Breakthrough Energy Ventures Has Bad Investment Theses Therefore Bad Investments

Support CleanTechnica's work through a Substack subscription or on Stripe.

Eight years ago, Bill Gates and group of his closest billionaire acquaintances launched an incredibly well funded venture capital group. Its noble mission was funding and supporting transformative technologies aimed at mitigating climate change. Many of its investments are sound and if commercialized, would assist, at least a bit.

However, a large percentage of its investments are quite far off the mark. That’s mostly because of the biases of the founding billionaires and resulting investment theses that don’t stand up to scrutiny. Investment funds regularly ask me for my input and assistance with their investment theses, so I at least have the basis for an opinion in the matter.

Recently I stepped through their entire existing portfolio and added a couple of additional firms which are legacy BEV investments or Gates-specific investments. I graded each of them with a thumbs up, thumbs down or sideways.

Note that the dollar values are not all BEV investments, but the sum total of money I was able to identify through publicly available sources including VC money, seed rounds, other investors and grants. One of the things that BEV endorsement does is open up a lot of other pocket books. Published assertions are that they have spent $3.5 billion, which in turn unlocked in the range of another $18 billion.

Thumbs up meant that the portfolio firms were technically viable, would move the needle, had a business model that made sense, could scale and were worth venture capital funding to get them through the technology readiness levels to commercialization, if possible. Thumbs down almost entirely meant that they were solution space dead ends and a waste of funding, indicative of the biases and misconceptions of the BEV founders and the team that they assembled as a result. Sideways meant that they were head scratchers in one way or another, either not remotely climate solutions, having a clearly bad business model and hence being unlikely to scale, or simply not even something a venture capital firm would typically invest in and a portfolio outlier, hence something that they would likely not be that helpful with.

38% of their portfolio by value and investments make little sense to me, but I’m pleased to see that a slight majority of the investments are in good companies, aligned with real problems and doing useful work.

To call out some of the firms I’m fully supportive of:

- Boston Metals is doing excellent work on molten oxide electrolysis of iron as an alternative green steel technique. Electra is toiling in the same space.

- Kobold Metals is applying big data and AI to better enable critical mineral exploration.

- Pivot Bio is working to decarbonize agriculture by creating mass-brewable microbes that fix nitrogen around the roots of plants.

- FleetZero is delivering battery power systems for ships and rail.

- Heart Aerospace is building hybrid-electric passenger aircraft to decarbonize regional air.

- Kodama is using IOT, satellite data and AI to manage forests and forestry like precision agriculture.

- QuantumScape is working on solid state batteries for electric vehicles.

- Rondo is working closely on industrial heat storage.

This is far from an exhaustive list of the roughly 51 firms I think merit climate-centric VC capital funding. I’ve dealt with principals and founders of a couple of those firms and am deeply impressed by them and their clear-eyed vision on the business that they are working to innovate within.

Also to be scrupulously fair to BEV, their hydrogen investments aren’t as bad as many. Electric Hydrogen, H2Pro and Koloma are risky investments, but have the potential to deliver value for industrial hydrogen feedstocks should they pan out. Only one of their investments is explicitly in the dead end hydrogen for energy space, which is pretty good for a portfolio of over 100 firms given the absurd hype the molecule has received in the last several years. That one is in the space of aviation, where very little techno-economic due diligence makes it clear it has no play. Three out of six hydrogen plays is better than most track records in the past five years. Once again, this isn’t saying that the three good firms will end up lucrative or delivering climate value, just that there is potential that is aligned with a venture capitalist investment.

But then there are some big hitters, and they speak to the biases and blinders of BEVs founders.

One of the big ones is fission energy and its Dopplering into the future fusion sibling. A review of all of the billionaires behind BEV found pro-nuclear, renewables-dismissive stances. This was in 2015 when it was clear that renewables had the conditions for success, that nuclear did not have the conditions for significant scaling and that hammering deployment for renewables was the clear path to rapid decarbonization.

As I noted in an article on climate-aware billionaires’ biases late last year, most of them arrived at their opinions in the late 1990s or early 2000s, when it was quite reasonable to look across the space and see nuclear as the only generation technology that would enable us to move off of fossil fuels. The USA and France had managed to build respectable fleets in reasonable periods of time, and if you squinted a little, at what appeared to be reasonable price points. At the time, wind and solar hadn’t plummeted in price, proven almost risk free to construct and proven to have no impact on the reliability of grid electricity. Asserting that nuclear was going to be a big part of our energy future in 2000 or 2005 was a very reasonable, informed and logical position to have. Now, not really. 2015? Still not really.

If the billionaires had been closely tied to reality, they would have asked about the conditions that led to successful nuclear generation scaling, and worked out a strategy to recreate them. Instead, they made a bad diagnosis of the problem being one of technology and set out to correct the technology.

As I’ve noted, nuclear programs worked historically because there was an external, nuclear armed, expansionist threat that led to many countries seeing nuclear weapons of their own being required. This strongly supported commercial nuclear generation development to share expenses, supply chains, technology and expertise. A national strategic program was funded and created with strong political support from multiple parties and interest groups that would persist for decades. A national human resource program was created to train, certify and security credential the resources. Reactors were GW-scale to get the benefits of scaling up — scaling vertically, not horizontally in Silicon Valley speak — after early attempts to use small reactors almost identical to the ones on subs and aircraft carriers proved exceptionally expensive. Only one or two designs of typically a single technology were built, to enable lessons learned to be shared across deployments. Dozens of reactors were built relatively quickly to enable sharing to lessons learned and to keep master builders working before retirement.

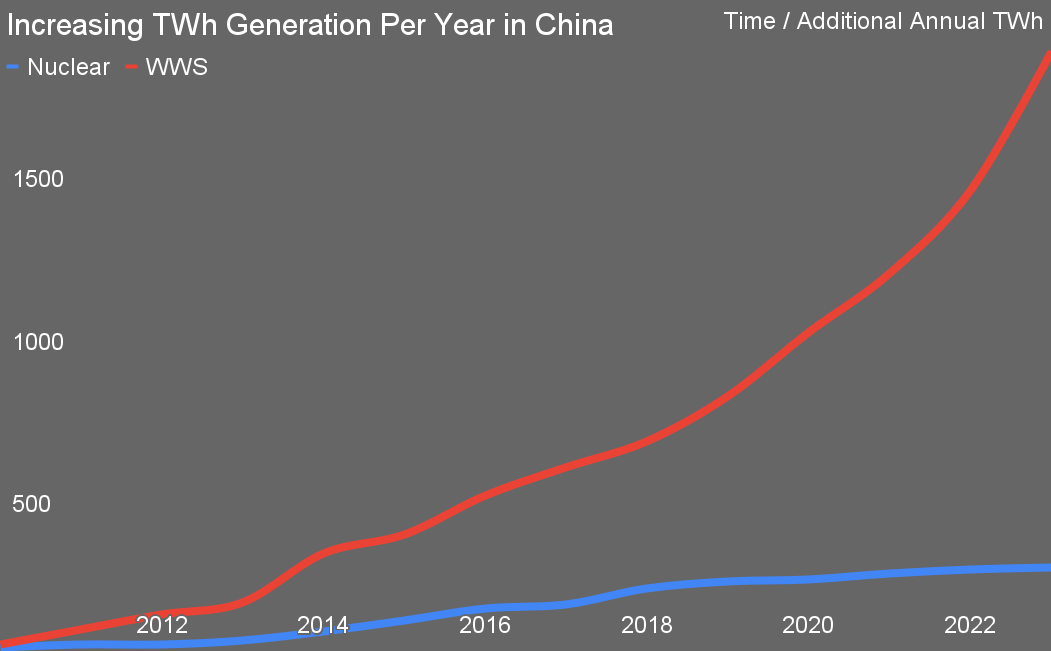

I started tracking the national experiment of nuclear and renewables in China in 2014, a year before BEV was founded. My thesis at the time was that renewables would radically outstrip nuclear, and this early 2024 update shows that’s true. Even China, which does megaprojects the way that other countries do press conferences, wasn’t able to create the conditions for success for nuclear scaling in the 21st Century. Most of the reasons that western nuclear advocates give for western headwinds for nuclear don’t apply in China, making it particularly apt as a comparison.

Small modular reactors don’t solve any of the conditions for success and in fact break two of them. First, they are tiny by comparison, so they lose the advantages of scaling up in size. Second, there are — the last time I counted — 18 different designs of multiple technologies jostling to compete on the market. Competing on a market isn’t what nuclear is good at, it has to be a national strategy aligned with foreign policy to succeed.

If I saw a nation or group of nations intentionally creating the conditions for success for scaling nuclear and following through, I would support that. However, I don’t see any nations, even the ones in the COP nuclear pledge, even acknowledging the real conditions for success or the barriers to scaling nuclear and strategically working to mitigate barriers and create success conditions. The headwinds for renewables are non-existent by comparison.

A problem with billionaires is that they accrete filters and bias-confirmers the way that subsea structures grow barnacles. They live in carefully curated virtual realities that are almost, but not quite, like actual reality. Bill Gates, for example, loves Vaclav Smil’s work, and as I noted Smil made three fundamental errors regarding energy and renewables that invalidated his analysis and thesis. It was only in 2021 that Smil acknowledged the primary energy fallacy, but he didn’t say he’d ignored it, that it was a mistake or that it deeply undercut his thesis, he just published a little monograph on it. Gates has been consuming Smil’s work as close to gospel and recommending it to others for a long time, and Smil was wrong about energy. Smil’s work agreed with Gates’ biases so his filters — mostly other people — ensured it landed on his desk, while publications by innumerable people about the primary energy fallacy and its implications for energy didn’t.

As a result, BEV has invested in three fusion startups whose only natural market, should they ever manage to deliver any power, is in spaceships beyond the orbit of Jupiter sometime in the next two hundred years. It’s noble and useful to do close to pure research into the space, but it’s a waste of money for a venture capital firm that has a focus on climate change. Gates, of course, is Chairman of Terrapower, a small modular reactor startup he founded 18 years ago, one he’s fronted to Congress, asking for billions in new subsidies for nuclear. The joint investments I’ve been able to track down are $3.3 billion to date.

Then there’s carbon capture and sequestration, the shell game of the fossil fuel industry. BEV has invested in seven CCS firms, only one of which, Verdox, was a worthwhile investment as it might prove useful in the couple of industrial spaces where CCS will actually be competitive with alternatives. I just published slides and notes from my PhD and masters student seminar on CCUS at SFU, so for chapter and verse on the space, the scale of the problem and the materiality requirements, have a look there.

BEV portfolio CCS firms have accrued $1.4 billion of investment and the only firm worth investing in only received $100 million to date. Most of the $1.4 billion was the ‘successful’ exit of Carbon Engineering when it was bought outright by its only customer, oil and gas major Oxy. As I noted in my analysis of the firm in 2019, its only natural market was enhanced oil recovery on tapped out oil wells with unmarketable natural gas. That’s what Oxy hired them to build and that’s what Oxy bought them to do. Enhanced oil recovery is not a climate solution. Burning enormous amounts of natural gas to capture CO2 from the air with two kilometer long, 20 meter high walls of fans, producing a ton of CO2 for every two tons of CO2 captured, and then shoving all three tons underground to get tons of oil to burn is a farce.

Four of seven BEV investments were in direct air capture, one of them the silliest Rube Goldberg contraption that it’s possible to imagine in the space.

And then there’s renewables, an actual solution space where actually deploying existing technologies with incremental innovation was clearly the winning strategy in 2015. Would you know that from BEV’s portfolio? Two of the six investments are for dead end technologies in solar and wind energy, the first something that’s languished in labs for decades for very well understood reasons, the latter a recreation of a multiply-failed approach with clear mechanical engineering and power generation deficiencies. Two are for reasonable business that have nothing to do with venture capital imperatives, so BEV likely isn’t helping them that much. Only two of the geothermal plays, Fervo and Natel, are really aligned investments, being high-risk, high-reward, should they pan out.

This part of the portfolio stinks of lack of awareness that wind and solar are incredibly fit for purpose, dominant and that investments in them have nothing to do with venture capitalism, except in narrowly identified value extensions. It’s back to the biases of the founders about wind and solar not being fit for purpose, so something else requiring invention and shepherding to market. That was impossible for any objective observer to conclude in 2015 when BEV is founded and now it’s just embarrassing. The awful wind generation technology received its funding in 2024. That’s more than embarrassing.

It’s worth pointing out the billion dollars sunk into fake food. That was clearly a hype bubble of a massive nature.

Veggie burgers and hot dogs have existed for decades. Asian cultures have an absurd history of fake meat. American startups thinking that they were boldly going where no food products firm had gone before were pandering to sheltered Silicon Valley types.

Fake food isn’t going to move the needle on climate action and it’s not going to make BEV any money to speak of either.

Next is storage, starting with heat storage. Chemical process engineer Paul Martin and I spoke about the strong value of heat storage at length recently, I’ve published on it extensively and as noted earlier, Rondo is well aligned in the space. But that’s storing heat for the sake of heat, arbitraging waste heat and cheap electricity for use as process heat later. That’s not storing electricity to return as electricity. The laws of thermodynamics aren’t going to be innovated around, and when there are 80% round trip efficient electricity storage technologies like cheap batteries and pumped hydro, heat based storage is never going to pencil out.

It’s going to be economically integral for industrial and district heating systems in many cases, but that’s not the target for three of five firms in BEVs portfolio. One of the firms is sideways in the space, not leaning into the actual business value proposition. Only Rondo is a good investment as a result.

BEV also invested in a firm which is proposing to refrack the same underground volume over and over and over for electricity storage, with very obvious and predictable failures looming. It took about an hour for me to work through the basics with that firm and arrive at the problem space from scratch, and any fracking engineer would glance at it and back away quietly. The firm is doing what fracking engineers work very hard not to do because it’s so problematic. Another storage firm is a clear investment in the high-profile team, because they’ve already pivoted on battery chemistries three times, their current chemistry has terrible round-trip efficiency, no off switch and a hydrogen problem, and is apparently trying to pivot out of energy storage entirely.

There are some good investments in the storage mix, but they are outnumbered by the ones that make no sense whatsoever, showing a lack of understanding of the storage market, a lack of understanding of industry, a lack of understanding of thermodynamics and a lack of understanding of basic geology. The complete failure of due diligence on the part of the BEV assessment teams is frankly shocking given how well funded the organization is. Or would be shocking if the founders’ biases weren’t being pandered to.

If BEV weren’t moving money and turning policy makers’ heads, I likely wouldn’t care. But billionaire adulation isn’t going to solve the climate crisis. Gates and the other founders are creating as many problems and causing secondary organizations and even governments to waste time and money we can ill afford. That’s not because they don’t care, but because they aren’t starting from reality. Investment theses require a very strong basis in reality and climate investments require strong technical due diligence. BEV’s theses in several parts of their portfolio are off base, and their technical due diligence approaches non-existent.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy