upon a star.” It seems that Geely had its wish granted. The small hatchback has finally given the Hangzhou OEM the much coveted best selling model trophy. In May, the Geely model was once again #1, with 38,751 registrations, basically the same result as in May 2025. With the focus now being on export markets, the small hatchback is now at cruising speed in its home market.

#2 — Tesla Model Y

The extended wheelbase version, imaginatively called “L,” is helping the Model Y’s fortunes in China. In May, deliveries were up by 17% YoY, to 28,911 units. The long wheelbase version is proving to be a real lifeline for the US crossover, keeping the Model Y’s sales afloat. Although unable to challenge the Xingyuan’s leadership, the US crossover is benefitting from the generation change slowdown of the BYD Song and gaining precious advantage in the race for silver (the Model Y was 3rd last year).

#3 — Xiaomi SU7

The poster child of the Chinese EV market won another podium position thanks to 24,023 registrations, despite a 14% drop compared to the same month last year. This meant that it was the best selling sedan in China. With a Porsche Taycan–like design, but for Tesla Model 3 money, the startup’s EV success is undeniable. Having said that, the SU7, like its crossover YU7 sibling, has plenty of peaks and valleys in its career, which makes one wonder about the solidity of Xiaomi’s demand. Are Xiaomi’s EVs a fad, or is there real, consistent demand for the tech company’s products? To be a champion, consistency is key — one has to be good day in, day out.

#4 — BYD Song (BEV+PHEV)

BYD’s midsize SUV scored 25,458 registrations, allowing it to win a top 5 standing. With the model in a transitional stage — as the new, flash-charging capable, Ultra body is ramping up — sales are considerably down compared to the same month last year (-34% YoY). Still, once the new generation is fully ramped up, it will be a fierce adversary for the competition to beat. It features LiDAR and 1,500 kW DC charging, and these two features aren’t even the most impressive aspect of the model! That would be the price. It starts at 152,000 yuan (or $22,000) with the 76 kWh battery, and it goes up to 180,000 yuan (or $26,000) for the 83 kWh version. For comparison, the Tesla Model Y starts in China at 259,000 yuan ($38,250)…. Expect the Song to experience a second youth in the second half of the year, and while it should be hard to displace the Tesla Model Y from the second place position, the last place on the podium should be doable this year. And maybe go for gold in 2027?

#5 — Leapmotor A10

Things continue to go well for the startup brand, with their new baby A10 promising to be the star player of an already strong lineup. Thanks to 22,036 registrations in only its third month on the market, the small crossover managed a top 5 presence for Leapmotor, a first for the Hangzhou make. The model has the usual value-for-money focus of the brand, and a low, low price of 66,000 yuan ($10,000). On top of that, however, the A10 offers something close to a distinct personality, as the design eschews the white product standard design of Leapmotor for something more personal, mostly thanks to the front and back lights and a floating roof effect. With the model still in ramp-up mode, one wonders how high will the crossover sit on the table once it is at cruising speed.

Looking at the rest of the best seller table, one highlight was the #9 Wuling Mini EV scoring its best result of the year, 18,308 registrations. That is still far from its peak form, but considering how bad the rest of the city car category is … it is a great result.

A model on the rise is the #13 Qinyuan/Nevo Q05, with Changan’s mainstream EV brand benefiting from a new generation of its compact crossover to score a record 15,954 registrations, its third record result in a row! Still in the compact car category, the new-generation MG4 is proving to be a success, with the hatchback scoring a record 15,067 units. That means it beat its BYD arch rival, the BYD Dolphin, by more than 2,000 units.

The other major highlight is Wuling’s new baby, the Wuling Bingo Pro, which is basically the new generation of the Bingo hatchback. The model landed with 13,657 deliveries. Is this new generation ready to come after the category kingpin, the Geely Xingyuan? Hmm … I doubt it. But it will be interesting to see where it goes after such a strong landing month. Top 10?

Outside the top 20, a few models deserve a mention.

Let’s start with the landing of BAIC’s Arcfox Beta S3 sedan, which started its career with a significant 7,492 registrations. And while Arcfox is currently not a heavyweight in the Chinese EV market, the spiritual ancestor of this new model, the BAIC EU-Series, was the 2019 best selling EV in China and won the silver medal globally in that same year, only behind the all-mighty Tesla Model 3. So it will be worth following the career of this new sedan. Can it come close to the high scores of its predecessor?

After a promising start in April, the Chery QQ3 EV had 8,523 registrations in its second month on the market, which wasn’t all that different from its debut month. So … not even 10,000 for Chery’s Xingyuan-fighter?

Speaking of second-month performances, the new VW ID.ERA 9X land yacht SUV rose to some 5,000 registrations in May, and while that is not headline-grabbing news, it does at least show that Volkswagen is still in the game.

Because let’s be real — Volkswagen is no longer looking to dominate the Chinese market. It must not even have the ambition to remain a major player. If the brand manages to stay profitable, with say 3–4% of share of a fully electrified Chinese car market, that is already a win. A million sales a year in China would be a good target. That may sound small considering the size of market, but, by 2030, that will be a lot for a foreign OEM. Toyota will be around that too, while Tesla, if all goes well and there’s no black swan event in the meantime, should be close to 1.5 million sales a year in China. Other foreign OEMs? Not even close to a million. Most will have left the market.

Speaking of foreign brands, how about Buick? The US make continues to be welcomed in its adoptive country, with the new Electra E7 scoring 7,668 sales in its second month on the market. The midsize SUV could become a welcome surprise for Buick, which saw its sales fall by 31% in May.

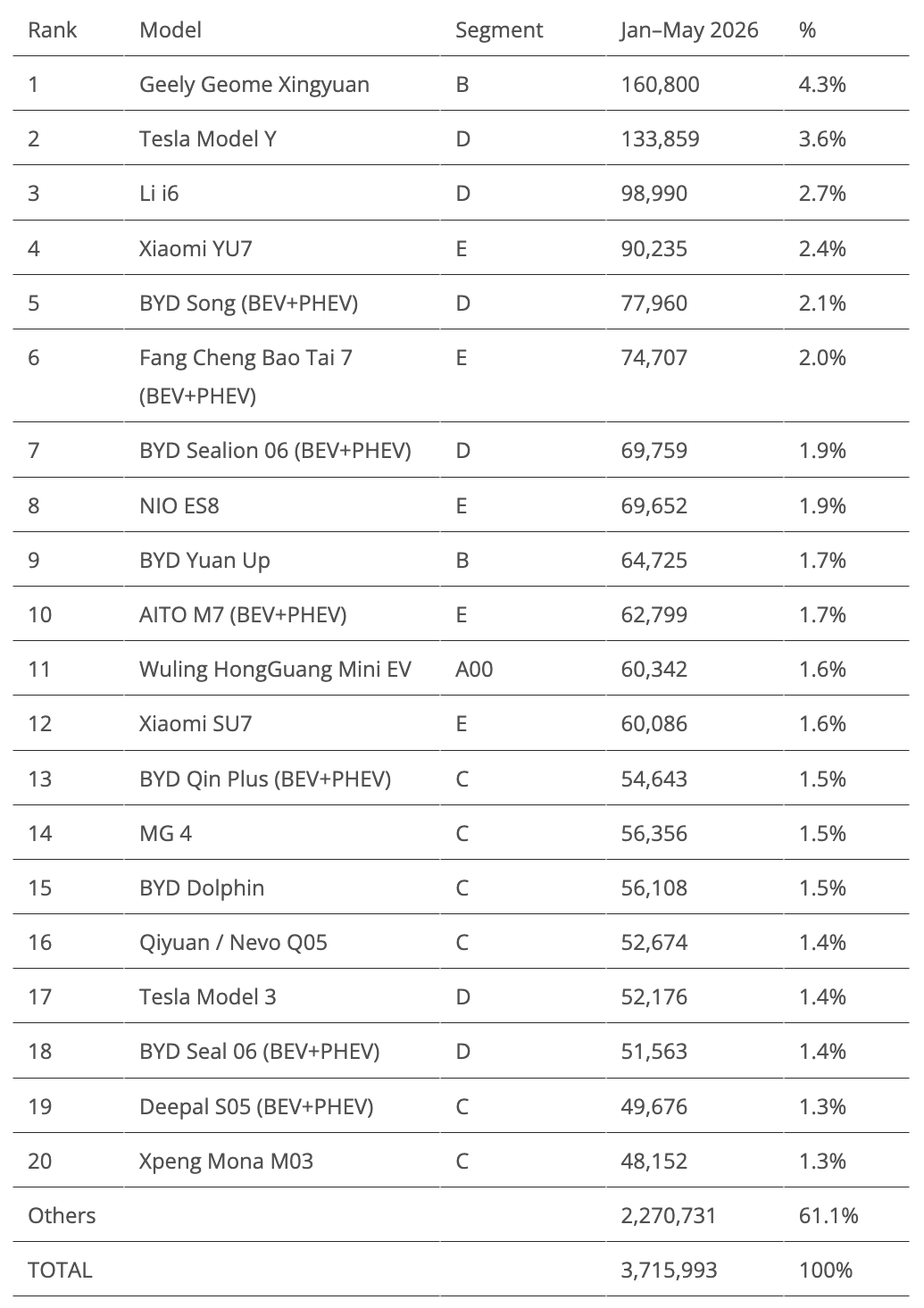

Looking at the 2026 ranking, the Xiaomi YU7 had another slow month, which means that the sporty crossover was surpassed by Li Auto’s i6 and the luxury MPV-SUV rose to 3rd.

Below the podium positions, it was another positive month for the BYD stable, with the rejuvenated Song jumping four positions into 5th while the Sealion 06 climbed another position into 7th. Additionally, the BYD Yuan Up was up to 9th.

But it wasn’t only BYDs that were on the rise. The MG4 climbed another spot, to 14th; the Wuling Mini EV was up to 11th; and the Qiyuan Q05 climbed another spot, to 15th.

Finally, two major climbers this month were the Xiaomi SU7, which jumped six positions into 12th, becoming the new best selling sedan on the table, and the Tesla Model 3, which returned to the top 20 in 17th and is hoping to get close to the #10 position by the end of June.

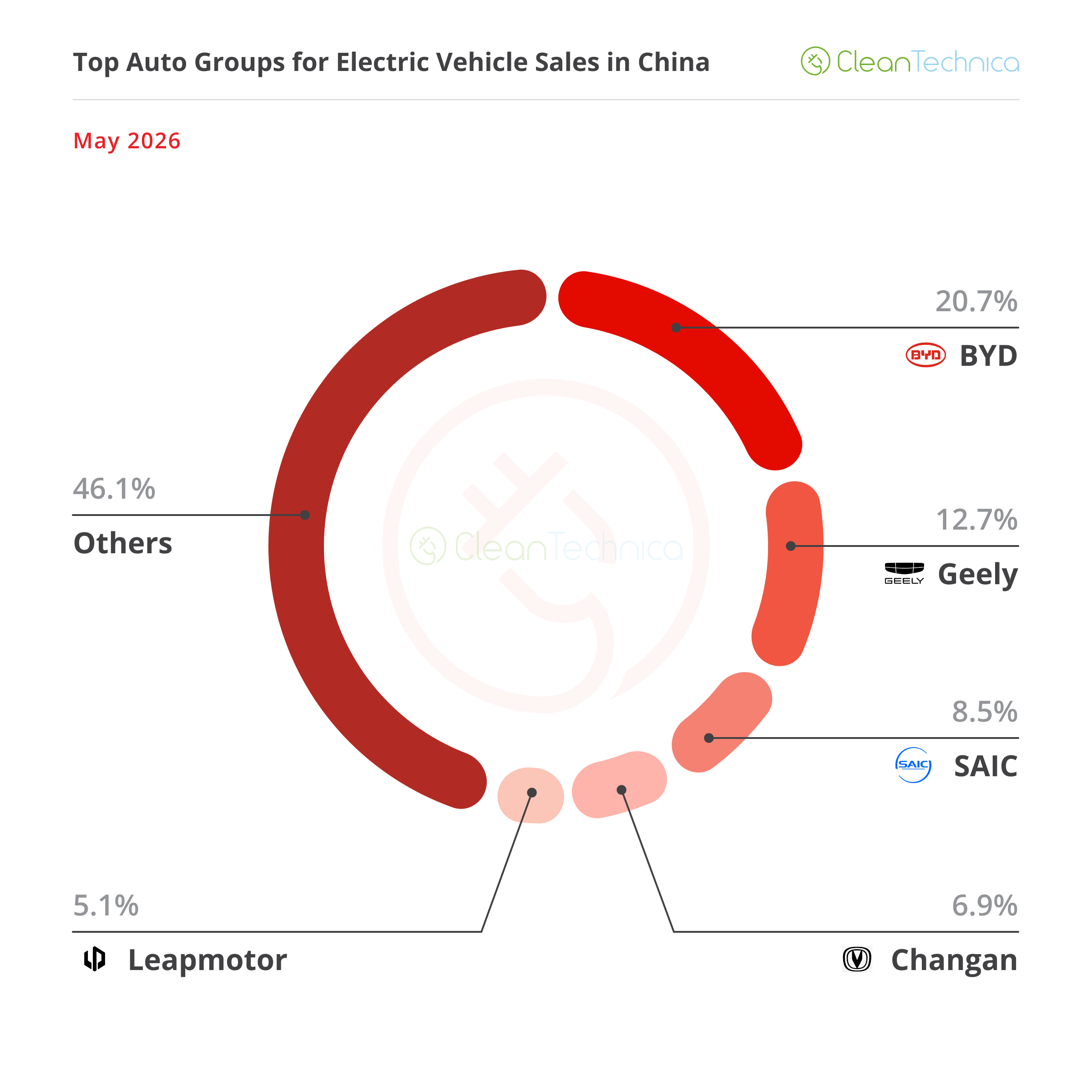

Looking at the overall manufacturer ranking, everything seems normal. BYD is on top, followed by Geely, Toyota, and Volkswagen.

Only, it’s far from being normal. Everyone seems to be bleeding sales. Seven of the top 10 brands experienced +20% losses.

So, if the big boys on top are crashing, who is winning?

Answer: Startups. And Tesla. #5 Leapmotor was up 48% YoY, to 61,401 registrations, another consecutive record score. At #7, Tesla is also rising, up 23%. Finally, there’s AITO. It was #10 in May, and despite its 6% sales drop, when everyone else is crashing … you win.

Looking below, a few more brands are experiencing surging sales, like #16 Qiyuan (+51% YoY). Meanwhile, Changan’s namesake brand is, unsurprisingly, crashing (down 64% YoY). This is an example of a managed transition — betting on new brands to ride the new technology (Qiyuan, Deepal, Avatr) while Changan itself tries to milk the old stuff to the last drop.

Looking at the auto brand ranking, there’s plenty of news. Leader BYD (16.8%, up from 16.1%) is firm in the leadership spot with comfortable distance over runner-up Geely (7.8%).

Tesla (5%) lost the last place on the podium to a rising Leapmotor (5.1%, up 0.5%), with the startup now in 3rd and looking to keep the US brand out of the medal positions.

Meanwhile, Wuling (4.9%) returned to the table, kicking Li Auto out of the top 5.

Looking at OEMs/automotive groups/alliances, BYD is leading, with 20.7% share of the market. Meanwhile, #2 Geely lost 0.4% share and got down to 12.7%, but the multinational conglomerate still had the runner-up spot secured.

#3 SAIC (8.5%, up from 8.1% in April) recovered ground, mostly thanks to Wuling and MG.

#4 Changan (6.9%, down 0.1%) is safe in 4th, but the new 5th placed Leapmotor (5.1%) will have a hard time keeping Tesla (5%) out of the top 5 in June.