Egypt Has Opportunity To Gain Green Infrastructure While Hydrogen Hype Persists

Support CleanTechnica's work through a Substack subscription, on Patreon, or on Stripe. Help us produce all of the high-quality, original content we publish week after week despite the challenges of content-scraping AI, antisocial media, inflation, and other hurdles.

Egypt’s Aswan Dam, as large as it is, has been providing a declining percentage of the country’s electricity with each passing decade, while natural gas has been providing more and more. While its oil rent is less than that of nearby Algeria’s, it is economically exposed to the loss of fossil fuel revenues, and susceptible to dreams of replacing them with green hydrogen and derivatives.

As part of my recently published report for Corporate Europe Observatory (CEO) and The Transnational Institute (TNI) on hydrogen in Northern Africa and the European organizations and firms supporting manufacturing it for export to Europe, I looked at Egypt’s plans more closely. I make no claims to be an export on the country or its history, or to have significant depth on other challenges it faces, of course. It’s a million square kilometer country with a 100 million citizens in a huge continent with its own rich past and priorities, and with intelligent and informed leaders and influencers who will make their own decisions.

As with Morocco and Algeria, Egypt has excellent wind and solar resources, but also has the Aswan Dam, although that supplies a surprisingly small percentage of its electricity today.

Egypt is not in as challenging an economic place as Algeria, but direct oil and gas revenue still represents 4% of its GDP, and the country has been growing exports of natural gas, including liquid natural gas.

What Are Egypt’s Hydrogen Plans?

Egypt’s hydrogen plans are not as advanced as those of Morocco or Algeria. Third-parties such as the Oxford Institute of Energy Studies — yes, the name hints at a problem when it comes to hydrogen — published an assessment of Egypt’s low-carbon hydrogen prospects in 2021. The authors, both from northern Africa, have extensive histories in oil and gas, and the report’s focus shines through. But it, like the report you are reading now, is a third-party perspective on Egypt, not an Egyptian governmental or corporate initiative. For that, we have to look at Egypt’s efforts with Europe.

Europe’s Development Bank Is Pushing Hydrogen For Energy

Egypt’s Ministry of Electricity and Renewable Energy and Ministry of Petroleum and Mineral Resources recently reached an agreement with the European Bank for Reconstruction and Development (EBRD) to develop a hydrogen strategy expected in the middle of the year. Unfortunately, the EBRD is part of the current EU focus on hydrogen for energy, not as a chemical feedstock, and so it is likely that Egypt will not be best served by their assistance. The involvement of the Egyptian oil and gas ministry is also telling.

EBRD’s hydrogen coordinator is on record as saying electricity doesn’t work for high heat applications, when common electric steel minimills using electric arc furnaces reach 1,500° to 3,000° Celsius and aluminum smelting is done with electricity as well at very high heat. It is reasonable to say that you can’t refuel most existing industrial infrastructure built for high-quality heat from natural gas with electricity, but as industrial facilities are scrapped and replaced, using electricity as a source of high-quality heat is almost always viable. There are very few industrial processes where there is no alternative to fuel, and the EBRD’s stance is contrary to climate and economic sense.

It’s illustrative to look at the EBRD’s hydrogen work with Ukraine, a key reason for the expanded focus on northern Africa. Their work in that currently beleaguered country was with the Gas Transmission System Operator of Ukraine (GTSOU), and focused on hydrogen as an energy carrier. They clearly state that their focus in EBRD regions is on making hydrogen competitive with fossil fuels.

As was stated in the report, hydrogen is not used as an energy carrier today and electricity is vastly more fit for purpose, more efficient and much cheaper. The EBRD would be better served by focusing on displacing chemical feedstocks using gray and black hydrogen, and helping countries retire legacy industrial infrastructure using natural gas or coal, and developing electrically powered industrial processes. Their current path is unfriendly to the climate and the economies they are purporting to assist.

Tax Breaks For Green Hydrogen & Ammonia

In advance of the EBRD strategy, Egypt’s government has passed legislation that would provide a wide range of fiscal support for green hydrogen and ammonia projects under the Investment Law No. 72 of 2017. Article 20 of the Investment Law enables projects deemed strategic by the Cabinet to be granted a license to operate and land in a single, rapid process. Article 11 provides tax breaks from 30% to 50%. Other provisions include state-funded grid connections and other benefits.

Clearly the national government of Egypt is taking hydrogen very seriously, and considers it a key economic development pathway. Hydrogen is key to decarbonization and the economy, it’s true, but there are uses which are better and worse.

Green Ammonia & Hydrogen For Shipping

Two projects have been announced with European firms for manufacturing shipping fuels. The IPCC’s most recent report on climate solutions and I agree on shipping refueling, which is that inland and short-sea shipping will electrify, but that deep-sea long-haul shipping requires alternative fuels, and that segment is still large.

At present, multiple technologies are being evaluated as replacements for bunker fuel, which is one of the waste by-products of refining crude oil, similar to asphalt. Maersk is investing in early efforts around green methanol, although they are underwhelming at this point. Hydrogen is being touted by many, despite its serious disadvantages of cost, boil-off, and high volume requirements.

Methanol is a globally produced alcohol, with a market dominated by Vancouver, BC, Canada’s Methanex, which operates plants around the world. It’s toxic, and can cause significant health problems if ingested, if it gets on skin, if it is vaporized and inhaled, or if it gets in a person’s eyes. As a fuel, its energy density is substantially below that of diesel or bunker fuel, so much more of it is required to travel the same distance. And green methanol will be much more expensive than shipping fuel today, of course.

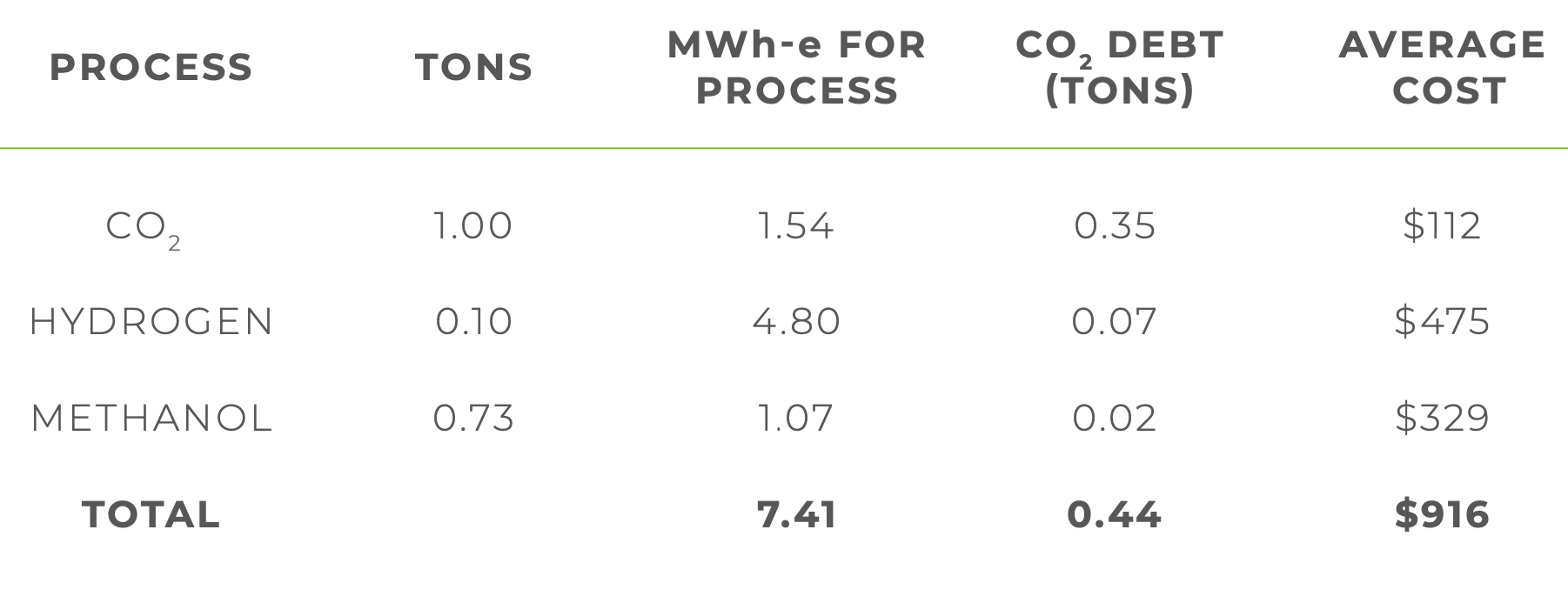

This example is from a direct air capture solution, so the cost of CO2 may be somewhat lower, but the hydrogen costs from a large-scale study of the alternatives are in line with assessments in this report of Lazard LCOE costs given utilization and electricity cost constraints. The cost of manufacturing methanol ends in the $1,250 per ton range, and methanol’s energy density is about half of diesel, so the cost of equivalent fuel is closer to $2,500 for the same range.

Others are considering green ammonia as a fuel, something which has more challenges than green methanol. Ammonia will kill a person who breathes it in concentrations as low as 0.5% of the atmosphere. If it comes in contact with water, it reacts quickly and turns into ammonium hydroxide, a caustic substance which can seriously damage lungs and mucous membranes, before dissociating into ammonium and hydroxide which are less harmful but still not safe for humans. Shipping is by definition exposed to water. Ammonia spills on a ship could be life and health threatening in three different ways.

Ammonia takes three times the energy to ignite as diesel, which makes dual-fuel engines problematic. Burning anything in oxygen creates nitrous oxides, including the variant with 265 times the global warming potential of CO2, something that can be somewhat reduced through careful ignition and temperature control in the engine. And, of course, green ammonia is made with green hydrogen, and will be much more expensive than current gray ammonia, and more than bunker fuel, even with the current price spikes of oil caused by the Russian invasion of Ukraine. The first dual-fuel ammonia marine engine is expected to be available for tests only in 2024, so ammonia is not a slam dunk as a marine fuel.

This is not to say that green methanol and ammonia won’t be the shipping fuels of the future for the portions that can’t be electrified, just that it’s far from a certainty. As with aviation, biofuels present another competitor, and it’s quite possible that they will dominate the sector. Egypt’s official statements indicate that they are going to manufacture both.

Egypt already has a shipping fuel initiative involving green hydrogen with Maersk, the Danish shipping company. They have reached a joint agreement with several Egyptian ministries and agencies for the development of a green hydrogen facility for marine fuel in the Ain Sokhna’s economic zone near the Suez Canal. Given Maersk’s focus on methanol, it’s likely that they will be manufacturing that fuel.

Green & Blue Hydrogen & Ammonia For Europe & Asia

But ammonia isn’t just being considered for shipping, it’s being considered for export as well, especially to Asia. This part of the potential for green energy exports from high-renewables areas to lower renewables areas has some merit, likely more merit than green ammonia as a fuel. As stated earlier in the report, ammonia is a key chemical feedstock for the manufacturing of fertilizers, and is used directly as a fertilizer itself. As is the case for all three of the countries, Egypt was a net exporter of fertilizer until 1993, and could return to that export stream.

Ammonia-based fertilizer is a climate change problem coming and going. The use of gray hydrogen means that there are three times the mass of CO2 and another three times the equivalent mass of CO2e in manufacturing the ammonia. But when ammonia and ammonia-based fertilizers are spread on farmland, up to the equivalent of another six tons of CO2e in the form of nitrous oxides with a global warming potential of 265 times that of CO2 are released.

Ammonia fertilizer manufacturing accounts for 37% of pure hydrogen demand globally, and the triple innovations of low-tillage agriculture, precision agriculture and agrigenetics of nitrogen-fixing microbes and plants are going to bring demand down substantially over the next 80 years as part of fixing agriculture’s emissions. The growth of ammonia-based fertilizers since the 1970s has been much slower than the growth of the population as more efficient use of it has occurred. And when the price of fertilizer increases, more efficiencies will be found.

Finally, a major hindrance on shipping volumes will be increased fuel costs due to ensuring the significant negative externalities are added to their cost or as more expensive replacements used. While some shipping is essential, I project that hydrogen and ammonia will be increasingly manufactured domestically in countries from decarbonized grid electricity, as green hydrogen’s raw materials of water and CO2 are in abundance in most places, even if desalination is required in some.

That said, there are at least three ammonia export initiatives in place in Egypt.

First is a northern European firm, Statec, a Norwegian renewables company that’s 15.2% owned by Norway’s national oil and gas firm, Equinor. A $5 billion deal has been signed for a green ammonia plant to be built in the Ain Sokhna economic zone near the Suez Canal. The intent for the initial million tons annually and the eventual three million tons is export to Asia and Europe, where at least at present ammonia demand is increasing.

The second is exploration with Toyota Tshusho of Japan, Egyptian Petrochemical Holding, and Egas of blue hydrogen for manufacturing ammonia for export to the Asian country. Blue hydrogen is not a climate solution. The upstream methane emissions remain regardless of capturing CO2 at the point of hydrogen manufacturing, and capturing the CO2 at point of manufacturing is likely 85%. Finally, most CCS is used for enhanced oil recovery, and as Egypt is an oil and gas country, the likelihood of it using CO2 for that purpose with two to three times the mass of CO2 emitted when the oil is burned as was sequestered is very high. Emissions from blue ammonia will still be high, and a substantial portion of them will be inside Egypt’s border, and so on their emissions scorecard and impactful on inevitable carbon border adjustments such as Europe’s 2021 announcement.

Siemens has reached an agreement with the Egyptian Electricity Holding Company to develop a 200 MW green hydrogen facility for export. Transporting hydrogen as hydrogen is very expensive for the units of energy delivered, and so is deeply unlikely to ever find a real market.

Finally, the Italian firm Eni, prominent in Algerian hydrogen efforts, is also engaged with the Egyptian Natural Gas Holding Company for the manufacturing of blue hydrogen, with similar concerns about emissions and price.

What Could Egypt Do Instead Of Exporting Inefficient Chemicals?

CO2 emissions in Egypt have increased by 190% since 1990, the opposite direction from good climate action.

Green Electricity

Emissions from electrical generation in Egypt are high, and have increased substantially over that period. In 1990, the Aswan Dam was in operation and represented a large portion of the country’s electrical generation. Now it’s a tiny fraction with natural gas generation and worse, oil generation, accounting for the vast majority.

Building wind, solar, transmission, and storage sufficient to eliminate first oil and then gas generation would reasonably be higher on Egypt’s priority list than significantly reducing the energy and value of generated electricity by turning it, inefficiently, into liquid and gaseous fuels which are too expensive to have markets. Egypt’s current electricity demand is twice Algeria’s, about 160 TWh per year, but its renewables targets are also more ambitious, aiming to reach 42% by 2035. This would require investment in the ballpark of $24 billion to deliver roughly 19 GW of solar, 10 GW of wind energy, transmission, and storage capacity over 13 years. While Egypt’s oil and gas windfall of 2021 and 2022 haven’t been as large as Algeria’s, its economy is 2.5 times bigger, so just under $2 billion per year until 2035 is not an unmanageable figure.

Similarly, connecting electricity transmission via Cyprus into Turkey and hence to Europe to share renewable electricity across a broader geographical region, including selling Egyptian solar and hydro electricity into Europe at peak times, is a stronger idea than attempting to create an export market for too-expensive chemicals that will be manufactured domestically in most countries. Similarly, more connections through northern Africa to share electricity and storage would be beneficial economically and from a climate perspective.

Greening Local Fertilizer

Egypt is doing better at manufacturing the fertilizer it uses domestically than either Morocco or Algeria, with 40% of its demand supplied internally. However, that manufacturing is all from gray hydrogen with its 8-10 times the mass of hydrogen CO2 debt, and about the same CO2e debt in upstream methane emissions. Egypt’s annual consumption of fertilizer in the rich Nile Valley and delta was in the range of 1.7 million tons in 2018. Given the CO2 and CO2e emissions before use of fertilizer, that represents in the range of 10-12 million tons of CO2e annually, a significant portion of Egypt’s emissions. Egypt would more reasonably green its local fertilizer manufacturing and extend it to the major of domestic demand, as demand in turn declines due to better agricultural practices that are not nearly as fertilizer intensive.

If Europe’s development bank is interested in assisting northern Africa, these should be the focus areas. With luck and intelligent strategy, Egypt’s leaders should be able to gain significant green infrastructure investment of value to the country and its citizens, and avoid being trapped into decarbonizing Europe while remaining high carbon themselves.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy