34% Plugin Vehicle Market Share In China — March 2023 Sales Report

Support CleanTechnica's work through a Substack subscription, on Patreon, or on Stripe. Help us produce all of the high-quality, original content we publish week after week despite the challenges of content-scraping AI, antisocial media, inflation, and other hurdles.

Plugin vehicles are all the rage in the Chinese auto market. Plugins scored over half a million sales last month, up 23% year over year (YoY), pulling the year-to-date (YTD) tally to over 1.3 million units.

Share-wise, with March showing another great performance, plugin vehicles hit 34% market share! Full electrics (BEVs) alone accounted for 24% of the country’s auto sales. This pulled the 2023 share to 33% (22% BEV), and considering the current growth rate, we can assume that the country’s plugin vehicle market share will end close to 40% by the end of next quarter.

Another measure of the importance of this market is the fact that China alone represented over half of global plugin registrations last month!

Looking at March’s best sellers in the overall market, we see how fast plugins are populating the top 10, with eight plugin models in the overall top 10, and only the #7 VW Lavida, and #8 Nissan Sylphy being pure ICE models. (Not long ago, these two models fought for #1, but now are barely able to keep a top 10 position.)

And to think: in other markets, we celebrate when one EV breaks into the overall top 10….

But looking at the best sellers by category, we see that some still need a heavy dose of electrification:

As we can see, while city cars (A-Segment) and the midsize category (D-Segment) are heavily electrified, compacts (C-Segment) and full size (E-Segment) still have some work to do.

As for the B-Segment (subcompacts), for some reason, the Chinese aren’t really into this category, so the only volume seller in this category is the BYD Dolphin. A golden opportunity for the upcoming Wuling Bingo? At least there aren’t that many competitors to compete against….

Here’s more info and commentary on February’s top selling electric models:

#1 — Tesla Model Y

Tesla’s star model got 54,937 registrations, a new record, which allowed it to win the best seller status in the overall ranking for the third time (after wins in June and September 2022). It seems the price cuts have gone well for the US crossover, with the midsizer being able to beat the BYD pack. Still, watching Model Y sales on an average quarterly basis, thus removing the valley/peak months factor from Tesla’s performance, the Model Y ended the quarter with a 31,500 units/month average, which is far from the 40,000-plus units/month of the leader BYD Song, but allows it to remain ahead of the remaining BYD pack. In a time where Chinese automakers are in peak form (just look at the recent Shanghai Auto Show), Tesla is currently the only foreign OEM able to follow the amazing pace of the domestic carmakers.

#2 — BYD Qin Plus (BEV+PHEV)

Thanks to a recent refresh, and the mandatory price cut, the BYD Qin Plus has surprised many by beating its Song sibling and winning silver in March. The midsizer reached 40,215 registrations in March, with the BEV version alone scoring 8,905 registrations. This placed it in 2nd in the overall market, allowing BYD to place two models on last month’s overall podium (Volkswagen, take notice). With the recent price drop and prices now starting at 100,000 CNY ($15,000), demand spiked again, despite the strong internal competition — the BYD Seal for the BEV version and the Destroyer 05 for the PHEV version. Expect BYD’s lower priced midsize sedan to continue posting strong results, at the cost of its most expensive siblings. It should have no problem keeping its most direct competitors, the Tesla Model 3 and GAC Aion S, at a safe distance.

#3 — BYD Song (BEV+PHEV)

BYD’s midsize SUV has dropped to 3rd in the Chinese automotive market, surpassed by the peak month of its rival Tesla Model Y, and by its sibling Qin Plus, which benefitted from a recent refresh and a price cut. BYD’s current star player scored 40,114 registrations, 6,050 of them belonging to the BEV version. So, will the Song end the year as the best selling model in the Chinese automotive market? Well, it depends on the competition, especially the internal competition. Currently, the Song only has the recently introduced Frigate 07 PHEV as internal competition, but the upcoming Sea Lion (BYD’s take on the Tesla Model Y theme) and the premium car-on-stilts Denza N7 (a car that sits somewhere between the Tesla Model Y and the Zeekr 001) are both set to land this year. This is probably too much competition inside BYD’s midsize SUV portfolio (the Song as the lower priced model, the Frigate 07 & Sea Lion as mid-priced models, and finally the more upmarket Denza N7). Also, the current wave of price cuts, which is spreading through the local market, will be a decisive factor. BYD has margin to reduce prices, just like it did with the Qin Plus, but by how much? All of these factors will be decisive for the Song to continue clocking 40,000–50,000 sales/month, a necessary threshold to continue leading the cutthroat Chinese auto market.

#4 — BYD Yuan Plus

With a record 27,907 registrations last month, BYD’s current star player in export markets is also expanding its sales in the domestic market, allowing it to be 4th in the overall auto market. Will the compact crossover continue to grow, both internally and overseas? If outside China, the answer is a resounding “YES,” with the compact EV just starting its career in several markets and still to land in many more. The answer in its home market is …”Maybe.” Considering the current price war in China and the ever increasing competition (the upcoming Zeekr X being just one of many), I believe BYD will direct production of its crossover to export markets, where competition is far less bloodthirsty and margins are higher.

#5 — BYD Dolphin

Temporarily at the bottom of the BYD lineup (the small Seagull is set to land soon), the small-to-compact Dolphin scored 27,687 registrations, a new record. One can say that the Dolphin has this class all to itself, as its most direct competitors in this category are selling four times fewer sales (the #2 Trumpchi GS3 — an ICE model — had 5,946 sales). The reason for this success? Using a space-efficient interior and competitive specs (not unlike a certain Chevrolet Bolt), the Dolphin adds the cost-saving features of its brand new 3.0 dedicated platform and cost-leading batteries. With more news about the Euro-spec version now available, the price was something of a disappointment — starting at 30,000 euros — but the specs, especially the size, which grew to a C-segment car (a VW ID.3/MG 4 fighter), were a surprise. Maybe they want to leave space in Europe for the upcoming Seagull? Will that be the true EV for the masses?

Looking at the rest of the best seller table, for once the highlight does not come from BYD or Tesla, but from GAC’s Aion S. The midsizer from Guangzhou is on a record streak, hitting 26,392 registrations, its third record in a row. It’s an impressive performance, especially considering that the sedan already has a few years on its back, allowing it to end the month in 6th. Does this mean the veteran sedan can keep pace with the Tesla Model 3 and BYD’s Qin Plus throughout the rest of the year? That would at least bring some extra color to the current BYD–Tesla domination. To be continued….

The Aion Y, the other half of GAC’s dynamic duo, also shone brightly, ending March in #9 with 13,267 registrations. Another highlight in the table is the Geely Panda Mini, the OEM’s answer to the Wuling Mini EV, which ended the month in #12 with 10,550 registrations in only its third month on the market.

This is a Wuling Mini EV–beating performance, because SAIC’s tiny EV had 9,150 units in its 3rd month on the market. Has the little Wuling finally found its match? One thing is for certain: with the SGMW best seller only reaching the 7th spot in March, with a disappointing 23,159 registrations, it sure looks like the cheaper and more cheerful stance of Geely’s Panda Mini is making a dent in the sales of the more bare-basics Wuling Mini EV.

Elsewhere, we see the #13 Denza D9 giant RV large MPV scoring a record 10,398 registrations thanks to record performances from both versions. In #15 we have the return of the sleek Changan SL03, mostly thanks to a record performance from the PHEV version, which had a 8,500 registrations in March. Still on the trend of models with both BEV and PHEV versions, we have a surprise in #18, with the Buick(!) Velite 6 reaching the best sellers table. The station wagon (imagine that, a Buick station wagon!!! :o) reached such heights thanks to a record performance from its PHEV version (5,409 units), allowing it to be the third foreign model in the table.

Finally, let’s give a nod to the return of the BAIC EU-Series to the table, in #16. It seems Beijing Auto has returned from a long hibernation period. Meanwhile, the Li Xiang L7, the startup’s new full-size 5-seat SUV (the L9/L8/L7 are all full-size SUVs) has shot up to #17 right in its landing month — so it seems the hot startup brand has another winner in its hands.

But the L7 was Li’s only model in the top 20, because the other two models dropped to 6,000-something performances in March. No doubt, some cannibalization is at play here, but hey, 20,000 sales per month in the full size category is nothing to feel sad about. After all, that is almost as much as BYD does in that category, adding the Han and Tang together.

Speaking of BYD, not everything is roses in the Shenzhen’s lineup. Last month, neither the Seal (5,201 units) nor the Destroyer 05 (4,136 units) reached the top 20. In fact, the BEV model had its worst score in 6 months, while the PHEV model had its worst performance in 11 months. … Time for a price cut?

Outside the top 20, the highlight is the Smart #1 reaching a record 5,911 registrations, with the Geely and Mercedes lovechild experiencing a surprising success in a market where the Smart brand has no brand recognition. This bodes well for the success of the model in Europe, and for the upcoming (and attractive) SUV-coupé-that’s-really-a-hatchback #3. It also provides a good omen for the career of the Zeekr X, another on trend genre-bending model. The Zeekr X is probably the most forward looking model, spec and styling wise, that the future Tesla compact model will have to deal with. Another SEA-based model set to land this year is the Volvo EX30. That makes four competitive compact EVs from the Geely platform, all ready to score some serious sales volumes.

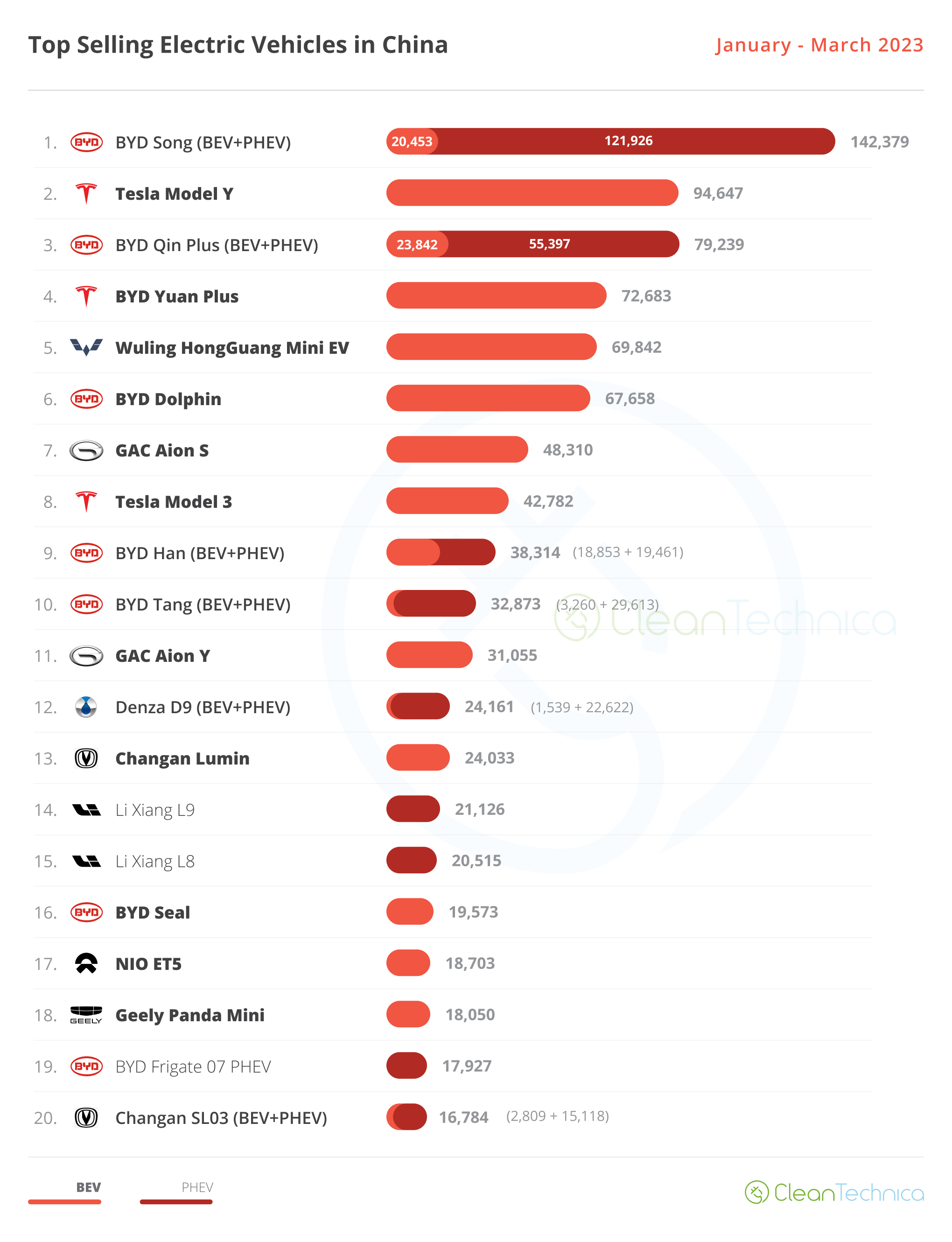

The 20 Best Selling Electric Vehicles in China — January–March 2023

Looking at the 2023 ranking, the leading BYD Song is well above the competition, resisting quite handily the Tesla Model Y’s peak month. Still, it was a positive month for the US model, which jumped two positions into the runner-up spot. The last place on the podium also has a new face, with the BYD Qin Plus benefitting from a slow month from the Wuling Mini EV to reach the bronze medal position.

Below the podium, the highlights are once again GAC’s Aion S, which was up to 7th, and the Tesla Model 3 profiting from its March peak to reach the 8th position.

In the second half of the table, the highlights are the Denza D9, which jumped four positions to #12, and the Changan Lumin going up two spots to #13. Highlighting Changan’s good moment, the midsize SL03 joined the table in #20. Will the Changan sedan be able to run with the category’s best?

Finally, in #18, we now have the Geely Panda Mini, which joined the table and is now looking to surpass the category runner-up, the Changan Lumin, and hoping to reach the leader Wuling Mini EV sometime in the future.

Looking at the auto brand ranking, there’s no major news. BYD (36.4%, down from 38.8%) remains stable in its leadership position, and not only on the plugin table. In the mainstream market, it again beat Volkswagen in March, but more important are the growth contrasts between the top 5 best selling brands: while the #1 BYD and #5 Tesla are growing fast (+67% for the Chinese make, +28% for the US brand), the best selling legacy OEMs (#2 Volkswagen and #3 Toyota) are in downward spirals (both -22%) and in one case in a life threatening spot (e.g., #4 Honda, down 48% YoY).

The Shenzhen automaker is looking to win its 10th plugin automaker title this year, while Tesla (10%, up from 7.6%) is stable in second place.

The SGMW joint venture slipped again (5.9%, down from 6.6%) and now has the rising GAC Aion (5.9%, up 0.8%) breathing down its neck. Will we see a position change here in April?

Finally, Changan (4.5%, up from 4.4%) is stable in 5th, gaining distance over the #6 Li Auto (3.9%).

Looking at OEMs/automotive groups/alliances, BYD is comfortably leading, with 38.1% share of the market. SAIC (7.8%, down from 8.4%) was again displaced to 3rd due to the rise of Tesla (10%). With the SAIC mothership still in crisis, and the Wuling Mini EV now starting to slow down, the new Wuling Bingo needs to be a success in order to stop the current sales bleeding.

If SAIC doesn’t stop the sales bleed soon, those behind it will surely surpass it, as the most immediate competitors are consistently rising: #4 GAC profits from the brilliant performances of its dynamic duo to jump from 5.4% to 6.1% in March, one step down, Geely–Volvo (5%, up from 4.9%) continues on the rise, thanks to the recent success of the Geely Panda Mini.

With #6 Changan (4.9%, up 0.1%) not too far behind, Geely can’t rest on its laurels. Still, the Chinese Volkswagen Group is still performing better than the original. Volkswagen Group is now nearly irrelevant in China (2.6%, up from 2.5%) — so much so that BMW Group is on its way to surpassing it and becoming the second best selling foreign OEM in China.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy