33% Plugin Vehicle Market Share In China — February 2023 Sales Report

Support CleanTechnica's work through a Substack subscription, on Patreon, or on Stripe. Help us produce all of the high-quality, original content we publish week after week despite the challenges of content-scraping AI, antisocial media, inflation, and other hurdles.

Plugin vehicles are all the rage in the Chinese auto market. Even in one of the slowest months of the year, plugins scored almost half a million sales, up 56% year over year (YoY).

This pulls the year-to-date (YTD) tally to close to 800,000 units, and with March set to be another strong month, we might have 1.5 million registrations by the end of Q1.

Share-wise, with February showing another great performance, plugin vehicles hit 33% market share! Full electrics (BEVs) alone accounted for 22% of the country’s auto sales. This pulled the 2023 share to 30% (20% BEV), and considering that the last month of the quarter is usually a strong month, we can assume that the country’s plugin vehicle market share will end around the 33% mark in Q1, and the first half of the year should see it already close to 40%.

Another measure of the importance of this market is the fact that China alone represented over half of global plugin registrations last month!

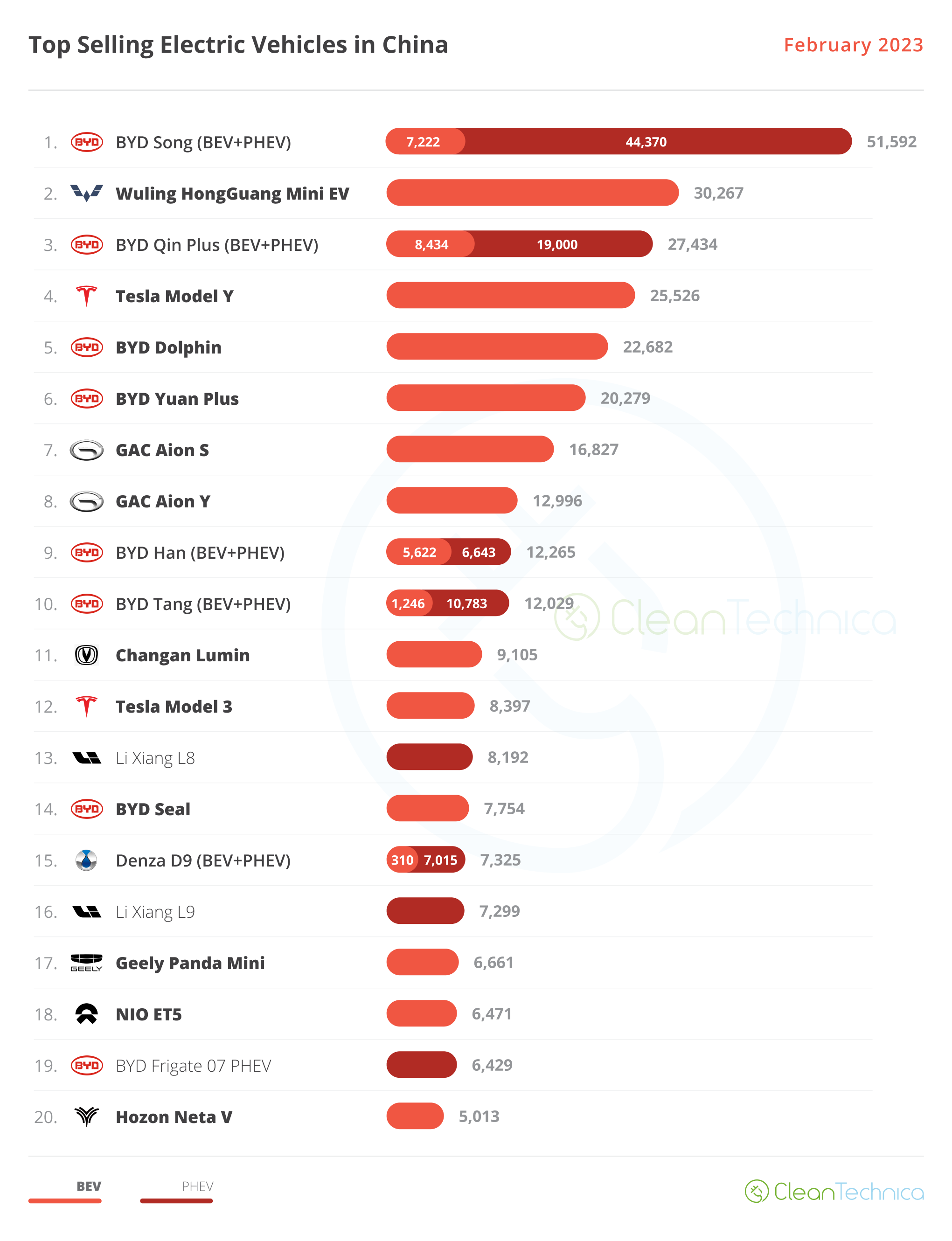

The 20 Best Selling Electric Vehicles in China — February 2023

Looking at February’s best sellers, we should first celebrate the fact that we had seven plugin models in the overall top 10, with only the #4 Nissan Sylphy, #7 VW Lavida, and #10 Haval H6 being pure ICE models*. (*The Haval H6 isn’t really a pure ICE model, because it has HEV and PHEV versions, but because most sales still come from the ICE versions, let’s consider it an ICE vehicle here.)

Here’s more info and commentary on February’s top selling electric models:

#1 — BYD Song (BEV+PHEV)

BYD’s midsize SUV is the new leader in the Chinese automotive market, now regularly topping the mainstream auto sales table. BYD’s current star player scored 51,592 registrations, 7,222 of them belonging to the BEV version. So, will the Song end the year as the best selling model in the Chinese automotive market? Well, it depends on the competition, especially the internal competition. Currently, the Song only has the recently introduced Frigate 07 PHEV as internal competition, but the upcoming Sea Lion (BYD’s take on the Tesla Model Y theme) and the premium car-on-stilts Denza N7 (a car that sits somewhere between the Tesla Model Y and the Zeekr 001) are both set to land this year. This is probably too much competition inside BYD’s midsize SUV portfolio (the Song as the lower priced model, the Frigate 07 & Sea Lion as mid-priced models, and finally the more upmarket Denza N7). It is probably too much competition for the Song to continue clocking 40,000–50,000 sales/month, a necessary threshold to continue leading the cutthroat Chinese auto market.

#2 — Wuling HongGuang Mini EV

With 30,267 registrations last month, the tiny four-seater won another silver medal in the overall market, but considering past performances, this is still kind of a meh score. It seems the new, direct competition, like the Geely Panda Mini (#17 in February, its first volume-delivery month, with 6,661 registrations) is making a dent in the little EV’s sales. Still, with this kind of scale, it is natural that the joint venture is turning a profit on its star EV (probably a small one, admittedly). The Wuling Mini EV has already made its mark in automotive history, becoming a trendsetter and a disruptive force in urban mobility. The added bonus is that the people buying it (mostly females under 35 years old) are usually a hard-to-capture audience.

#3 — BYD Qin Plus (BEV+PHEV)

Along with the Song, the BYD Qin has been a bread and butter model for the Chinese automaker for a long time. The midsizer reached 27,434 registrations in February, with the BEV version alone scoring 8,434 registrations. This placed it in 3rd in the overall market, allowing BYD to place two models on last month’s overall podium (Volkswagen, take notice). With the recent price drop and prices now starting at 100,000 CNY ($15,000), demand spiked again, despite the strong internal competition — the BYD Seal for the BEV version and the Destroyer 05 for the PHEV version. Expect BYD’s lower priced midsize sedan to continue posting strong results, at the cost of its most expensive siblings, keeping its most direct competitors, the Tesla Model 3 and GAC Aion S, at a safe distance.

#4 — Tesla Model Y

Tesla’s star model got 25,526 registrations, which allowed it to land in #5 in the overall ranking. It seems the US crossover has found its cruising speed in the Chinese market, at around 25,000–30,000 units. While that doesn’t allow it to be the best seller in the market, it allows it and the Model 3 to be the only two foreign EVs to run at the same pace as the domestic brands (Volkswagen, take notice). To place things into context, the other best selling foreign EVs, the ID.3/4 series from Volkswagen and the i3/iX3 midsizers from BMW, each maxed out at around 3,000 units in February.

#5 — BYD Dolphin

Temporarily at the bottom of the BYD lineup (the small Seagull is set to land soon), the small-to-compact Dolphin scored 22,682 registrations. One can say that the Dolphin has this class all to itself, as its most direct competitor in this category is the #20 Hozon Neta V, getting four times fewer sales (5,013). The reason for this success? Using a space-efficient interior and competitive specs (not unlike a certain Chevrolet Bolt), the Dolphin adds the cost-saving features of its brand new 3.0 dedicated platform and cost-leading batteries. That allows it to offer unbeatable prices, starting at 13,000€ for the 31 kWh battery version. Of course, do not expect these kinds of prices when the Dolphin lands on European shores (tariffs, VAT, etc.), but I wouldn’t be surprised if it started to be sold here at 19,999€ … which would still be a killer price considering the direct competition is still north of 30,000€ (Renault Zoe, Peugeot e-208, etc.). Once the Dolphin lands, expect some serious price slashing from legacy OEMs.

Looking at the rest of the best seller table, for once the highlight does not come from BYD or Tesla, but from GAC’s Aion S. The midsizer from the Guangzhou make had a record 16,827 registrations, an impressive performance in one of the slowest months of the year, allowing it to end the month in 7th. Does this mean the veteran sedan can keep pace with the Tesla Model 3 and BYD’s Qin Plus throughout the rest of the year? That would at least bring some extra color to the current BYD domination. To be continued….

The Aion Y, the other half of GAC’s dynamic duo, also shone brightly, ending February in #8 with 12,996 registrations. The Geely Panda Mini, the OEM’s answer to the Wuling Mini EV, joined the table for the first time. It was in #17, with 6,661 registrations right in its first volume month. Expect the tiny EV to become another strong player in the city EV arena, and while it might not reach the Wuling Mini EV’s sales levels, I believe Geely will already be happy if it gets to a cruising speed of 10,000 units/month.

Finally, we see BYD’s new Frigate 07 PHEV in #19 in only its 3rd month on the market. That means there were 8 BYDs in the top 20, or 9 if we count the #15 Denza D9 giant RV large MPV as part of BYD’s lineup (as an OEM).

Outside the top 20, there was no major news this time. Geely’s Zeekr 001 high-end model scored 4,760 registrations, a somewhat meh result that could be partly explained by the fact that buyers might be waiting for the production series of the big fastback model with CATL’s famous Qilin battery. That could allow the 001 to have a 140 kWh battery!

(And now a suggestion for Geely: Do an Aston Martin–like sports car called 007. Hey, it’s not that much of a stretch — just ask your stable-mates Lotus to do it! You’re welcome!)

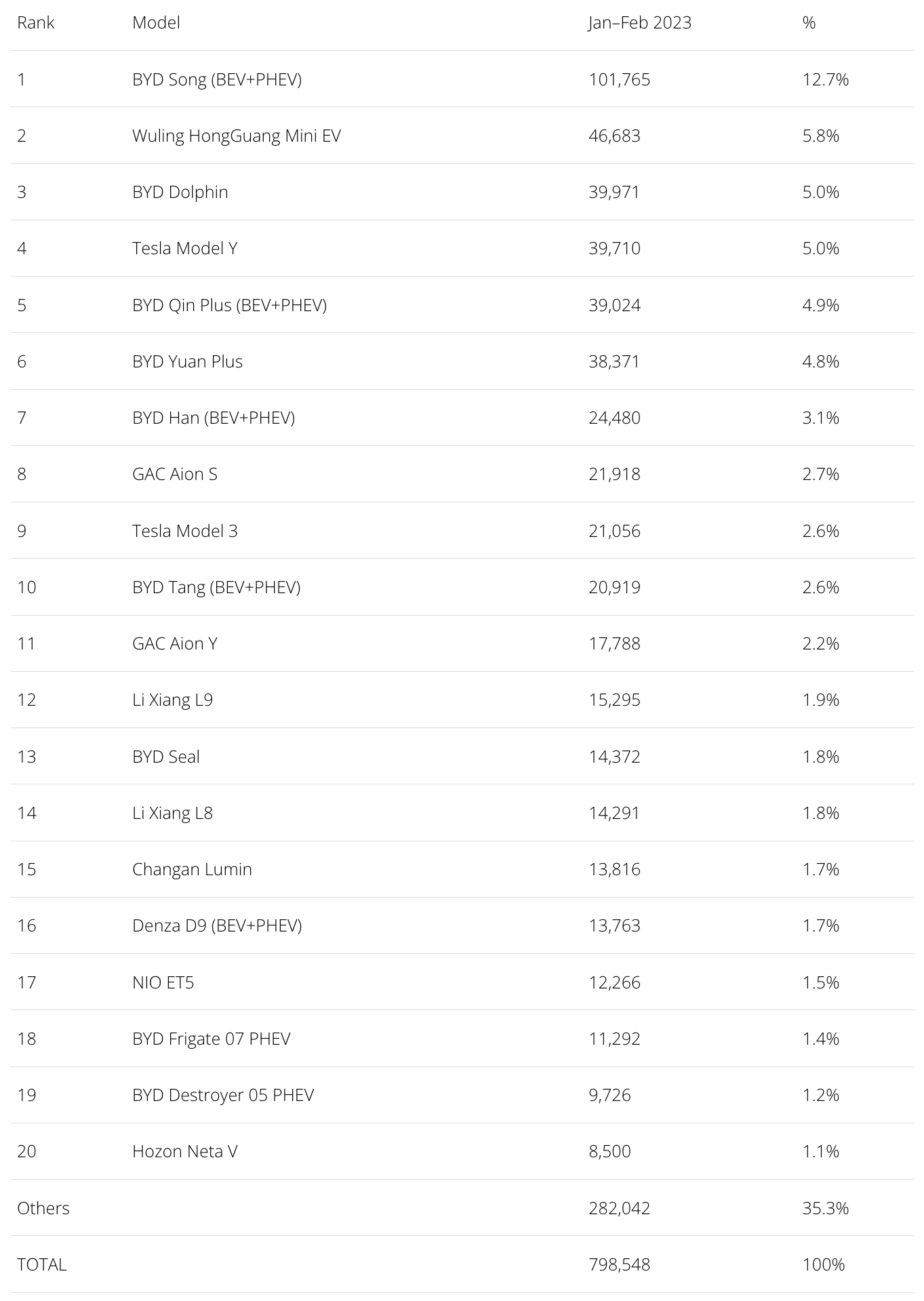

The 20 Best Selling Electric Vehicles in China — January–February 2023

Looking at the 2023 ranking, the leading BYD Song is well above the competition, doubling the result of the new runner-up Wuling Mini EV.

The BYD Dolphin completes the podium, with close to 40,000 registrations, ending slightly ahead of the #4 Tesla Model Y and #5 BYD Qin Plus. With the #6 BYD Yuan Plus also not that far behind (38,371 registrations), expect an entertaining race for the bronze medal in the coming stages, with Tesla hoping to have a strong March and hoping to end Q1 ahead of the competition.

Below them, the highlights are once again GAC’s dynamic duo. The Aion S jumped seven positions, to 8th, while the Aion Y also surged seven spots, in this case to #11.

Finally, in the last place on the table, and recovering from a slow start of the year, we now have Hozon’s Neta V. The small crossover is surely looking to recover more positions in the coming months.

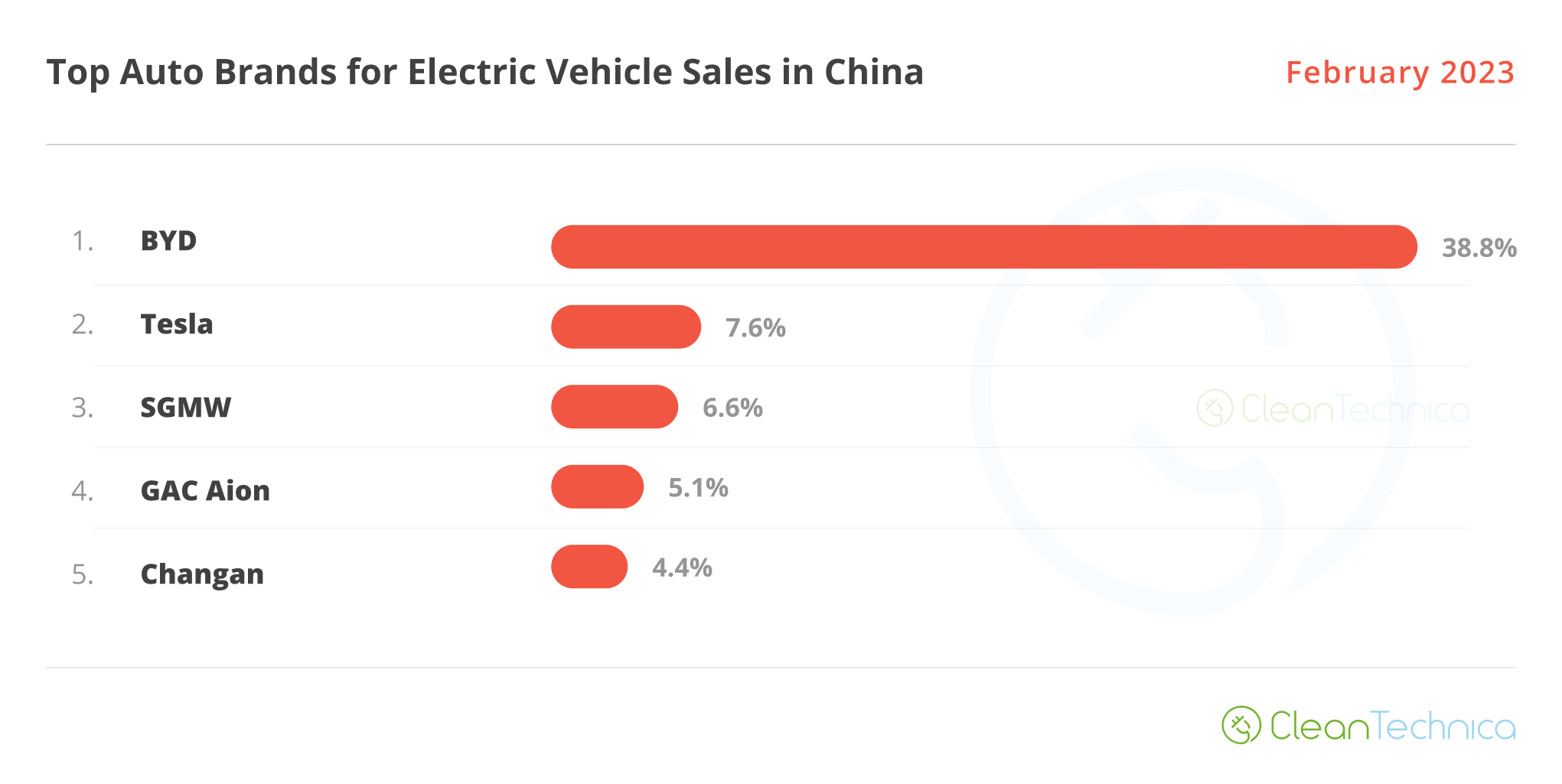

Auto Brands Selling the Most Electric Vehicles in China

Looking at the auto brand ranking, there’s no major news. BYD (38.8%, down from 40.2%) remains stable in its leadership position, and not only on the plugin table. In the mainstream market, it beat Volkswagen by 2,000 units in February (Volkswagen, take notice). The Shenzhen automaker is looking to win its 10th plugin automaker title this year, while Tesla (7.6%, down from 7.8%) is stable in second place.

The SGMW joint venture is in recovery mode (6.6%, up from 5.1%) and is looking to switch positions with #2 Tesla. Meanwhile, the GAC Aion (5.1%, up 1.8%) came out of nowhere and jumped into the 4th position.

Finally, Changan (4.4%) dropped to 5th, kicking Li Auto (4.1%) out of the top 5.

Auto Groups Selling the Most Electric Vehicles in China

Looking at OEMs/automotive groups/alliances, BYD is comfortably leading, with 40.5% share of the market. It is profiting from good results from both BYD and premium daughter Denza. SAIC (8.4%, up from 7.1%) returned to the runner-up spot, displacing Tesla to 3rd. That’s thanks to a good result from SGMW, which was more than enough to counterbalance another bad month from the SAIC mothership. What’s up with that, SAIC?

While Tesla is the new bronze medalist, GAC has jumped to 4th. The Chinese OEM profited from the brilliant performances of its dynamic duo to join the top 5. One step down, Geely–Volvo (4.9%) ended the month in 5th.

With #6 Changan (4.8%) not too far behind, Geely can’t rest on its laurels. The Chinese Volkswagen Group is still way better than the original, though, with Volkswagen Group slowly eroding into irrelevance in China (2.5%, down from 2.6%) — so much so that BMW Group is on its way to surpassing it and becoming the second best selling foreign OEM in China.

It will be interesting to look at Geely–Volvo’s and Volkswagen Group’s behavior this year. Prior to the EV revolution, Volkswagen Group was the #1 domestic and foreign automaker in China. Having seen its thrones being taken by BYD and Tesla, respectively, it’ll be interesting to see how the company reacts. With the mainstream and plugin markets quickly merging in China, how Volkswagen Group tackles the current disruption will say a lot about its future in the largest automotive market in the world.

The current situation is especially critical for Volkswagen Group, because the 15% market share it currently owns in the Chinese mainstream market is far above the 2.5% it has in the plugin market. If the latter is an indication of the future, it would mean that in China alone, Volkswagen Group will lose over two million sales per year! Considering that Volkswagen Group sold 8.3 million units in 2022, this might mean that the German conglomerate could lose 25% of all its global sales once the full electrification of the Chinese market is complete, about five years from now.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy