World EV Sales Now Equal 18% Of World Auto Sales

Support CleanTechnica's work through a Substack subscription or on Stripe.

Or support our Kickstarter campaign!

Global plugin vehicle registrations were up 45% in August 2023 compared to August 2022, rising to 1,238,00 units. In the end, plugins represented 18% share of the overall auto market (with a 13% BEV share alone). This means that the global automotive market is firmly in the Electric Disruption Zone*. Add over 800,000 units coming from plugless hybrids and we have one quarter of global registrations having some form of electrification! (*People have asked me what the “Electric Disruption Zone” is. Basically, it is the steepest part of the tech adoption S-curve. Between 10–20% and 80–90% market share growth will accelerate, and then it will slow down on the way to 100%.)

Full electric vehicles (BEVs) represented 71% of plugin registrations in August, keeping the year-to-date tally at 70% share.

20 Best Selling EV Models in the World in August

Looking at August best sellers, there were no surprises on the podium. The Tesla Model Y was high above everything else, even scoring its best off-peak month ever. A record performance could come in September.

Behind it, the Tesla Model 3 again lost the race against the BYD Song for the silver medal, due to Tesla’s off-peak month. Although, with refreshed Model 3 deliveries beginning in October, expect this race to tilt heavily towards the US sedan from then on. Speaking of the Chinese SUV, the BEV version had a record month, 9,081 registrations. We could soon see the midsize model have a more balanced breakdown between the PHEV and BEV versions.

BYD highlights were the #7 Dolphin and #5 Seagull, with both models hitting record performances, 32,288 units in the case of the larger hatchback and 34,841 units in the case of the smallest EV in the BYD stable. The Dolphin benefitted from the start of exports. The Seagull is rapidly ramping up production, having reached close to 35,000 registrations in only its 5th full month on the market. It is still early to guess how high these models will get in the table, but I will go out on a limb and say that the Dolphin could be a future podium candidate while the BYD Seagull could become the only model strong enough to threaten the Tesla Model Y’s leadership position in the table!

There was another record performance on the top half of the table, and in this case, it wasn’t (thankfully) coming from either Tesla or BYD. The #8 GAC Aion Y had a record 26,719 registrations. It was the best selling NTNB (non-Tesla, non-BYD) on the table.

With its sedan stablemate GAC Aion S in #10, with 22,650 registrations, it looks like GAC is the only automaker that could run at the same pace as the top two. The Aion Y and the Aion S are in fact the best selling NTNBs on the table.

Elsewhere, the second half of the table saw two midsize plugin hybrid sedans hit record results, with the #16 BYD Destroyer 05 scoring its 3rd record in a row, 12,096 registrations, and the #20 Geely Galaxy L7 getting 11,117 registrations.

The #16 VW ID.3 also shined, with 14,363 registrations, thanks to Volkswagen’s Chinese operations. The model benefitted from a significant price cut in China**, allowing it to jump into record territory, if we exclude the (in)famous 28,110 units of December 2020, when Volkswagen deployed boatloads of units in order to meet Europe’s CO2 emissions targets. (See, Volkswagen — for the right price, people still love you….)

Outside the top 20, there is plenty to talk about. Going from biggest to smallest, the Cadillac Escalade-like Li Xiang L9 had a record result of 10,933 registrations. Added to the strong results of the brand’s other two models, that meant that Li Auto’s machine was firing on all cylinders. Everything they make is already sold, something that no other OEM can claim.

In the midsize category, the highlights come mostly from Korea, with the Hyundai Ioniq 5 (10,510 units), Ioniq 6 (5,084 units), and Kia EV6 (9,561 units) all hitting record results. It seems the Korean OEM has finally solved its battery constraint issues and is ready to increase its output by a significant margin.

Another model on the rise is Changan’s Deepal S7, the make’s take on the Tesla Model Y recipe. It reached a record 8,891 registrations in August. Could this new model become the brand’s best selling vehicle soon?

As for the compact category, we salute the third record performance in a row from the value for money king, the Skoda Enyaq. It scored 8,226 registrations this month. Now, about those deliveries in China ... is it just me that sees this as low-hanging fruit? I mean, the Enyaq seems a more appropriate model for Chinese tastes than the VW ID.4. Just sayin’.

As for the compact category, we salute the Great Wall’s Ora Good Cat, which got 9,616 registrations, the hatchback’s best result since December 2021.

Top 20 EV Models YTD

In the year-to-date (YTD) table, this time the Tesla Model 3 couldn’t resist the advances of the BYD Song, pushing the Tesla to the 3rd position in the ranking. With the sedan now in the middle of a refresh, expect the Chinese SUV to retain the runner-up position for a couple more months, but the Model 3 should regain the silver position in December thanks to an unusually high tide month for the sedan.

The other big highlight of the month is the five-position jump of the BYD Seagull, which was up from #18 to #13 in just one month. Expect it to continue rising until the year end, probably ending the year in the top 10.

Other points of interest are the hot #10 GAC Aion Y looking to surpass the #9 BYD Han, and the rejuvenated VW ID.3 looking to improve on its 17th spot, maybe climbing a couple of positions in the coming months.

Finally, we have a new face in the table, with the Li Xiang L7 now showing up in #20. Meanwhile, its seven-seat sibling, the L8, was #21, some 1,500 units behind. Both the Volvo XC40 and the Hyundai Ioniq 5 need to step up their game if they want to stay in the table, as Li Auto is looking to place all three of its models in the top 20.

Top Selling Brands

In August, BYD continued its never-ending record streak, thanks to a 261,000-unit performance. It was the 4th record in a row for the Shenzhen make. Having said that, Tesla also has reasons to smile, because it had its best off-peak month ever.

Below the top two galactics, GAC Aion ended the month in 3rd, banking on its dynamic duo to get its 3rd record performance in a row, 51,570 registrations.

This allowed it to beat Volkswagen to the last position on the podium. Not far below it, we have #5 BMW, ending the month only 400 units behind Volkswagen.

#7 Li Auto goes from strength to strength, with another record month, its 5th in a row. It had close to 35,000 registrations thanks to strong results across the lineup. With the startup brand still supply constrained, expect the high-end make to continue beating records regularly in the near future. But the real fun will start when the L6 and L5 midsized models land sometime next year.

The middle of the table saw #12 Hyundai score a record result (25,551 registrations). That was thanks to good results from the Ioniq 5 & 6. With the new Kona EV now reaching dealerships, expect the Korean brand to continue posting record results in the next few months.

But one of the biggest surprises of the month was NIO, which once again hit a record performance — 20,846 registrations. That was thanks to strong deliveries of the ES6 SUV and another solid result from the ET5 sedan/station wagon.

Other brands shining were #16 Toyota(!), which hit a record result of 17,370 units, and #20 XPeng, which seems to be back on track. XPeng got 13,763 registrations, its best result since June 2022. Over half of that volume came from the promising G6 crossover. Despite just being in its 2nd month on the market, it already hit a monthly result of 7,068 registrations. Will XPeng’s take on the Tesla Model Y theme be the one that will save the company? One thing is certain — the crossover has a lot going for it….

Outside the top 20, one highlight was #21 Hozon, with 13,623 registrations, a new year best. Also, Great Wall’s Ora brand had 10,301 registrations, its best result since June 2022, mostly thanks to the good performance of the Good Cat hatchback.

Stellantis hasn’t managed to place any brand in the top 20, with its highest placed brand being Jeep at #22, with just 12,481 registrations. Nevertheless, Opel saved the day (partially), by scoring a year-best result, 10,315 registrations.

In the YTD table, there isn’t much to report regarding the podium. BYD is ahead of Tesla, with the two makes together responsible for more than one third of the global plugin vehicle market.

Far below these two, which are really in a league of their own, you have the hot GAC Aion, which has finally surpassed BMW and is the new NTNB best seller. Don’t expect others to reach the Chinese make anytime soon. It seems this year’s podium is already decided: #1 BYD, #2 Tesla, #3 GAC Aion.

Li Auto’s rise has been paused, staying in 8th, but expect the Chinese brand, without a doubt the hottest startup brand in 2023, to continue shortening the distance to #7 Mercedes.

But the remaining highlights happened in the second half of the table, where Toyota climbed to #16, proving that the giant is slowly awakening. Question is: Is it already too late for Toyota to reach the Big Boys table?

Finally, NIO is rising fast, thanks to another record performance, with the startup make now in #17. Next stop: Toyota’s 16th position?

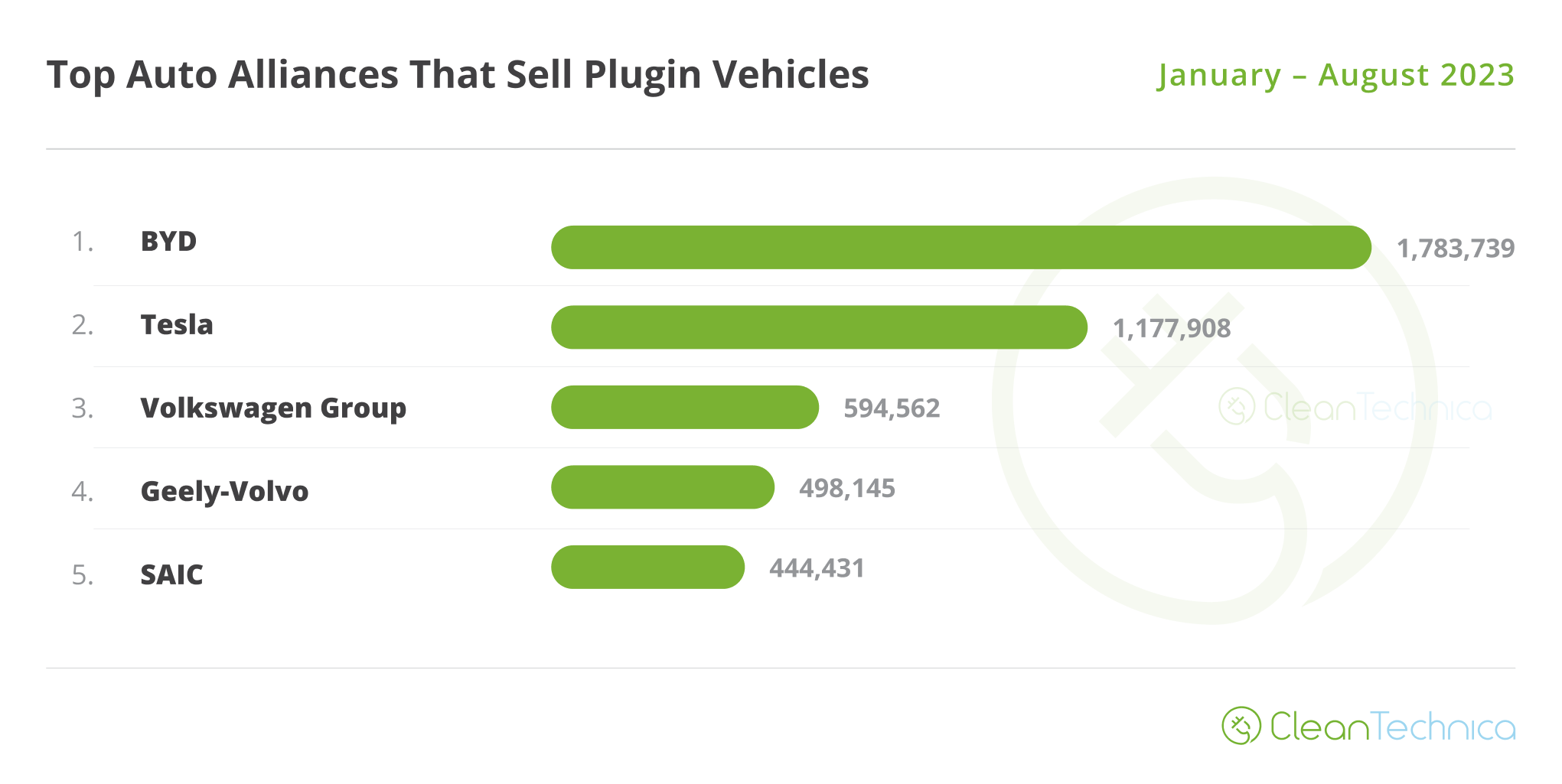

Looking at registrations by OEM, leader BYD was comfortable at 21.8% share, while Tesla was slightly down — to 14.4% share.

3rd place is in the hands of Volkswagen Group (7.3%, down from 7.4%), keeping a good distance from #4 Geely–Volvo (6.1%).

As for #5 SAIC (5.4%, down from 5.6%), the share loss resumed, but consequences aren’t too concerning for it, because #6 Stellantis was also down in August, from 4.7%, to 4.6%.

Below the multinational conglomerate, things are more interesting. While #7 BMW Group (4.1% share) gained a precious 4,000-unit advantage over #8 Hyundai–Kia (also 4.1%), the truth is that rising #9 GAC (4%) is now just 8,000 units behind the German OEM. We could see the Chinese maker jump two positions in September alone!

Looking where the ranking was a year ago, we can see that both the top two brands gained share, 4.9% in the case of BYD and 2% in the case of Tesla. The other beneficiary was Geely–Volvo, which in the meantime surpassed SAIC and added 0.4% share on the way.

On the losers side, Volkswagen lost 1% share YoY, while SAIC dropped almost a third of its share, from 7.9% a year ago to its current 5.4%….

Looking just at BEVs, Tesla remained in the lead with 20.6%, down from 20.9% in June. The US make has a comfortable lead over BYD (15.7%, up from 15.6%), making it unlikely the Chinese automaker will be able to remove Tesla from the BEV throne this year. Next year, however … stay tuned.

In the last place on the podium, Volkswagen Group (7.8%) gained precious ground over SAIC (7.5%, down from 7.7%). Still, expect an entertaining race between these in the remainder of the year.

In 5th we have a position change, former 5th placed Geely–Volvo (5.6%, down from 5.7%) was narrowly surpassed by rising GAC (5.6%, up from 5.5% in July) — without much media attention, it was quickly becoming a force to be reckoned with.

Comparing BEVs to where they were a year ago, things roughly follow the trends in the PEV market — BYD and Tesla were up, SAIC was down, but in this case, Volkswagen Group instead of losing share actually gained 0.5% share YoY, which can only be explained by the fact that the German OEM is ditching PHEVs and becoming a more BEV-based company. Good for you, VW!

A final note on the current domination from BYD and Tesla: I do not expect this to last for many years, because the entry barriers for the EV business are far lower than in the ICE era. I expect a future with a more diverse (and dynamic) automotive landscape, and with some players coming from countries not traditionally associated with the automotive business.

**On the topic of the VW ID.3 price reduction in China, I have a few thoughts on the recent Volkswagen policy change in China:

- There is a fallacy regarding the price difference between EVs in China and in Europe. Yes, part of the difference regards a higher margin from OEMs, but that margin is much smaller than what people think.

- When comparing the European prices of EVs made in China with the prices of the same models in China, we should remember that VAT there is just 13% compared to some 23% in Europe. That alone will increase the price by some 10%, when a model lands in Europe. Add to that the 10% tariff import tax and we already have a 20% price difference between the two markets.

- Add to that some $2,000 in shipping costs, and you have the primary explanations for the price differences between China and Europe.

- For example, the base Tesla Model 3 costs 260,000 yuans in China ($35,800), while in Europe, the same version costs €43,000 ($46,700). Just in extra taxes/tariffs, the same model costs an extra $7,160. Add the aforementioned $2,000 for transportation costs, and the car already costs $44,960 in Europe.

- Which means that Tesla is earning an extra profit of about $1,800 by selling it in Europe instead of China — assuming no other additional costs. Much lower than what many expected.

Support CleanTechnica via Kickstarter

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy