Latin America EV Sales Report: Sales in Q1 Grew 74%, Reaching a New Record of Over 115,000 Units!

Support CleanTechnica's work through a Substack subscription or on Stripe.

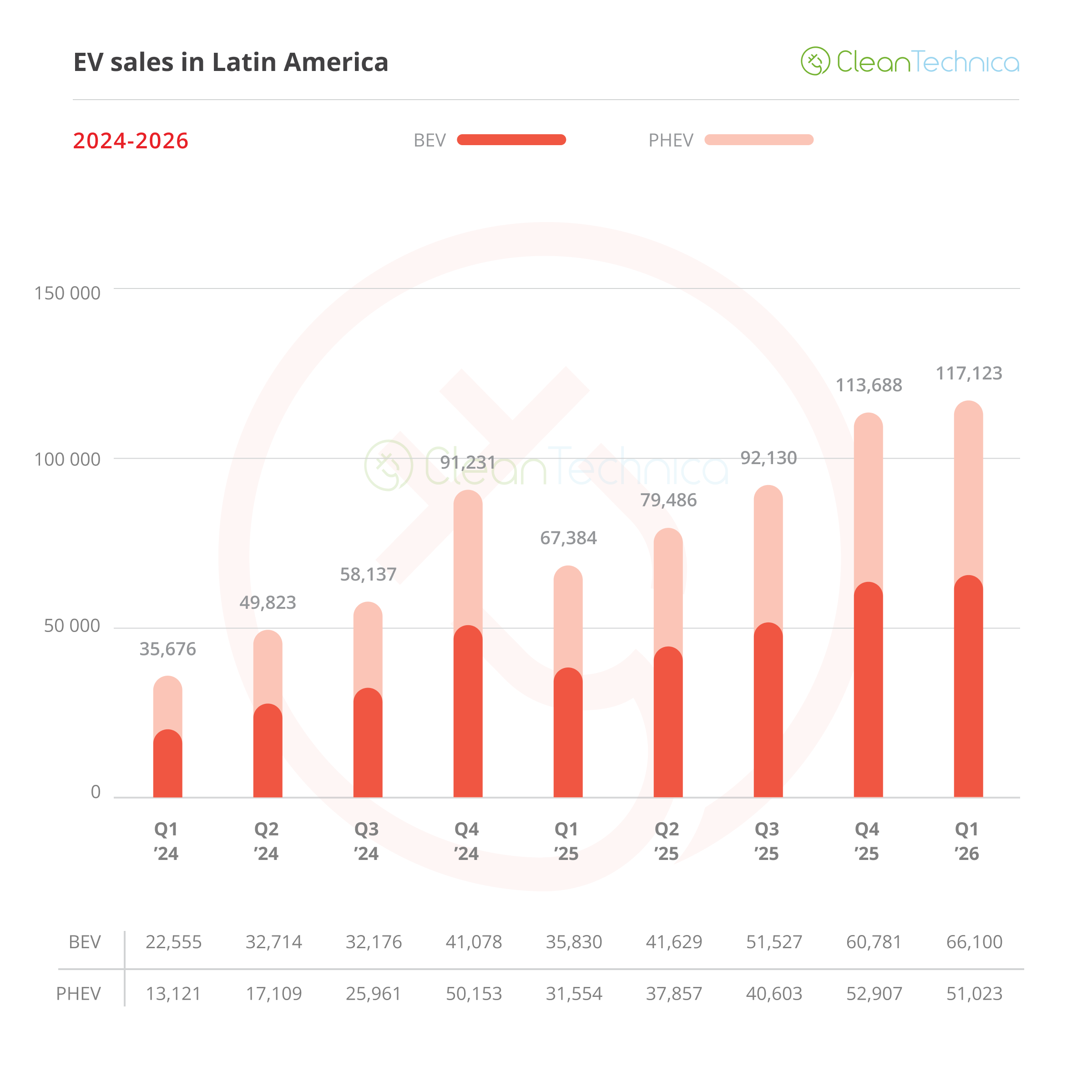

A mere quarter ago, we were celebrating the first time ever Latin America had seen more than 100,000 EVs sold in only three months. Now, thanks to significant growth year-on-year (YoY), we’re once again reaching a record, with Q1 surpassing 115,000 EVs sold in the region!

This is a deviation from the previous trend: normally, we would expect Q1 to stand below Q4 the previous year: for example, in 2025, EV sales in Q1 fell 27% compared to Q4 2024, despite growing nearly 90% YoY. But the first quarter of 2026, EV sales increased by a robust 74% and managed to grow 3% compared to the previous quarter, which, may we remind our readers, was a record at the time.

BEVs led with an 84% increase YoY, whereas PHEVs grew 62%. Market share reached 4.3% for BEVs and 3.4% for PHEVs for a total of 7.7%, perhaps a bit less than we would’ve expected due to the overall market also increasing by a solid 20%. If costumer interest remains and high oil prices start to hit the region, there’s a very real chance we will surpass 10% at some point this year.

Market overview

As far as the available data we have in ZEMO, EV sales roughly doubled YoY in 2023 and 2024*, whereas the increase in 2025 slowed down to 50%. Q1 2026 seems to be a return to stronger levels of growth and will hopefully put the EV transition again on a faster track (reasonably, the 50% growth seen in 2025 can already be considered “fast”). *Due to data constraints, this number excludes Mexico, which only started providing reliable data in 2024, making a comparison with 2023 impossible.

This growth means that EV sales in Q1 rose to 117,123, with BEVs, now at 56%, gaining a smidge of market share, a development that may or may not continue in the coming months:

Market-share wise, plug-ins managed to reach 7.7% market share, again an all-time high, well above the 6.4% of Q4 2025 and 5.3% of Q1 that same year.

All this is happening just as fuel prices are starting to increase in the region (at least in the countries where they are not heavily regulated), meaning there’s reason to believe Q2 could be even better.

Now, the fact that EV sales are booming, sadly, has yet to translate into a decline in non-plug-in vehicles, including combustion and hybrid cars. Most countries’ vehicle markets gained sales in Q1, with the overall market up 20% YoY, meaning that once we subtract EVs, we find that fuel-only vehicles rose from around 1.2 to 1.4 million units. Yes, the increase would’ve been higher without EVs (50,000 higher to be precise), but the ICEV meltdown is still ahead.… Though, if fuel prices get high enough, perhaps it will come sooner than anybody expects.

The good news is that total vehicle sales in Latin America have actually fallen from their peak in 2014, and, despite their recent recovery from COVID-caused lows, are yet to rise back to those levels (with sales in 2025 still some 10–15% below that all-time peak).

Country overview

By and large, we see a very similar situation to Q4 2025 in our list, with an identical top 5: Brazil, Mexico, Colombia, Uruguay, Costa Rica. Further down, Ecuador managed to surpass Chile, a notable development given significant growth on the Chilean side, and Argentina surpassed a thousand BEV registrations (tripling the result from Q4 2025) and reached nearly 3,000 PHEVs:

A different picture arises when looking at market share. Uruguay here becomes the indisputable leader, just shy of 30% BEV market share and with an additional 3% PHEV market share, followed by Costa Rica and Colombia, the latter closing the gap on second place. Ecuador is #4 with a decent 6% BEV, and Brazil closes out the top 5 at 5% BEV and 4.7% PHEV market share:

(As you may notice, we have information now on PHEVs for a few markets where this information was not available a mere quarter ago, thanks to the work at ZEMO collecting ever more accurate data.)

A quarter ago I said the space between leaders and laggards was increasing, but with Argentina’s sudden jump, this is less true today than in 2025. However, some markets at the bottom of the list do have either very sluggish growth or even a reduction, as happened in Panama and El Salvador. This is something we had not seen before and, to be honest, is something I find quite surprising, as I expected more affordable prices would invariably lead to higher adoption levels so early in the transition.

Looking at countries individually, we find leading Uruguay sprinting ahead of Costa Rica, which held the title for years but which has had very sluggish growth in the last couple of years…. Though, that could change soon as a result of fuel prices going up in the country. As for Uruguay, with 166% growth YoY already from a high base, the sky’s the limit, and if fuel prices also go up in the small austral country, we could well see it rise past 40% in the near future.

Meanwhile, at #3, Colombia is feeling the impact of the most affordable Teslas in the world, growing by 187% quarter-to-quarter and by a massive 279% in March alone, thanks to a veritable tsunami of Tesla registrations that accounted for half of all BEVs that month. Market share in the country rose to 20% that month (18% BEV), meaning that if momentum is sustained, it could well rise to second place in our next quarterly report. Of course, we have to wait a couple more months to make sure all those Model Ys and Model 3s were not just backlog orders from the four months prior. Colombia’s market is also benefiting from an insane price war, most noticeable by the arrival of two hyper-competitive SUVs: the MG S5 at USD$26,700 and the Chery E5 at USD$22,500.

But even then, Colombia’s market is not the one with highest growth. Looking only at BEVs (as I think it’s the fair thing to do when PHEV data is not available), we find Ecuador in position #4 with massive 244% growth YoY, and if we look only at March, it raises to an insane 451%. Truly, I thought the days of such outrageous numbers would be over once we got past 2% market share, but it seems the factors driving the transition in some countries have gone into overdrive lately. And keep in mind both Colombia and Ecuador are net oil exporters with regulated oil prices, meaning all this is happening with relatively stable gasoline prices.

Latin America’s giant, Brazil, is at a very respectable #5 position, growing at the same rate as the regional average (74% YoY). Notably, BEV sales are growing much faster than PHEVs (105% vs 49%) and now make up a majority of sales; whether that’s a long-time trend or a one-time circumstance, we will have to wait to find out. Local production is ramping up, and competition from locally made EVs should increase significantly in the next couple of years. Market share in Brazil has not risen as fast as overall EV sales due to significant growth in the general vehicle market as well.

In #6, we have Chile, yet another country showing significant growth (+132% YoY), and yet another one which saw growth explode in March (+234%). BEVs lead the plug-in segment (56%), but they’re growing far less than PHEVs, which increased by an impressive 319%. Overall market share, at 4.7%, still remains relatively low, but in the e-bus segment, we see a massive drive towards electrification, with 80% of new buses being electric in the quarter. As every bus can easily consume as much fuel as 100 cars, there’s an oversized impact from this switch, making up for relatively slow EV adoption in the passenger segment.

And we have to get to #7 to see some less-than-stellar news. Mexico, the other Latin American giant, has greatly slowed down its pace of growth, increasing by only 23% overall, and with BEVs growing by a mere 10%. This is probably due to the fact that the Mexican government — under US pressure — has increased tariffs on Chinese vehicles to 50% in 2026, and unlike Brazil (which also raised tariffs), Mexico has no local production to rely on. There are rumors of Geely, Vinfast, and BYD being interested in Nissan’s former plant in Aguascalientes, but it will take a while for any of these automakers to ramp up production, and Trump can still pressure Sheinbaum’s government to limit Chinese investment in the country (though, presumably, Vinfast would be exempt from these restrictions).

Paraguay, at #8, remains an elusive country to get accurate data on, and the information we present is only for the first two months of the year, as no data has yet been published for March. Calculating yearly growth is hard, as monthly data isn’t available from 2025 (the first datapoint we have is for H1), but extrapolating from the first two months, we can roughly calculate a 100% growth rate if the trend continues as it has.

And at #9, we find a rising star, albeit from a very, very low base. Behind us are the days when Argentina’s EV market was little more than symbolic, with market share below 0.1% … as only in the first quarter, the Argentinian market has sold sevenfold as many EVs as it did in the entire first half of 2026. Thanks to this, BEVs have risen to 1% market share and, more impressively, PHEVs have exploded and stand now at 1.8%. Argentina’s EV sales have benefited from a steady source of Brazil-made EVs with very low tariffs, and the country seems ripe for growth as people get more accustomed to these new technologies.

Finally, our last four positions bring us back to countries with less-than-stellar news. Peru is the only one to show strong(ish) growth (+99%), but EV market share remains below 0.8%, and BEVs have not even reached 0.4%. Panama stands just above 1% market share, but BEV sales decreased by a massive 50% in Q1. Both of these countries have significant presence from Chinese brands and both lack any meaningful oil reserves, so I can’t understand why this transition is taking so long.

As for El Salvador and Guatemala, both presented a decrease in BEV sales of 16% and 12%, respectively. Though, in the case of Guatemala this information may be reviewed once we get local data from Amegua, Guatemala’s EV organization, which has decided to kindly help us at ZEMO to provide accurate data for their country. Both of these countries are also net oil importers, both remain below 1% market share (due probably to the availability of hyper-affordable used ICEVs in their markets), and both lack the size and/or wealth of Peru and Panama, meaning the current oil crisis could affect them severely.

Final thoughts: regional transition amidst global turmoil

Latin America may have some of the most important oil producers in the world, including Brazil, Mexico, and Venezuela, but the region as a whole still depends on imported fuel, as local production and refining capacity is not enough to keep up with demand. If the current crisis was to continue, and, most importantly, if the US was to limit fuel exports to guarantee local availability, most countries in the region could be facing a severe fuel crisis.

For now, however, fuel prices have gone up much less than in other parts of the world, or in some cases have not gone up at all. Mexico and Brazil, for example, present fuel price growth of around 10%, much less than more free-market oriented countries such as Canada and the US. Smaller countries which lack oil production and refining will probably see higher price increases, but even some of these (such as Panama) have turned to subsidies to prevent inflation spikes and social unrest. Still, prices are going up in most countries in the region, but this means the pressure from the crisis is, for now, more political than economical, and it’s uncertain that national leaders will choose to pivot to EVs in order to protect their budgets, more so as this will not provide immediate relief in any case.

All in all, we see EV adoption being driven in the region by economical concerns (made better as more affordable EVs arrive on our shores and as fuel prices rise, slow as that process may be) and by policies aimed at the promotion of EVs or, more commonly, that disincentivize ICEVs (such as traffic restrictions). If the worst comes out of Trump’s adventure in Iran and the world enters a global recession driven by high oil prices, 2026 could easily bring the end of the combustion-car recovery seen after the peak in 2013–2014 and start an irreversible trend of decline in combustion-only markets, bringing forth an era of cleaner, greener, and cheaper transportation.

And remember, you can check out more details in our Zero-Emissions Observatory.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy