World Getting 120 New 1GW Nuclear Fusion Power Plants This Year! Or Something Like That …

Support CleanTechnica's work through a Substack subscription or on Stripe.

Well, that’s one way to put it. I have to give the credit to CleanTechnica reader “ElectricGuy” for this one. Yesterday, he wrote, “The world will add 120 new 1GW nuclear reactors this year. What a headline that would be!”

He was referencing a recent report’s estimate for solar power additions in 2024, and translating that to a nuclear power plant total assuming 20% capacity factor for those solar power installations. You could assume a higher capacity factor, or a lower one for nuclear, and it would be equivalent to even more than 120 new nuclear power plants.

Of course, nuclear power plants use nuclear fission. However, the sun generates its energy from nuclear fusion, so I got a little creative.

But let’s get to the actual solar figures and report summary.

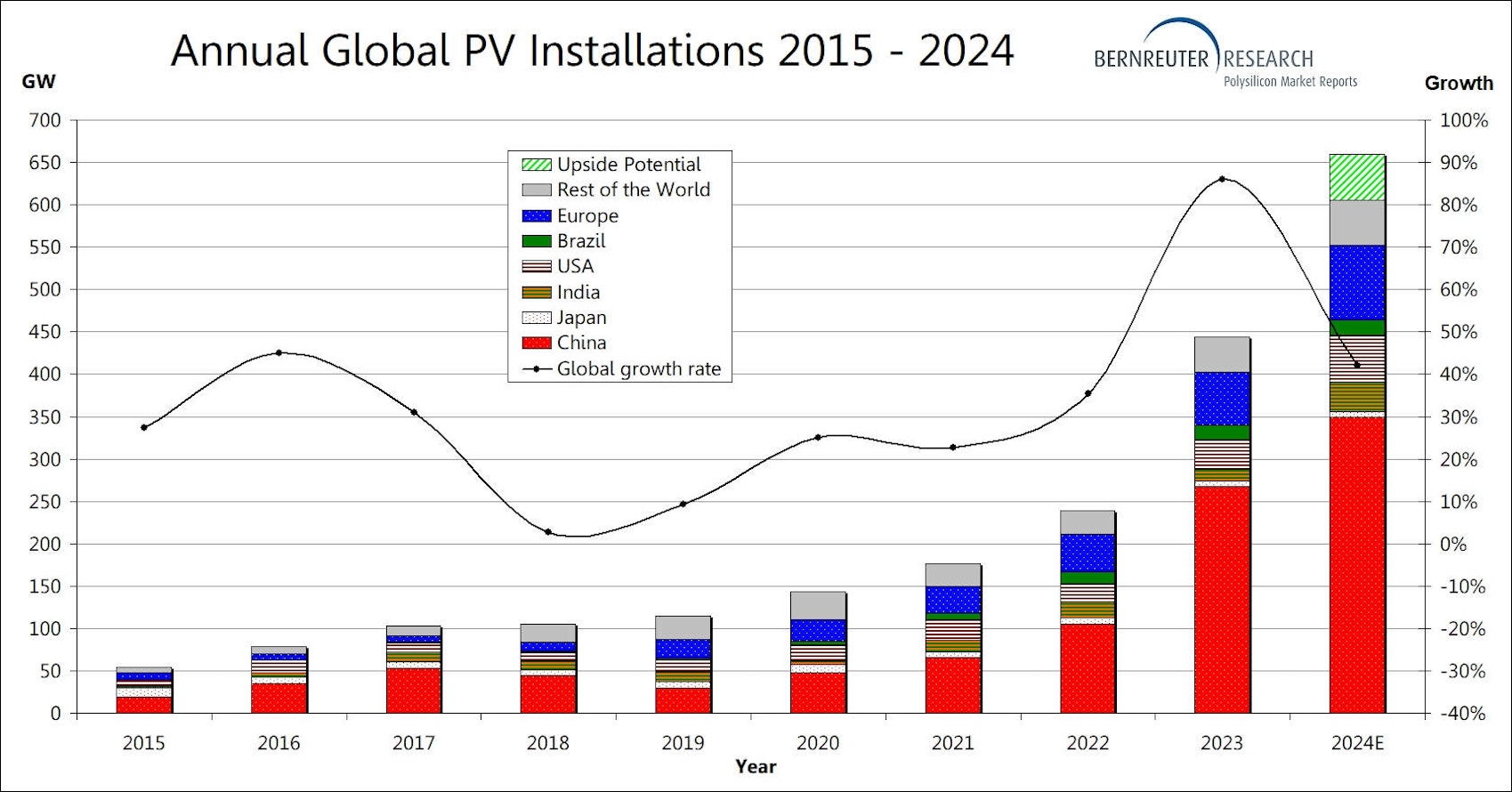

According to Bernreuter Research, 600–660 gigawatts (GW) of solar PV power capacity will be installed worldwide in 2024. That’s new power capacity, and it’s a significant increase from 2023, when nearly 450 GW of solar power capacity was installed. Though, at just about 40% growth year over year, it wouldn’t replicate the nearly 90% growth of the market from 2022 to 2023. Though, in volume terms the market grew by a little more than 200 GW from 2022 to 2023 and will again grow by a little more than 200 GW from 2023 to 2024.

Bernreuter Research highlights that much of the growth will come from big solar panel price drops finally tapering off. “Once market participants come to the conclusion that the crash of the solar module price has reached its bottom, demand will accelerate,” says Johannes Bernreuter, Head of Bernreuter Research and author of the Polysilicon Market Outlook 2027 report.

The solar research firm notes that the 2024 estimate is supported by the public solar module shipment targets from the six largest solar module producers in the world. “On average, Jinko, Longi, Trina, JA Solar, Tongwei and Canadian Solar aim for a growth rate of 40%. Based on global PV installations of 444 GWdc in 2023, this rate would result in a newly installed capacity of 622 GWdc in 2024,” Bernreuter Research writes.

“Even if the leading players gain market share as Tier-2 and Tier-3 manufacturers struggle in the current low-price environment, it is likely that new PV installations will exceed 600 GWdc this year,” says Bernreuter.

Solar module producers were a bit optimistic in 2023 and missed their targets for the year, so Bernreuter thinks they’re being more cautious this year and are thus likely to surpass their targets rather than miss them. We’ll see. “On the supply side, all indicators point to the upper half of our forecast range,” explains Bernreuter. “I am optimistic that demand will catch up in the second half of the year, fueled by the record-low module price level.”

So, they won’t be nuclear fusion or nuclear fission reactors, but they will be something much better — thousands of clean distributed solar PV projects spread around the world.

A special note goes out to China, though. As it has routinely done lately, China is expected to install more than 50% of the world’s new solar power capacity.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy