EVs Take 24.1% Share In France — Popular BEVs Hit By Incentive Stop

Support CleanTechnica's work through a Substack subscription, on Patreon, or on Stripe. Help us produce all of the high-quality, original content we publish week after week despite the challenges of content-scraping AI, antisocial media, inflation, and other hurdles.

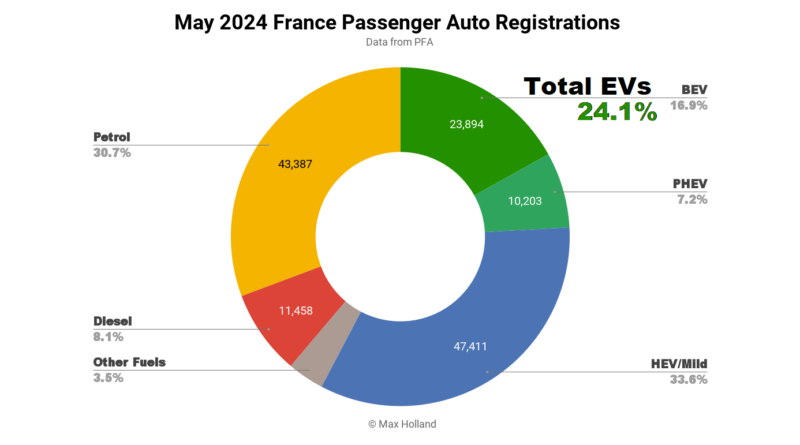

May’s auto sales saw plugin EVs take 24.1% share in France, roughly flat from 24.3% year-on-year. BEV share was up, while PHEV share dropped. Overall auto volume was 141,298 units, down by some 3% YoY. The Peugeot e-208 now has a strong lead in the BEV rankings.

May’s results saw combined plugin EVs take 24.1% share in France, comprising 16.9% full battery-electrics (BEVs), with 7.2% plugin hybrids (PHEVs). These compare with YoY figures of 24.3% combined, with 15.6% BEV, and 8.7% PHEV.

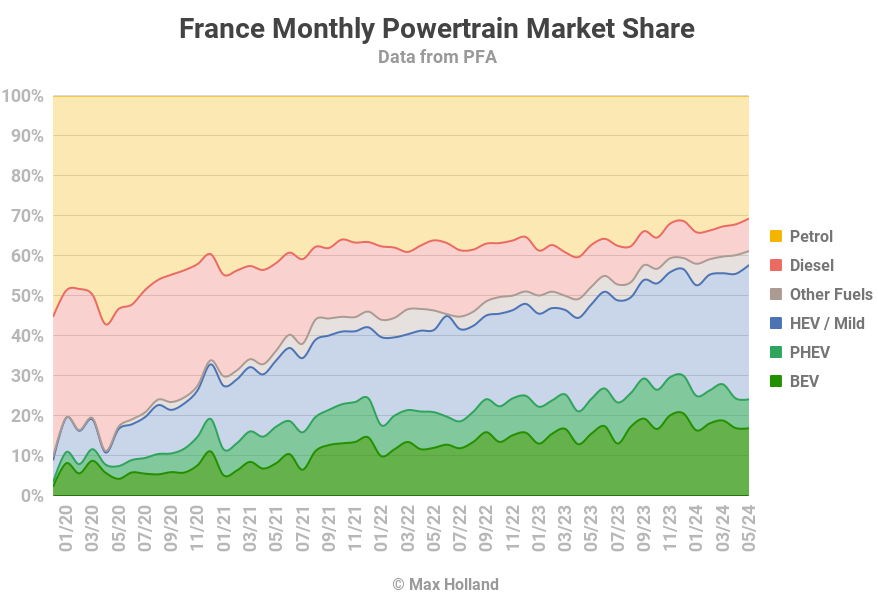

If you’ve been following our French market reports this year, you will remember that there have been two main forces at play in the BEV market in recent months.

The first was the March 15th cancellation of the eco-bonus for BEVs made outside Europe. This included many of the most popular BEVs; Tesla Model 3, Dacia Spring, Kia Niro, Kia EV6, BYD Atto 3, Volvo EX30, MG4, Ford Mach-e, Fisker Ocean, Nissan Ariya, Toyota BZ4X, and many others.

The removal of the bonus for these models has effectively blocked (or severely smothered) some of the least expensive BEVs (e.g. Dacia Spring, MG4) and some of the best value BEVs (e.g. Volvo EX30, Tesla Model 3) from the market. The end result is that the spectrum of BEVs that remain now contains fewer affordable options, and fewer good-value options, than previously. Not great.

The second force at play has been the social leasing programme which ran from January to mid February, and managed to sign up 50,000 new BEV lease contracts (twice the planned number). The contracted BEVs were not typically delivered “at signing” but instead, with some wait time (several weeks to a few months). For example, April saw a strong bump in BEV registrations (up 44.9% in volume year on year), which was almost certainly an effect of the social leasing programme.

However, most of those 50,000 leased units have probably made their way through to deliveries by now, and we know that after a “pull forward” effect, there is typically a consequent “hangover” effect.

Add to that hangover, the stopping of the eco-bonus for many popular BEVs, and what do you get? A depressed BEV market. I expect the slowing YoY volume growth we see in May is part of this, at just 5.4% (compared to the 27.7% January to April average). Likely June (and perhaps July, and August) will also see unimpressive YoY growth, or perhaps even negative growth. Let’s keep an eye on this.

Beyond BEVs, most other powertrains were down in volume YoY, except for HEVs (plugless hybrids and mild-hybrids), which were up by a strong 38%. Likely most of these are 12 volt or 48 volt “mild hybrids”, which are a very cheap (and temporary) fix for manufacturers to meet tightening emissions rules.

Meanwhile, PHEVs sales volumes were down YoY by 19%, petrol-only down by 20%, diesel-only down by 25%.

Best Selling BEVs

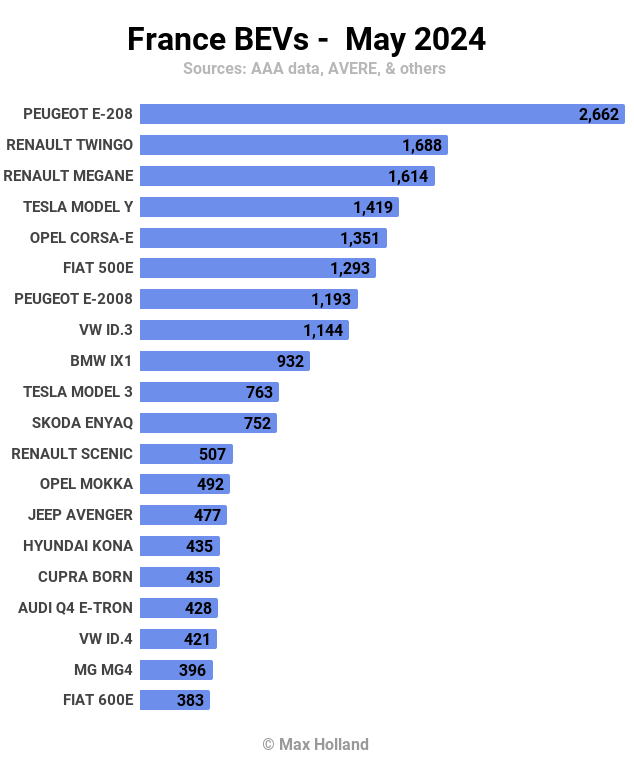

The Peugeot e-208 has been the best selling BEV in France for every month of the year so far. May saw it deliver 2,882 units.

In second place was the Renault Twingo, with 1,688 units, and its sibling the Renault Megane came in third, with 1,614 units.

It is likely that all of the top three are strongly benefitting from remaining delivery units from the social leasing scheme.

Their elevated rank is also a consequence of the cancellation of the non-European BEVs noted above: in the final quarter of 2023, none of these now-top-3 models even appeared in the top six, let alone in the top 3. Back then, the Tesla Model 3, Tesla Model Y, Dacia Spring, and MG4 were regularly dominating. As of May, only the European-made Tesla Model Y remains near the top now, the Model 3 is relegated to 10th, the MG4 to 19th, and the Dacia Spring has disappeared entirely!

We don’t have access to deep enough market data to detect the trace volumes of any potential new BEV models debuting on the French market. See our other European reports for the regional picture on emerging models, which are likely to now (or soon) be on sale in France also.

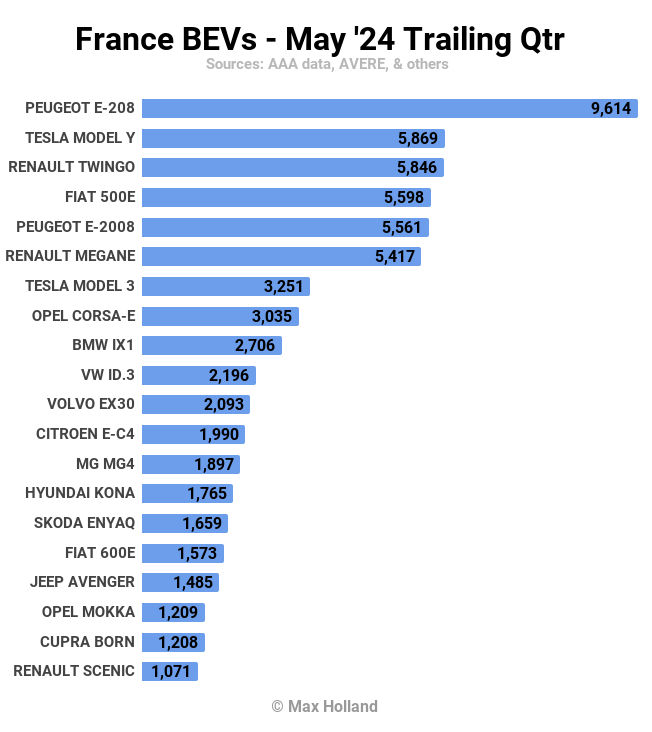

Let’s take a step back to review the longer term rankings:

The trends shaping the trailing 3 months rankings are similar to those shaping the month-to-month. The Tesla Model Y was not part of the social leasing programme, so it has dropped to second place since the December to February period. The Peugeot 208 has stepped up in its place to take the lead.

Hit by the double whammy of the leasing and the incentive cancellation, the Tesla Model 3 has fallen from 2nd in the prior period, now down to 7th. The Model 3 will likely fall further, since this period is still propped up by a decent March, when it managed to make okay sales just prior to the incentive cancellation.

The MG4 is in the same boat. It is now down to 13th spot, from 4th in the prior period. Again, March saw okay sales, so this 3-month window is still propped up somewhat. The MG4 will struggle to stay in the top 20 going forwards. With a level playing field, the MG4 is one of the most compelling and best value BEVs on sale in Europe – French consumers are worse off now that it has been boxed in.

The Dacia Spring is in even worse shape. In the December to February period, it was in 5th spot. Now it has disappeared almost entirely. It had just 148 sales in March, and then a pitiful 35 sales in April and May combined. This is a great shame, because over the past 3 years, the Spring was periodically the monthly best seller in France.

When the level playing field was in place, the Spring was also the only BEV in Europe that could be called roughly “affordable” on an absolute basis, and was loved by French consumers, just as affordable classics like the Citroen 2CV, and Renault 4, were loved by previous generations of French drivers.

There’s been plenty of excitement about the upcoming Citroen e-C3, which is due to start customer deliveries in the next 2 or 3 months (September at the latest). The C3 has a decent balance of specs for an entry BEV, with 44 kWh usable LFP battery (45 kWh gross), and decent efficiency. In favourable weather conditions, it should be able to repeatedly cover 2 hours of sensible highway or rural driving, between DC charging stops of just over 30 minutes. This duration of charging and driving cycle is more than good enough for many Europeans who only make long journeys very occasionally, especially in areas with decent DC infrastructure. In short – the car itself is all well and good.

However, while the pricing (from €23,300) might appear to be good in relative terms, given typically high European BEV pricing, in reality, the e-C3 is still far overpriced given the low cost of BEV components. LFP cells now cost just €49 per kWh, and a 45 kWh battery pack can be produced for under €3,000. The Citroen C3’s integrated 3-in-1 drive unit (83 kW peak) can be sourced for under €2,000 in large orders, with a few hundred more for other power electronics and controls.

Altogether, this adds up to well under €6,000 in BEV-specific powertrain costs. Then there are the savings of at least €1,500 to €2,500 from avoiding the ICE, transmission, emissions control system, and other ICE ancillaries. Realistically the cost premium for the BEV over the ICE variant should not be more than ~€4,000.

Why then in France and Germany does the BEV variant get priced from €23,300 MSRP, whilst the ICE variant is priced from €14,990 MSRP – a difference of €8,310? To me this over-inflated pricing is just another example of legacy auto companies keeping their foot on the brake of the BEV transition. Please share your thoughts on this in the comments section.

Outlook

Looking past the weak auto market, France’s broader economy saw 1.1% YoY growth in Q1 2024. This is far healthier than the Euro-area average of 0.4% in Q1, let alone the negative growth in neighbours such as Germany (-0.2%), the Netherlands (-0.7%), and Norway (-0.8%).

Inflation was flat at 2.2% in May, and interest rates finally reduced to 4.25% after 7 months at 4.5%. Manufacturing PMI was 46.3 points, from 45.3 points in April.

As discussed above, the coming months will likely see a hangover related to the tailing-off of the social leasing deliveries, and the continuing lack of incentives on non-European BEVs, which were previously the most affordable and best value BEVs available. We will keep an eye on how these dynamics influence the market.

What are your thoughts on France’s auto market and transition to EVs? Please join in the discussion below.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy