35% Plugin Vehicle Market Share In China! (China EV Sales Report)

Support CleanTechnica's work through a Substack subscription or on Stripe.

Plugin vehicles are all the rage in the Chinese auto market. Plugins scored over half a million sales last month, up 93% year over year (YoY). That pulled the year-to-date (YTD) tally to over 1.9 million units.

Share-wise, with April showing another great performance, plugin vehicles hit 35% market share! Full electrics (BEVs) alone accounted for 24% of the country’s auto sales. This pulled the 2023 share to 33% (23% BEVs), and considering the current growth rate, we can assume that China’s plugin vehicle market share will end around 40% by the end of 2023.

Another measure of the importance of this market is the fact that China alone represented over half of global plugin registrations last month!

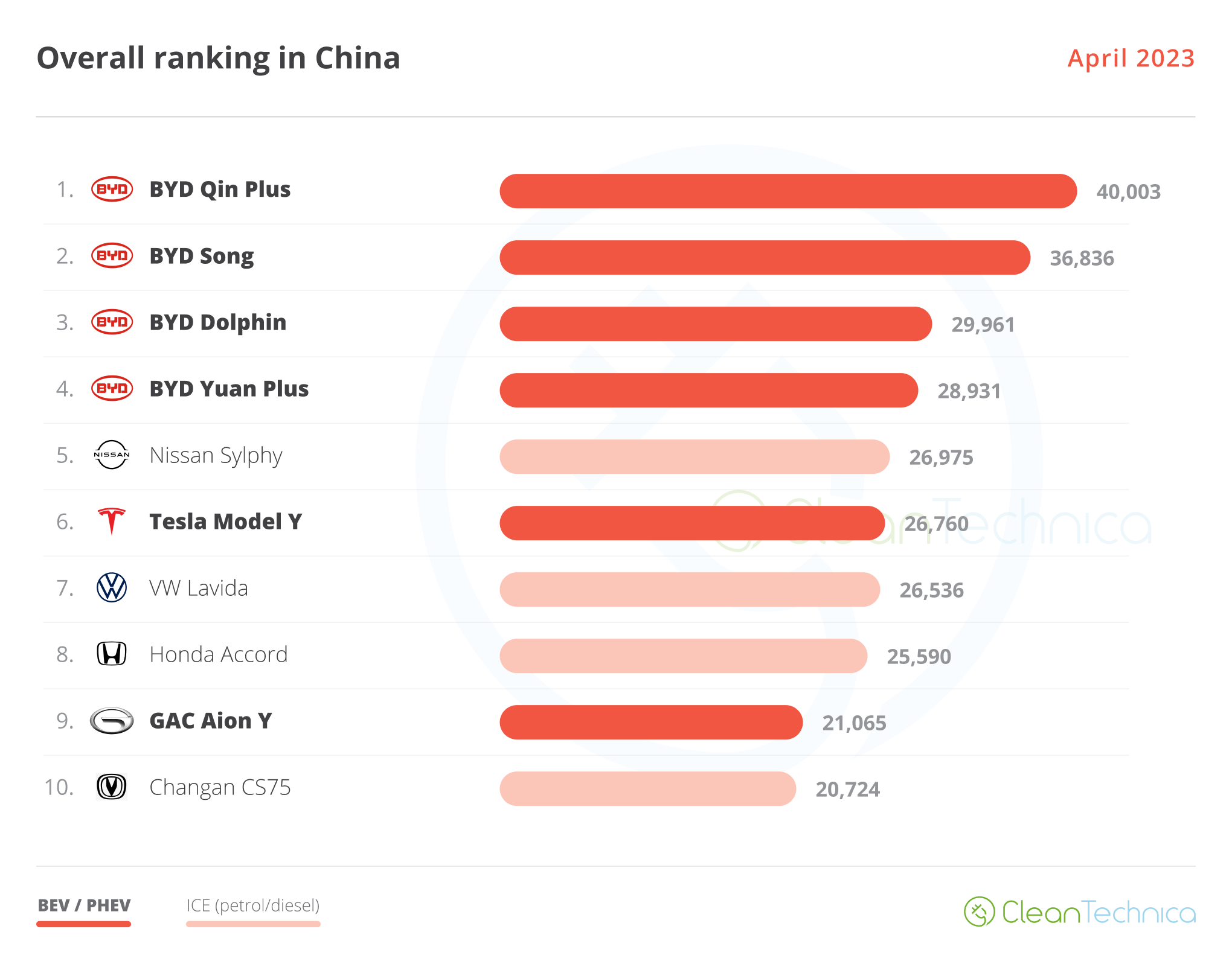

Looking at April’s best sellers in the overall market, we see plugins populating most of the top 10, with 6 plugin models in the overall top 10. In the top 5, the only pure ICE model was the Nissan Sylphy. And to think: in other markets, we celebrate when one EV breaks into the overall top 10….

But looking at the best sellers by category, we see that some still need a heavy dose of electrification:

As we can see, while city cars (A-segment) and the midsize category (D-segment) are heavily electrified, compacts (C-segment) and full size (E-segment) still have some work to do.

As for the B-segment (subcompacts), for some reason, the Chinese aren’t really into this category, so the only volume seller in this category has been the BYD Dolphin. But now the Wuling Bingo is looking to break BYD domination in the category, while the remaining competition is lagging behind.

Here’s more info and commentary on April’s top selling electric models:

#1 — BYD Qin Plus (BEV+PHEV)

Thanks to a recent refresh, and seemingly mandatory price cut, the BYD Qin Plus has surprised many by beating its Song sibling and winning the best seller prize in April. The midsizer reached 40,003 registrations in April, with the BEV version alone scoring 8,718 registrations. This allowed BYD to win all three positions on the overall podium (Volkswagen, take notice). With the recent price drop and prices now starting at 100,000 CNY ($15,000), demand spiked again, despite the strong internal competition (the BYD Seal for the BEV version and the Destroyer 05 for the PHEV version). Expect BYD’s lower priced midsize sedan to continue posting strong results, at the cost of its most expensive siblings. It should have no problem keeping its most direct competitors, the Tesla Model 3 and GAC Aion S, at a safe distance.

#2 — BYD Song (BEV+PHEV)

BYD’s midsize SUV was 2nd in the Chinese automotive market, with BYD’s current star player scoring 36,836 registrations, 4,600 of them belonging to the BEV version. So, will the Song end the year as the best selling model in the Chinese automotive market? Well, it depends on the competition, especially the internal competition. Currently, the Song only has the recently introduced Frigate 07 PHEV as internal competition, but the upcoming Sea Lion (BYD’s take on the Tesla Model Y theme) and the premium car-on-stilts Denza N7 (a car that sits somewhere between the Tesla Model Y and the Zeekr 001) are both set to land this year. This is probably too much competition inside BYD’s midsize SUV portfolio (the Song as the lower priced model, the Frigate 07 & Sea Lion as mid-priced models, and finally the more upmarket Denza N7). Also, the current wave of price cuts, which is spreading through the local market, will be a decisive factor. BYD has just reduced prices of its Song model, just like it did with the Qin Plus, but will this be enough? All of these factors will be decisive for the Song to continue clocking 40,000–50,000 sales/month, a necessary threshold to continue leading the cutthroat Chinese auto market.

#3 — BYD Dolphin

The small-to-compact Dolphin scored 29,961 registrations, a new record. In the past, one could say that the Dolphin had its class all to itself, as its most direct competitors in this category were selling significantly less. The reason for this success? Using a space-efficient interior and competitive specs (not unlike a certain Chevrolet Bolt), the Dolphin adds the cost-saving features of its brand new 3.0 dedicated platform and cost-leading batteries. This success is now going to be tested by the recently introduced Wuling Bingo, which clocked 15,011 registrations in April. The race in the small hatchback category could become an entertaining thing to follow, especially if the upcoming JAC Yiwei 3, said to receive sodium-ion batteries later this year, also becomes a success.

#4 — BYD Yuan Plus

With a record 28,931 registrations last month, BYD’s current star player in export markets is also expanding its sales in the domestic market, allowing it to be 4th in the overall auto market. Will the compact crossover continue to grow, both internally and overseas? Outside China, the answer is a resounding “YES,” with the compact EV just starting its career in several markets and still to land in many more. The answer in its home market is …”Maybe.” Considering the current price war in China and the ever increasing competition (the upcoming Zeekr X being just one of many), I believe BYD will direct production of its crossover to export markets, where competition is less blood thirsty and margins are higher.

#5 — Tesla Model Y

Tesla’s star model got 26,760 registrations, which, considering it was an off-peak month, should be considered a positive result. It seems the price cuts have gone well for the US crossover, with the midsizer being able to run at the same pace as the best of the BYD pack. Watching the Model Y’s Q1 sales on an average quarterly basis, thus removing the valley/peak months factor from Tesla’s performance, the Model Y ended the quarter with a 31,500 units/month average, which is a great result for a foreign model in China. In a time when Chinese automakers are in peak form (just look at the recent Shanghai Auto Show), Tesla is currently the only foreign OEM able to follow the amazing pace of the domestic carmakers.

Looking at the rest of the best seller table, below BYD and Tesla, GAC’s Aion S & Aion Y continue to impress, with the latter inclusively beating its sedan sibling with a record 21,065 registrations. Will GAC’s dynamic duo continue to grow and reach the top spots? That would at least bring some extra color to the current BYD–Tesla domination. To be continued….

Below GAC’s models, we have another duo coming from Wuling, but this isn’t exactly dynamic, because while the 9th spot of the Wuling Bingo is a great start for the small hatchback, the 8th position of the Mini EV is its 3rd worst month ever, as it seems the competition of the cheap and cheerful Geely Panda Mini (#13, with 10,615 units, its third record score in a row) and the arrival of its larger Wuling Bingo brother is making a dent in the sales of the bare-basics Wuling Mini EV. With Wuling recently cutting prices of its Mini EV (throwing out the window the mini profit they made with it…), the make hopes to revive the sales of its smallest and cheapest offering.

In the second half of the table, the highlights were the #14 Denza D9 giant RV large MPV scoring a record 10,526 registrations thanks to record performances from both versions. In #15 we have the Li Xiang L7, the startup’s new full-size 5-seat SUV (the L9/L8/L7 are all full-size SUVs), with the new model crossing into five-digit performances in only its second month on the market (10,486 registrations). It seems the hot startup brand has another winner in its hands.

But the other Li Auto models dropped to 6,000-something performances in April. No doubt, some cannibalization is at play here, but hey, over 20,000 sales per month in the full size category is nothing to feel sad about. After all, that is almost as much as BYD does in that category, adding the Han and Tang together.

Speaking of BYD, not everything is roses in the Shenzhen’s lineup. Last month, neither the Seal (6,323 units) nor the Destroyer 05 (5,133 units) reached the top 20. On the other hand, the #16 Frigate 07 continues to ramp up production, with the plugin hybrid SUV reaching 10,042 deliveries last month.

Outside the top 20, the highlights were the recovery of some models, like the Zeekr 001 (6,463 units), which could return to the table soon — once the new Qilin battery versions reach significant production. The VW ID.4 (5,240 units) had its best score all year, so there might be some hope for the German crossover after all. Meanwhile, Leap Motor’s C11 midsize SUV scored a record 6,146 registrations, no doubt helped by the introduction of a range-extended version (3,677 units in April) that is now sold along the regular BEV version.

Last, but not the least, the last days of the month saw the landing of the much-hyped BYD Seagull, which had 1,500 registrations in those few days, no doubt demonstration units. It will be interesting to look at May’s volumes in order to see if its first volume month will already make an impact in the table.

The 20 Best Selling Electric Vehicles in China — January–April 2023

Looking at the 2023 ranking, the leading BYD Song is well above the competition, with the #2 Tesla Model Y resisting quite handily the #3 BYD Qin Plus’ strong month.

Below the podium, the highlights were the BYD Dolphin reaching the 5th position, switching places with the Wuling Mini EV and putting four BYDs in the top five positions! The GAC Aion Y was up one spot, to #10, an impressive standing for the compact MPV-disguised-as-a-crossover.

In the second half of the table, the highlights are the Geely Panda Mini, which jumped four positions to #14, and the BYD Frigate 07 also going up four spots, to #15. A few positions below, the midsized Changan SL03 was up one spot, to #19.

Finally, in #21, we now have the Wuling Bingo, which should join the table in May, with the question being: How high will it get by year end? Top 10?

Top Selling Auto Brands & Auto Groups in Chinese EV Market

Looking at the auto brand ranking, there’s no major news. BYD (35.7%, down from 36.4%) remains stable in its leadership position and is looking to win its 10th plugin automaker title this year, while Tesla (9.3%, down from 10%) is stable in second place.

After a long period of bleeding sales, the SGMW joint venture is starting to benefit from the Bingo-effect (having stopped the trend of losing share) by remaining with 5.9% share in April, but that wasn’t enough to stop the rising GAC Aion (6.3%, up 0.4%) from taking its bronze medal position. Will we see SGMW retake the position in May?

Finally, #5 Changan (4.3%, down from 4.5%) is in 5th, but has lost ground over rising #6 Li Auto (4.1%, up from 3.9%). Will we see the startup reach the 5th position in May? (Hint: May’s partial results points that way.)

Looking at OEMs/automotive groups/alliances, BYD is comfortably leading with 38.1% share of the market, while #2 Tesla (9.3%) also remains stable. With the SAIC mothership still in crisis, the new Wuling Bingo wasn’t enough to stop the current sales bleed — the Shanghai-based OEM once again lost share (7.6%, down from 7.8%).

If SAIC doesn’t stop the sales bleed soon, those behind it will surely surpass it, as the most immediate competitors are consistently rising: #4 GAC profited from the brilliant performances of its dynamic duo to jump from 6.1% to 6.6% in April; one step down, Geely–Volvo continues on the rise thanks to the recent success of the Geely Panda Mini (5.3%, up from 5%) .

With #6 Changan losing ground (4.6%, down 0.3%), Geely can rest on its laurels. The “Chinese Volkswagen Group” is still performing way better than the actual Volkswagen Group. Still, Volkswagen Group is looking to recover relevance in China, having recently recovered some share. In April, it saw its share grow from 2.6% to 2.8%. Which is still less than what the #8 Tesla Model 3 has….

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy