20% Of New Cars In Europe Have A Plug!

Support CleanTechnica's work through a Substack subscription or on Stripe.

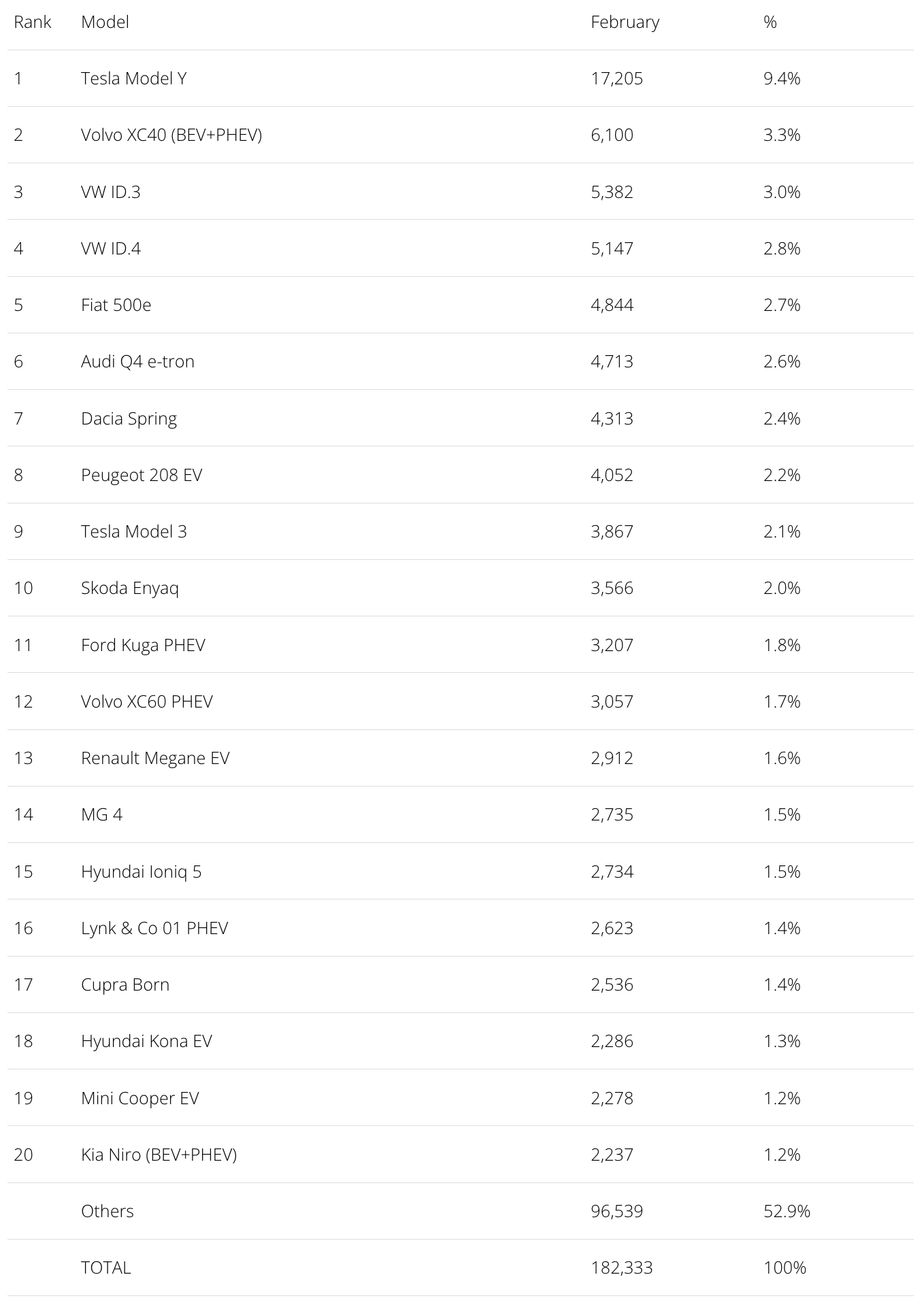

Some 182,000 plugin vehicles were registered in February in Europe — which is +14% year over year (YoY). Unfortunately, the overall market grew almost as fast, +12%, to 902,775 units, leaving the market share close the where it was 12 months ago. Last month’s plugin vehicle share of the overall European auto market was 20% (13% full electrics/BEVs). That result pulled the 2023 plugin vehicle (PEV) share to 19% (12% for BEVs alone).

BEVs (+31% YoY) keep gaining momentum, while PHEVs (-8%) are still suffering from the loss of incentives in a number of markets at the end of last year, allowing pure electrics to represent almost two thirds of plugin registrations last month (65% vs. 35%), a stark departure compared to what happened at the same time last year (57% vs. 43%).

Now, let’s look closer at February’s plugin top 5:

#1 Tesla Model Y — It was another good month for Tesla’s crossover. In February, the midsizer had 17,205 registrations, a number that no doubt benefited from the recent price cuts, and also from the fact that the Model Y is one of the few EVs that has a balanced supply and demand ratio, unlike other models*, allowing quick delivery for anyone interested in buying one. Regarding last month’s performance, the Model Y’s main markets were Germany (6,442 units), France (2,485), EV-loving Norway (1,271), Italy (1,114), and Denmark (1,018). (*It came to my knowledge this week that BMW has an average waiting list for their EVs of around 12 months! A full year!!!)

#2 Volvo XC40 (BEV+PHEV) — The compact Swede is a sure value in the EV arena, and with the BEV version being the main driver of growth (4,409 units), Volvo’s SUV was in 2nd place last month, only behind the galactic Tesla Model Y. The XC40 doesn’t really stand out on any item in particular, but it also doesn’t have weak points, which contributes to its continued success. In February, it had 6,100 registrations, with XC40 sales distribution being evenly distributed across several markets. Its main markets were: Sweden (835 units), Belgium (756), Germany (654), and the Netherlands (683).

#3 VW ID.3 — After a tough 2022, the compact Volkswagen is coming back to life, having earned a bronze medal in February thanks to 5,382 registrations. With the restyling giving it a (slightly) more purposeful look, losing a bit of its “happy puppy” look, along with better interior materials, the German hatchback is looking to replicate the VW Golf’s decades-old success recipe: Not especially good or bad at anything, and a design that doesn’t scare anyone. It now only needs to have a pragmatic, no-nonsense interior like the VW Golf of the good ol’ days. … If those VW Golfs of the past were a political party, they would be a centrist party, looking to house as many voters as possible under its umbrella. (But then again, under current political polarization globally, pragmatic centrists are not really fashionable. … Is that the reason why the VW Golf is losing sales?) But i digress, back to the ID.3’s February performance. The main markets were its domestic market (1,898 units), the UK (650), Norway (535), and France, where the ID.3 got a meritable 445 registrations.

#4 VW ID.4 — Volkswagen’s crossover this time played the supporting role to the ID.3, ending the month in 4th with 5,147 sales. Europe is just one piece in the crossover puzzle of becoming the best selling legacy automaker EV on the global stage, so beating its ID.3 sibling in Europe isn’t really a priority. Speaking of the ID.3, like its smaller sibling, Germany was the model’s biggest market, with 1,599 sales, followed by Sweden (718 sales) and Ireland(!), where the German crossover has really caught on, being #1 in the overall market.

#5 Fiat 500e — The little Italian had a strong February, logging 4,844 deliveries. With wrinkles showing up on the competition (VW e-Up, Smart Fortwo EV, Renault Twingo EV…) and the Dacia Spring appealing to a more cost-sensitive customer base, the Fiat EV won’t have serious competition for the near future. Last month, its main markets were France (1,919 units), Germany (1,183 units), and its native Italy (538 units).

Looking at the rest of the February table, the surprises were the return to form of the Tesla Model 3 (9th, with 3,867 sales) and the Peugeot 208 EV (8th, with 4,052 sales). Expect the US sedan to experience a peak result next month, most likely reaching a podium position in March. The French hatchback, meanwhile, is looking to recover lost time and benefit from revised specs to return to top positions in the next few months.

Moving on, the #11 Ford Kuga PHEV was the best selling PHEV in the table, with 3,207 registrations, but this time the Ford crossover had to sweat to earn the title, because the #12 Volvo XC60 PHEV (3,057 registrations) ended just 150 units behind. This strong performance coming from the Swedish SUV is a good omen for the Volvo EX60, the Swede’s much awaited midsize BEV, set to land in 2024.

Two other impressive performances come from the value for money king, the MG 4, getting to #14 with 2,735 registrations, and the Lynk & Co 01 PHEV showing up in #16, with 2,623 registrations. The Cupra Born also joined the table this month, in 17th, with the spicy Spaniard being the 5th MEB-platform EV in the top 20. It joins the #3 VW ID.3, #4 VW ID.4, #6 Audi Q4 e-tron, and #10 Skoda Enyaq.

Below the top 20, there were a few highlights, like the new Audi Q8 e-tron + old e-tron keeping the full size leadership position with 2,149 registrations, well above the category runner-up Porsche Taycan (1,102 units) and the #3 Mercedes EQE (1,015 units). For once, the three-pointed-star sedan seems to be going somewhere, so will we see it (at least) become the category best selling sedan?

Another highlight is the Toyota bZ4X registering 1,235 units last month. It looks like the Japanese SUV is finally getting its act together and ramping up production. Now the question is: How high will Toyota want to go with its production output?

Looking at the 2023 ranking, the Tesla Model Y consolidated its strong start to the year, now having twice as many deliveries as the runner-up Volvo XC40. So, one can say that the 2023 best seller title has already found an owner.

In the last place on the podium, we now find the VW ID.3, which was up two positions in February. Its larger sibling, the ID.4, also had a positive month, climbing to 5th. With the Audi Q4 e-tron in 6th, we now have three Volkswagen Group models in the top 6 positions.

The Peugeot 208 EV also jumped positions, up to #8, being by far the leader of the B-segment/subcompact class.

The PHEV title is for now in the hands of the #10 Ford Kuga PHEV. But the #11 Volvo XC60 PHEV is fewer than 500 units behind, so it looks as if the Ford crossover will need to beat the Swede in a close race in order to retain its title. It seems Ford’s walk in the park days in the PHEV category have ended….

Elsewhere, the main news was the rise of two models, with the #17 MG 4 and #18 Audi Q8 e-tron/e-tron combo both climbing one position.

Finally, we have two returns to the table. The Tesla Model 3 showed up in #14, with Tesla’s sedan now looking for a position in the top 5, while the Cupra Born joined the table in #20, thus becoming the 6th Volkswagen Group model in the table.

In the automaker ranking, the Battle for Europe is very much ON. Tesla jumped from 5th to 1st, thanks to a significant increase in its market share — from 6.2% in January to its current 9%. Meanwhile, Volkswagen, not wanting to let the leadership of its home market go to its American competitor, was also up, in this case from 4th to 2nd after having increased its share from 7.7% to 8.3%. Expect both models to increase their share again in March, as both will do their best to end the year in the #1 position. This will be fun to watch….

In the midst of this deep reshape of the top 5, Mercedes (8.1%) held onto its #3 spot, thanks to good performances across its extensive lineup. The EQA got 2,053 registrations, the EQB 1,328 registrations, and the new GLC PHEV 1,718 registrations.

The big losers of the month were #4 BMW (7.9%, down from 8.6%) and #5 Volvo (7.4%, down from 7.8%), with both makes being kicked off of the podium in February.

The next step down, #6 Audi (6%) is still far away, so both BMW and Volvo can rest knowing they will continue to be in the top 5 in the near future.

Arranging things by automotive group, Volkswagen Group is ahead with 20.8% share, well above Stellantis (14.4%). The runner-up multinational conglomerate nonetheless increased the distance between itself and the current bronze medalist, Geely–Volvo (10.2%, down from 10.7%). Meanwhile, #4 BMW Group (9.5%) is not far away. Will we see a position change here in March?

Or maybe … could it be the case that #5 Tesla (9%) ends up surpassing both Geely and BMW in March? Depending on the size of the “Tesla high tide,” that could very well be the case!

And let’s not forget that Mercedes-Benz Group (9%) is just 60 units behind Tesla, so it, too, could cause a surprise next month.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy