German EV Market — Hangover After Pull-Forward In December

Support CleanTechnica's work through a Substack subscription, on Patreon, or on Stripe. Help us produce all of the high-quality, original content we publish week after week despite the challenges of content-scraping AI, antisocial media, inflation, and other hurdles.

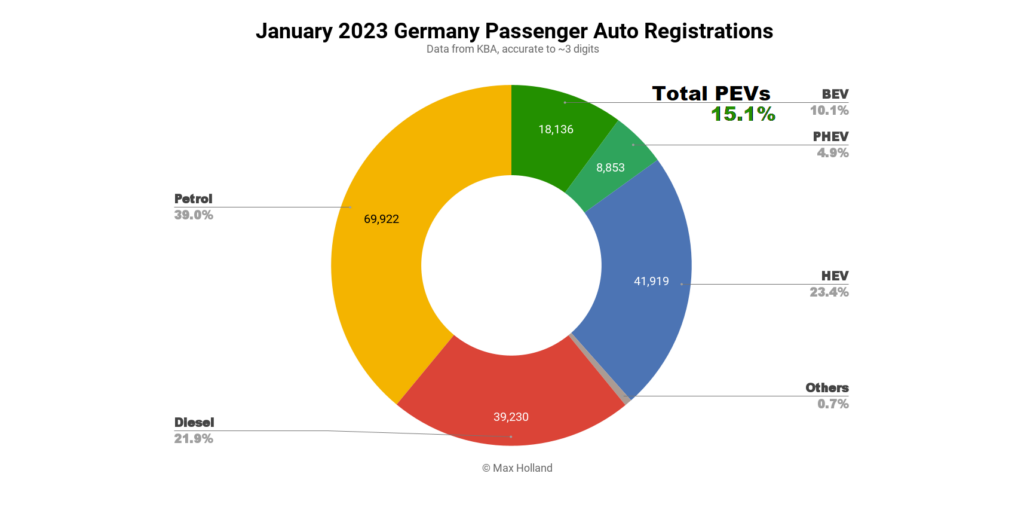

Germany saw plugin electric vehicle (EV) share at a low ebb in January, just 15.1%, from 21.6% year on year. The one-off low result comes in the shadow of record plugin share in December, ahead of reduced incentives from January 1st; the imbalance will normalise in the coming months. Overall auto volumes were 179,225 units, just 2% lower than January 2022, though still well down from pre-Covid seasonal norms. The best selling BEV was the Tesla Model Y.

January’s combined plugin share of 15.1% comprised full electrics (BEVs) at 10.1%, and plugin hybrids with 4.9%. Their respective shares in January 2022 were 21.6%, 11.3%, and 10.3%.

Trend Analysis

BEVs took a slight YoY dip in volume, from 20,892 units in January 2022, to 18,136 units this time around. This reflects the hangover from the December pull-forward, ahead of the roughly €1500 trimming of incentives from January 1st (see last month’s report for details). Since this is a modest change, and still leaves €3000 to €4500 BEV incentives on the table, the hangover is not overly dramatic for BEVs, and the market should equalise by sometime in Q2.

PHEVs on the other hand saw a more dramatic complete incentive cut. This means that a consumer buying a PHEV before the end of December was saving around €4000, compared to buying in January. The large cost change created a much stronger pull-forward-and-subsequent-hangover disjuncture.

As a result, the PHEV category in January saw their lowest market share since June 2020, and unit volumes just 12.7% of those seen in December. It will be several more months before we can begin to detect what the new steady-state market share of PHEVs is likely to be. There may remain some distorting PHEV incentives in, e.g., company tax rates, and similar (beyond simply the lower rated CO2 emissions). Please chime in below if you have insights into this.

Personally, I think the only “incentive” for PHEVs should be the intrinsic running cost savings that they provide when correctly used as a plugin, along with the convenience features of having a large battery (cabin pre-conditioning, etc), and the other experiential benefits of electric drive (smooth, silent, etc).

Because of these fiscal incentive disjunctures, we can’t read too much into the December-through-January pattern of plugin sales, other than saying that the overall the move to EV will continue. We will get more of a handle on 2023’s plugin trajectory perhaps by the end of Q2, and certainly later throughout the second half.

Best Selling BEVs

January saw an interesting distinction in market leader Tesla’s model deliveries:

The habitual first-month-of-quarter low volumes were still evident for those models produced overseas and arriving via global shipping, most noticeably, the Tesla Model 3, which again saw a relatively quiet month (389 units), compared to December and November.

With the local Tesla Gigafactory in Brandenburg now producing decent volumes of Model Y, however, its January performance was very strong, with 3,708 units. We haven’t seen the first month of a quarter with these volumes for a Tesla model previously, and this should become the new normal, from now on.

In second place was the Volkswagen ID.4/ID.5 pair, with the refreshed Audi e-tron (which from now on is badged as the Q8 e-tron), taking third.

The Tesla Model Y’s January volumes were in fact so strong that it actually took 4th spot in the overall auto market for the month (behind the VW Golf, VW Tiguan, and VW T-Roc), something never previously seen in the first month of a fiscal quarter.

Over a 3 month period, the Golf, and Tiguan, are nevertheless each selling around 20,000 units (sometimes a bit more), whereas the Model Y is still “just” around 15,000 units for now. With production still ramping at the Brandenburg factory, Tesla could close this gap.

Further down the top 20 list there were a few movements in the ranks, but considering the market disjuncture discussed above, we can’t read too much into these.

There were four BEV models new to the German market in January; the BYD Atto 3 (48 initial units), Genesis GV60 (27 units), Hyundai Ioniq 6 (8), and even the Lucid Air (2). Diversity of choice is obviously healthy for the continued improvement of EVs, so it’s good to see these new arrivals. It will be interesting to see if the GV60 and Air are given attention by German premium-segment consumers, who have transitionally favoured their home-grown premium brands.

Let’s now turn to the three month picture:

Tesla’s models have a very strong lead, on the basis of massive volumes since November. Volkswagen’s ID models will need to step up to catch up. This is not just in Germany — the balance is roughly similar at the Europe-wide level.

Most of the top 10 rankings have shown remarkably little movement (one or two positions at most) since three months ago. Gainers include the Opel Corsa (10th from 18th), and Renault Megane (12th from 17th).

Those falling in rank, since 3 months prior, include the Hyundai Ioniq 5 (7th to 13th), Audi Q4 e-tron (10th to 14th, Skoda Enyaq (12th to 18th), and Mini Cooper (13th to 19th).

Many of the larger movements are due to irregular global logistics patterns (particularly Tesla, Hyundai, MG), and temporary regional allocation decisions. As a reminder, the best BEVs (i.e. most or all of the top 20) are production-and-supply constrained, rather than demand constrained.

Let’s take a quick look at the manufacturing group performance:

The top four ranks are unchanged since the three months to October. Volkswagen Group has actually taken 2.2% more of the German BEV market pie since the prior period. Tesla lost 1.5%, Stellantis gained 2.2%, and Renault–Nissan gained 1.1%.

The top four ranks are unchanged since the three months to October. Volkswagen Group has actually taken 2.2% more of the German BEV market pie since the prior period. Tesla lost 1.5%, Stellantis gained 2.2%, and Renault–Nissan gained 1.1%.

In the lower half, BMW Group slipped from 6th to 7th (just outside this table), and Mercedes Group climbed from 7th to 5th, pushing Hyundai Group down a spot to 6th.

Outlook

January’s low plugin result is a one-off, the hangover from the significant pull forward we saw in December (and to some extent, November). In a few more months, the market will settle in to a new normal.

More broadly, the German economy continues to face significant headwinds, which will necessarily affect the auto market this year. The government statistics office just reported a 0.2% QoQ shrinkage in the final quarter of 2022, which was worse than expected.

Q1 2023 is also expected to show shrinkage, which means that 2023 will likely start in recessionary conditions. As of early February, the Scope ratings agency expected a 0.2% economic decline across 2023, whereas in late January, the government was still hoping for 0.2% growth. This latter was before the news of the 2022 Q4 shrinkage however. Deloitte forecasts 0.4% shrinkage, amid declining consumer spending.

Obviously heavy energy users, like the auto manufacturers and their supply chains, will face cost pressure from energy price inflation. This comes just as consumers are facing both recessionary conditions and inflation (still near 10% overall).

These macro economic conditions suggest growth in overall auto sales is unlikely in 2023, even if the auto supply chain shortages seen over 2021 to 2022 are somehow improved.

As I usually point out, since demand for plugins will likely remain relatively buoyant in the context of a shrinking overall auto market, this does at least mean that plugin share of the market will continue to grow. We will have to see how all these factors play out.

What are your thoughts about Germany’s auto market outlook for 2023, and the EV transition? Please jump in and share your perspective, in the comments below.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy