Coal Capacity Factor Drops from 55% to 35% in 10 Years in PJM

Support CleanTechnica's work through a Substack subscription or on Stripe.

Editor’s note: The war on coal is real, and it’s been happening on several fronts. Solar power is replacing coal. Wind power is replacing coal. Natural gas is replacing coal. At the end of the day, coal has been on a long, big decline in the USA. The following update from the U.S. EIA provides more info on that.

Use of the coal fleet in PJM, the country’s largest wholesale electricity market, has fallen over the last decade, driven largely by higher relative fuel costs. Much of the competitive pressure has come from the significant build out of efficient natural gas combined-cycle plants, the capacity of which has doubled in PJM since 2013.

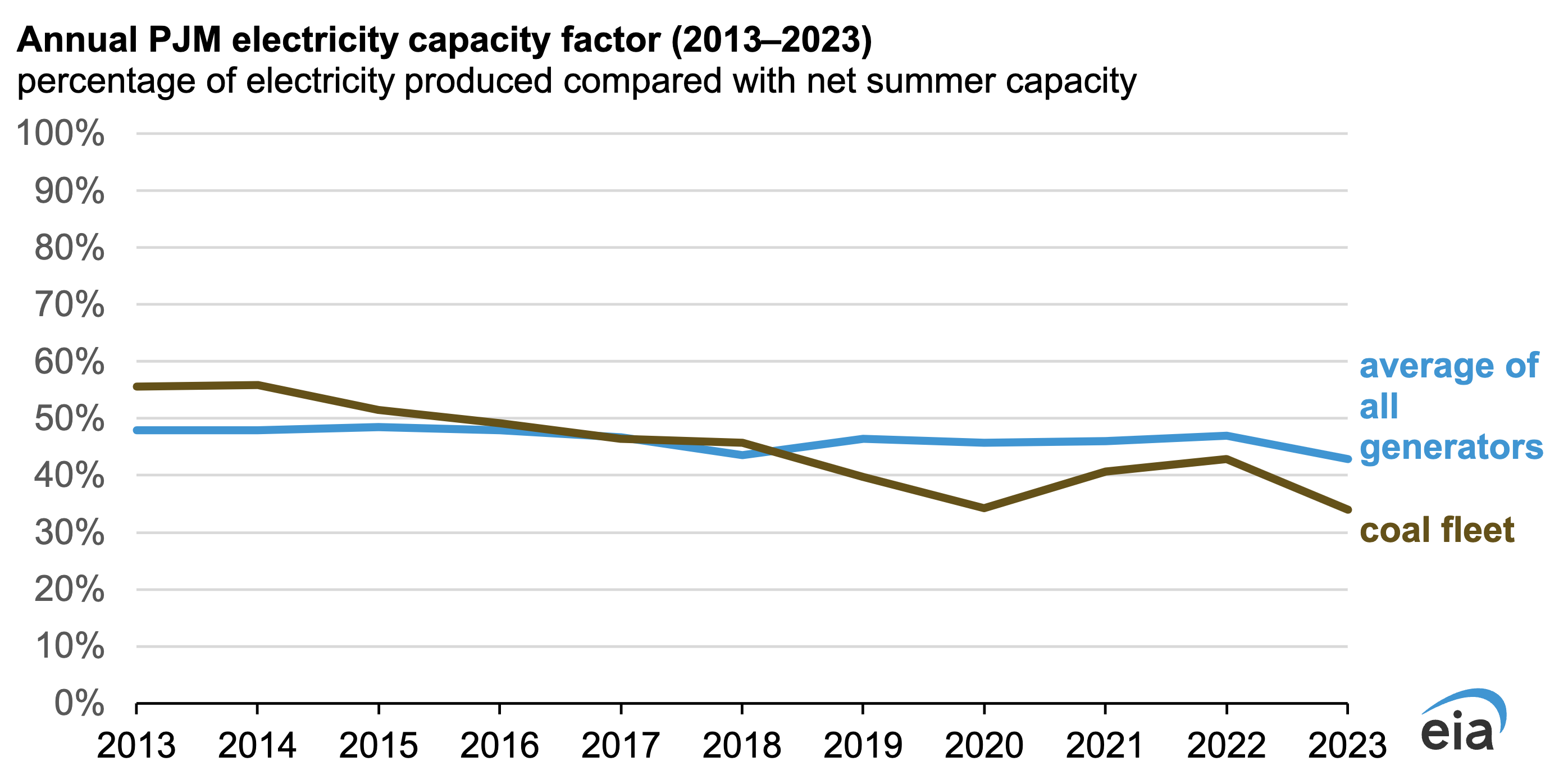

In 2023, the use of coal-fired generation in PJM dropped to 34% of capacity. In 2023, coal-fired generation contributed 14% of PJM’s generation, while it made up 18% of its generating capacity. By comparison, in 2013, the capacity factor of coal-fired power plants in the market was 56%, when coal-fired power made up 44% of the market’s generation and 38% of its capacity.

PJM is the largest wholesale electricity market in the nation, covering all or parts of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia, and Washington, DC.

Operating costs of competing resources are significant factors for PJM to determine which plants will run. How much the plant is called on affects operator decisions to keep coal-fired plants open. Other factors influencing dispatch and retirement decisions include local demand, wholesale prices, fuel supply contracts, maintenance costs, and debt service.

For coal, competitive pressure from other energy sources, particularly natural gas, has significantly reduced generation from PJM’s coal fleet, increasing retirements. Since 2013, operators have retired about 34 gigawatts (GW) of coal capacity in PJM and switched about 2 GW of coal capacity to other energy sources, mostly natural gas. Although PJM still has the most independent power producer (IPP) coal capacity in the United States, 17.6 GW, IPP coal plants accounted for most of the retired coal capacity in PJM since 2013, about 24 GW. As a result, the generation from IPP coal in PJM has fallen more than the generation from regulated facilities, which unlike IPPs, operate with cost recovery that tends to lower financial risk.

The same competitive pressures that resulted in coal retirements have also reduced the capacity factors at the remaining coal plants due to less time operating. PJM coal plants can be grouped into those that have dispatched a lot and those that operate less often.

In 2023, 11 coal-fired power plants made up more than three-quarters of the coal-fired generation in the region. These plants were offline relatively infrequently, operating on average 330 days out of the year and averaging only three shutdowns, each with an average duration of about a week. Output from the other 22 PJM coal plants with outage data varied more by season. Those plants operated for an average of 175 days in 2023, shutting down nine times, each with average durations of about a month.

Coal-fired generating units are generally designed for steady state operation, and they operate with the fewest problems when they run all the time. Restarts can be costly because large thermal plants can experience problems caused by repeated startups and shutdowns, increasing maintenance costs. The restart cost can be a key factor in determining plant operating strategy. Most coal-fired power plants are required to offer into the PJM day-ahead market used to dispatch plants. Because those restart costs increase their market offer, coal plants, when competing against other sources, may not be selected to operate.

Coal is currently the third-largest energy source in PJM behind natural gas and nuclear, and its participation remains significant. However, the effects of increasing competitive pressures from both natural gas and renewables are evident as operators plan to retire nearly 20% of current coal capacity in PJM by 2028. The output from the rest of the coal-fired capacity in PJM will likely continue to reflect a diversity of run times.

Principal contributor: Glenn McGrath. Originally published on Today in Energy.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy