World BEV Sales Now 10% Of World Auto Sales

Support CleanTechnica's work through a Substack subscription or on Stripe.

Global plugin vehicle registrations were up 49% in February 2023 compared to February 2022. There were 812,000 registrations, representing 14% share (9.7% BEV share) of the overall auto market. This means that the global automotive market is in the Electric Disruption Zone. Year to date, the market share is now at 13% (8.7% BEV).

Fully electric vehicles (BEVs) represented 70% of plugin registrations in February, slightly above the year-to-date tally (68%).

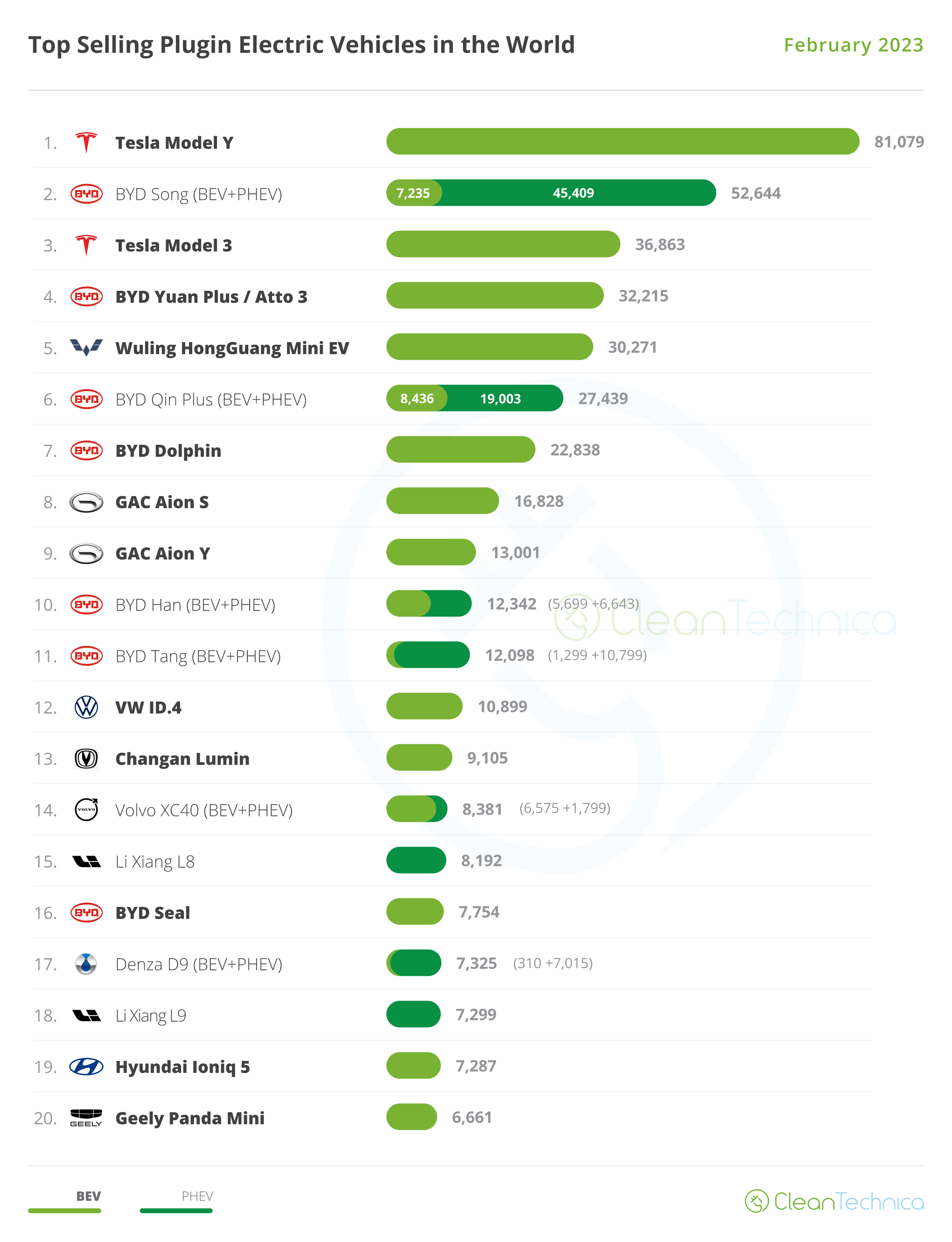

20 Best Selling EV Models in the World in February

Looking at February best sellers, there were no surprises on the podium, with the 2022 podium being replicated once again. The Tesla Model Y was high above everyone else, and the BYD Song ended above the bronze medalist Tesla Model 3.

Just off the podium, the highlight is the #4 BYD Yuan Plus, aka Atto 3 in many export markets. The compact crossover scored a record month in February, with 32,215 registrations. That’s especially thanks to increasing volumes in markets outside its native China.

But the BYD EV wasn’t the only model scoring a record performance, as the #8 GAC Aion S surprised everyone with a record 16,828 registrations. In fact, highlighting GAC’s positive month, the Guangzhou make placed its other star player, the Aion Y, in the 9th. It was the 3rd brand to have multiple models on the top 10.

The second half of the table saw the cutesy Changan Lumin return to form, ending the month at #13 with 9,105 registrations. But the little Changan EV, and everyone else in the city car scene in China, will have to deal with a new, strong competitor, as Geely’s Panda Mini EV just had its first volume month in February and jumped immediately to #20 thanks to 6,661 registrations. Expect Geely’s take on the Wuling Mini EV (even the name is similar) to start becoming a familiar face in the ranking.

On the legacy model front, the #12 VW ID.4 is suffering from low numbers in China, which allowed the #14 Volvo XC40 to come closer. For now, the German crossover is still safe, having ended some 2,500 units ahead of the Swede, but it is a sign that the VW EV does not have its legacy best seller status assured.

An interesting fact of the February top 20 is that there are five full size models in the table and all are Chinese. Not one legacy model is close to casting a shadow over the BYD, Denza, and Li Auto models, and all are set to have six-figure full-year numbers in 2023.

If someone wants to be relevant at the higher end of the market, monthly 5-digit scores are a must, and this goes for everyone — be they legacy OEMs (we’re looking at you, Mercedes EQE), other Chinese automakers (XPeng? NIO?), or even Tesla.

Speaking of BYD, the Shenzhen automaker is ruling several categories at once. The #7 BYD Dolphin is the undisputed leader of its segment, the only B-segment/subcompact in last month’s top 20. The #4 Yuan Plus/Atto 3 is almost tripling the sales of its most direct competitor in the compact segment (#12 VW ID.4). Meanwhile, in the full size category, BYD has a #1 plus #2 lead — with the Han sedan in the lead, followed by the Tang SUV.

Outside the top 20, the highlights are the recently introduced BYD Frigate 07 PHEV model, reaching a record 6,429 registrations and looking for a top 20 presence soon, and the Chevrolet Bolt EUV profiting from the new incentives scheme in the USA to score a record 5,636 result.

Other models on the rise are the NIO ET5 (6,471 registrations), providing a much needed volume boost for the startup brand, and the VW ID.3 (6,444 units) and Audi Q4 e-tron (6,012) coming close to top 20 positions.

Top 20 EV Models in January & February

In the year-to-date (YTD) table, there was nothing new on the podium, with the Tesla Model Y still ruling supreme above the BYD Song and Tesla Model 3.

The first position change happened with the Wuling Mini EV recovering from its slow start in 2023 and climbing to 5th.

The BYD Qin Plus was up one position, to 7th. The most impressive performances, though, belonged to GAC’s dynamic duo, with the Aion S jumping nine spots … to #9 … while the Aion Y surged to #12.

In the second half of the table, the highlight was the rise of the Changan Lumin to #17, while the #11 VW ID.4 remained the best selling legacy model. The #13 Volvo XC40 is not too far from the German model, though.

Top Selling Brands

In February, BYD’s strong start of the year had another chapter, clocking around 184,000 registrations. It is expected the Shenzhen automaker is pushing some 200,000-plus units in March, which might not be enough to beat Tesla in its peak month, but will allow it to keep the YTD lead.

Below the top two galactics, Chinese automakers were on the rise. SGMW was 3rd, with 35,082 registrations, thanks to the delivery ramp-up of the Wuling Mini EV. Meanwhile, GAC benefitted from another brilliant performance from its dynamic duo, the Aion S & Y, to reach the 4th position in February.

Geely had a positive month thanks to the new Panda Mini EV, allowing it to reach the #9 position, just behind its Swedish arm, Volvo, which was at #8.

The best selling legacy US brand showed up in #18, and the bearer of the honor wasn’t Ford (which ended the month in #22) or Chevrolet (which was 21st in February), but was Jeep. Jeep is profiting from the rise of Wrangler PHEV sales (thanks in no small part to IRA incentives) and the volume deliveries of the Grand Cherokee PHEV. It beat not only its US competition, but also its Stellantis siblings, like the French Peugeot, #19 in February, which lost to the US company by some 300 units.

In the YTD table, there wasn’t much to report regarding the podium. BYD is ahead of Tesla, with the two makes together responsible for more than one third of the global plugin market.

Far below these two, which are really in a league of their own, BMW is still in the 3rd spot, but the rising SGMW joint venture is closing in and should surpass it in March.

GAC jumped seven positions, to 7th, and could climb higher in the next few months, something that could also be said about Geely, which was up five spots to #12. Should the little, cute Panda Mini EV prove to be a success, expect the Chinese automaker to remain in the top 10 in the foreseeable future.

In the second half of the table, NIO jumped three positions, to #16, but it is still far from the Chinese new blood #10 Li Auto. Still in this category of brands, we should highlight Hozon returning to the table, in #20, thanks to the recovery of the small Neta V.

Finally, a reference goes out to Jeep, which thanks to a strong start of the year was up to #17. The US brand is now a Stellantis star player, with the go-anywhere brand now having a 1,500 advance over the #21 Peugeot.

Top Selling OEMs for EV Sales

Looking at registrations by OEM, leader BYD increased its share slightly, from 22.7% to 23.2%, while Tesla was down slightly, to 15% share (it had 15.2% a month ago). Expect the US brand to recover some share in March thanks to the usual end-of-quarter peak, but that won’t be enough to endanger BYD’s leadership.

3rd place is still in the hands of Volkswagen Group, but with the German OEM losing 0.3% on the way (7.5% a month ago, 7.2% now) and #4 Geely–Volvo on the rise (6.2%, up from 5.8%), the Chinese Volkswagen Group is closing in on the original. We might even see the Apprentice overcoming the Master this year.

The media in general like to compare Volkswagen Group to Tesla, but that is really comparing apples to oranges, as currently the two play in different leagues and have different strong points. As Pulp Fiction’s Jules character would say: “It ain’t the same league. It ain’t even the same ****ing sport!”

Not only do they play in different sales levels, but Tesla is closer in concept to what BYD does (10 years ago, I was saying BYD was the Chinese Tesla…). The closest OEM in concept to Volkswagen Group is, along with Stellantis, Geely–Volvo. So, why aren’t Tesla vs. BYD and Volkswagen Group vs. Geely–Volvo being compared more often?

SAIC is 5th with 5.6%, up from 5.1%. The Shanghai OEM secured its position thanks to a good February from the Wuling Mini EV, while below it, Stellantis (4.7%) recovered the #6 spot from BMW Group, which dropped from 4.8% in January to its current 4.3%.

Looking just at BEVs, Tesla remained in the lead, with 22%. The US make has a comfortable lead over BYD (16%), making it unlikely the Chinese automaker will be able to remove Tesla from the BEV throne this year. Better luck next year?

The last place on the podium saw a position change, with a rising SAIC (7.8%, up from 6.9%) surpassing Volkswagen Group (7.3%, down a half percentage point).

In 5th we have Geely–Volvo, with 5.6%, up from 5.1%. The Chinese OEM is looking to reach #4 Volkswagen Group, but still has a ways to climb.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy