How The IRA Is Affecting Energy Storage Projects In The USA

Support CleanTechnica's work through a Substack subscription or on Stripe.

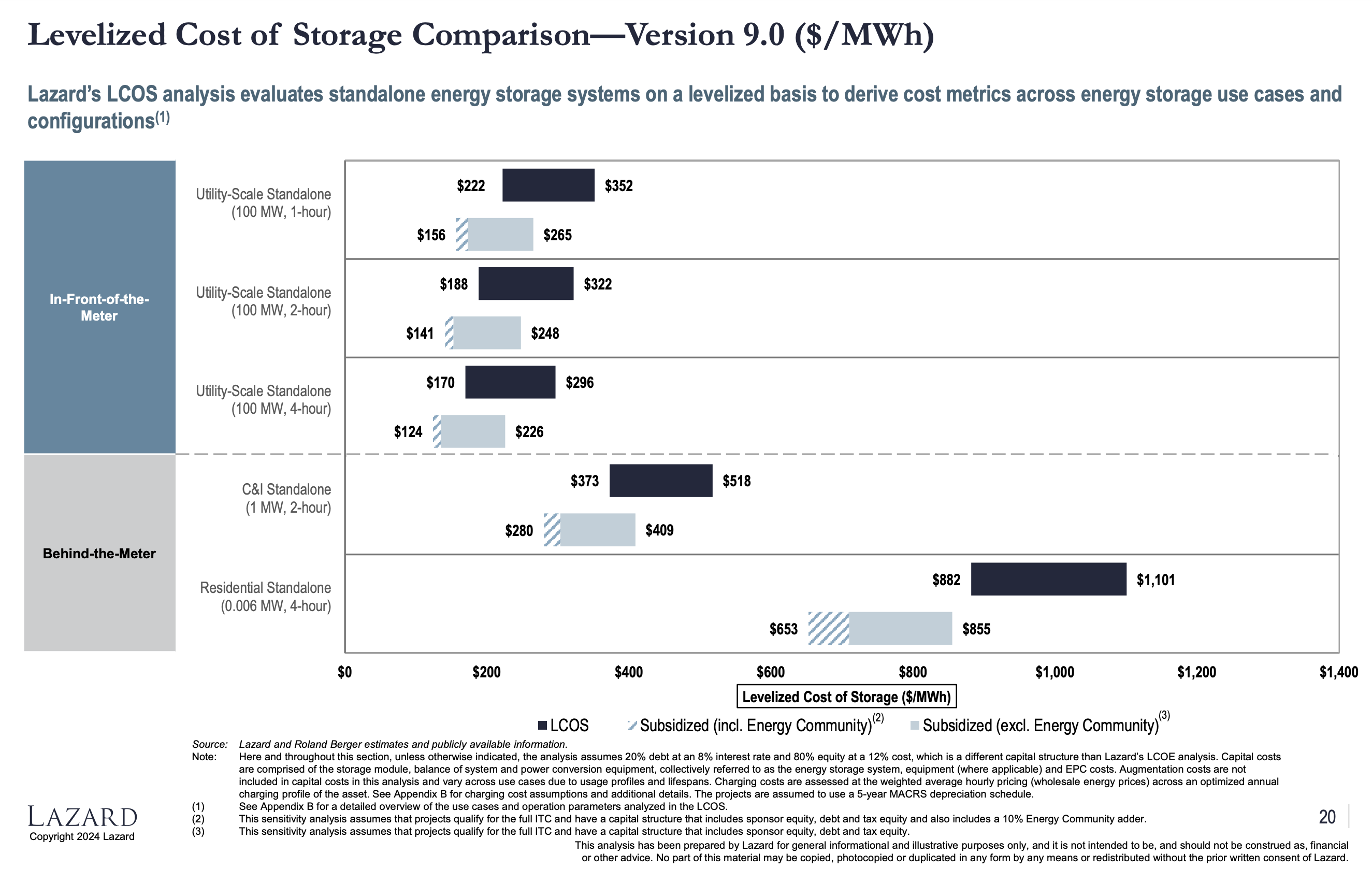

Looking through Lazard’s recent LCOE (levelized cost of energy) report, in addition to the key headline points on renewable energy costs vs. fossil fuel and nuclear energy costs, I ran across some interesting notes the analysts made about energy storage projects in the USA. In particular, Lazard highlighted some effects of the IRA (Inflation Reduction Act of 2022) which jumped out to me.

For one, the IRA is leading to larger energy storage projects that will last longer as their original battery capacities degrade and diminish. Notably, building larger projects that last longer, Lazard is projecting better long-term financial returns for the project owners. Overall, the point is that the IRA brings down energy storage system costs.

“Despite the significant increases in wholesale pricing for lithium carbonate and lithium hydroxide observed from 2022 to 2023, the IRA’s grant of ITC eligibility for standalone ESS assets kept LCOS v8.0 values relatively neutral as compared to LCOS v7.0. One year later, for this year’s LCOS v9.0, ITC implementation, including the application of energy community adders, is fully underway and the impacts are clear. The ITC, along with lower cell pricing and technology improvements, is leading to an increasing trend of oversizing battery capacity to offset future degradation and useful life considerations, which is not only extending useful life expectations but is also increasing residual value and overall project returns.”

Secondly, however, there have been some delays in projects moving forward as questions remained about battery supply chain rules. Time is money, and any delays in projects moving forward come with some costs, but hopefully that’s being cleared up if it isn’t already.

Thirdly, because of IRA regulations, Lazard expects more and more stationary battery storage projects will use battery cells and underlying battery materials that come from the US — rather than China, for example. Though, what’s unclear at this point is how these changes will influence costs. Of course, that will be a changing matter as well — using battery components produced in the US may cost more initially, but those costs should come down over time as battery component production scales up and industry synergy forms in North American regions.

“While the ITC and energy community adder are prevalent, the domestic content adder remains uncertain, notwithstanding the various domestic manufacturing announcements,” Lazard writes. “The lack of clarity related to qualifying for local content is leading to longer lead times and higher contingencies. Adding to this overall complexity is the recently proposed increase of Section 301 import tariffs on lithium-ion batteries, which many believe will lead to increased domestic battery supply but with uncertain costs results.”

So, that’s the story on storage. It was also discussed in combination with wind and solar in my first article about the new Lazard report. Check that out if you haven’t read it yet, or dive all the way into the full Lazard report.

Hat tip to “earwig” for sharing the new Lazard report with us and pushing for some coverage.

Related: Utilities: Batteries Are Most Commonly Used for Arbitrage & Grid Stability

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy