Top Selling Electric Vehicles in the World — January 2024

Support CleanTechnica's work through a Substack subscription or on Stripe.

The Tesla Model Y is #1 again in the electric vehicle market. Registrations were up 63% year over year (YoY) in January, to over a million units. China’s market was the main driver of growth.

Share-wise, 2024 started with plugin vehicles getting 16% share of the global auto market (10% BEV). The global market was helped by significant volumes in markets outside the spotlight being on the upswing, like Thailand (+239% YoY), Turkey (+219%), and Brazil (+263%).

With a price war happening in several markets, and other markets receiving new, cheaper models, expect the global EV market to continue growing at a solid pace. We could end this year at above 20% EV market share (15% BEV market share).

Last month, BEVs grew by 48% YoY, while PHEVs were up by an amazing 91%, mostly thanks to the increasingly PHEV-friendly Chinese market. What happens in the Chinese market is always important globally — this market represented over 60% of all global sales of electric cars in January. One should highlight that most plugin hybrids in China are a different beast compared to those in the rest of the world. In reality, most are range-extended vehicles, with large batteries sized between 30–40 kWh. They even typically include fast-charging capability.

These events placed the initial BEV vs. PHEV breakdown at 61% to 39%, somewhat below the average of recent years.

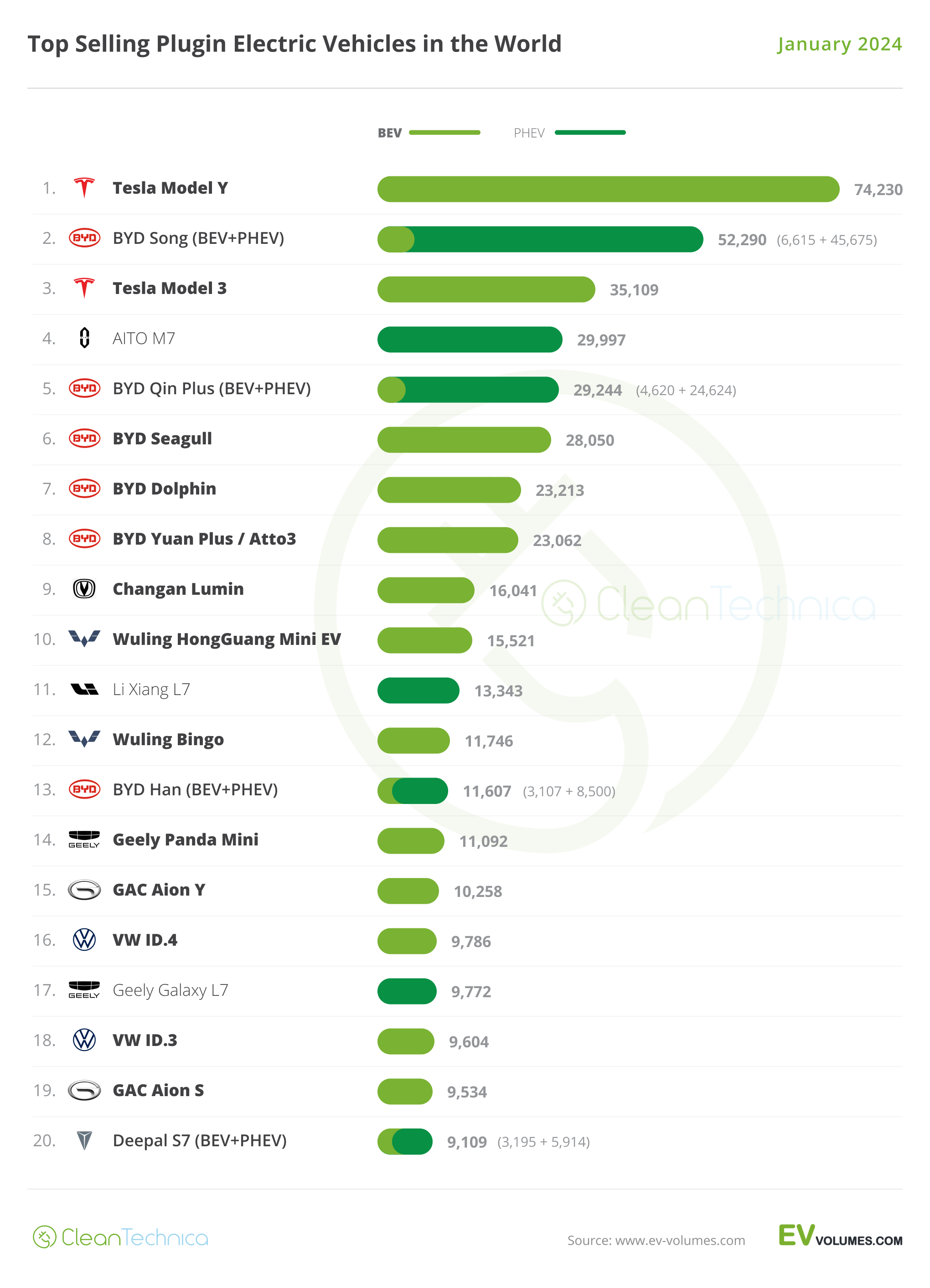

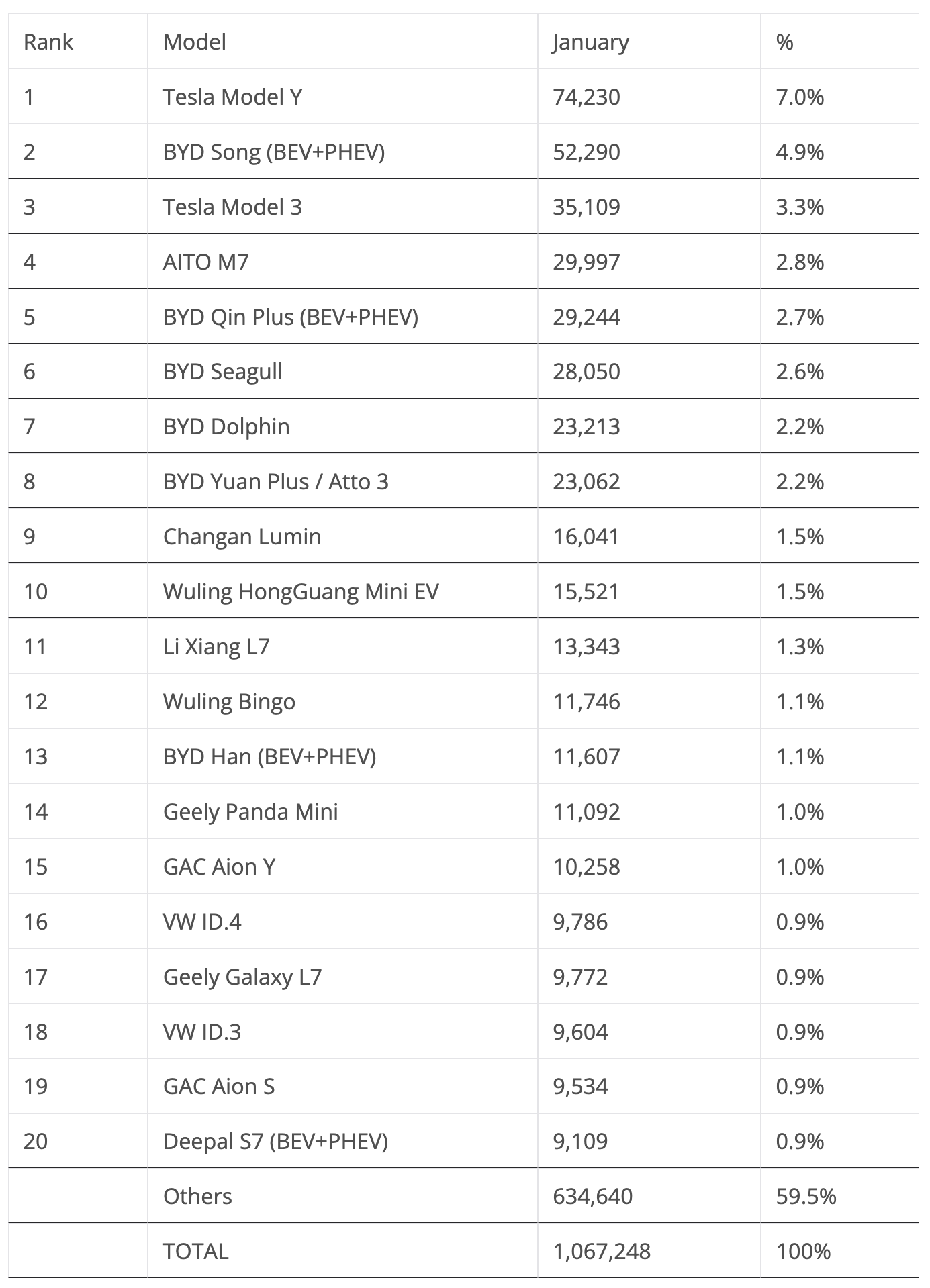

The Model Y started the race right at #1, while in the runner-up spot, we have the BYD Song, starting the year in the same place as it ended the previous one. But with internal competition heating up, namely with the ramp-up of the Song L and the upcoming Sea Lion 07 BEV, one wonders if the Song will suffer the same destiny that its Qin Plus sedan sibling suffered — becoming a cash cow for the company, but no longer its star player.

In the last spot on the podium, the Tesla Model 3 also had a good start of the year. It will be interesting to see how much of a kickback the refresh will have on Model 3 demand. Let’s not forget that the sedan is now on its 7th year….

Off the podium, the highlight is without any doubt the AITO M7, with the Huawei-backed model landing in 4th globally in January. Not bad for a full size SUV only sold in China! What’s more, in January, the almost 30,000 deliveries represented a 9,000-unit increase over its previous record, which was set in December…. And while February will be a slow month, due to the Chinese New Year, one wonders how many units of the AITO SUV will be delivered in March. Should the #3 Tesla Model 3 be worried?

Elsewhere, it is the usual BYD armada, with four models coming from the Shenzhen brand between the 5th and 8th positions.

The second half of the table looks more interesting, starting with the two Geely models. The crossover Galaxy L7 was in 17th, with 9,772 registrations, while the slightly smaller Panda Mini was 14th, with 11,092 registrations. With the Galaxy L6 sedan also on the rise, having registered a record 6,389 sales in January, Geely finally seems ready to go after the big boys. It is helped by other models in the Geely galaxy, like the Lynk & Co 08 (8,816 sales), the Volvo XC60 PHEV (7,523 sales), and the much-hyped Zeekr 007 sedan (currently at some 6,000 sales, but likely to soon cross north of 10,000 sales a month).

Another model impressing was the #20 Deepal S7 SUV (3,195 units of which were the BEV version). Changan’s upmarket brand had its star model in the top 20 and should continue to be a regular presence in the coming months. The VW ID.3 also showed up, in this case at #18, making it the second Volkswagen model in the table.

With AITO and Geely models on the rise, BYD’s domination in the table is starting to fade. As an example, 12 months ago, BYD had 9 models in the top 20, while now it has “only” 6 representatives.

So, is the table finally becoming more diverse? Fingers crossed….

Outside the top 20, a reference goes out to the new BYD Song L, which ended the month with 7,374 sales, in only its 3rd month on the market. Expect it to rise into the top 20 soon, maybe even in March?

Another model on the rise is GAC’s Trumpchi E9 PHEV, a large MPV with a very … peculiar styling that had a record 6,686 sales in January. Expect it to provide some competition for the current MPV category king, the Denza D9.

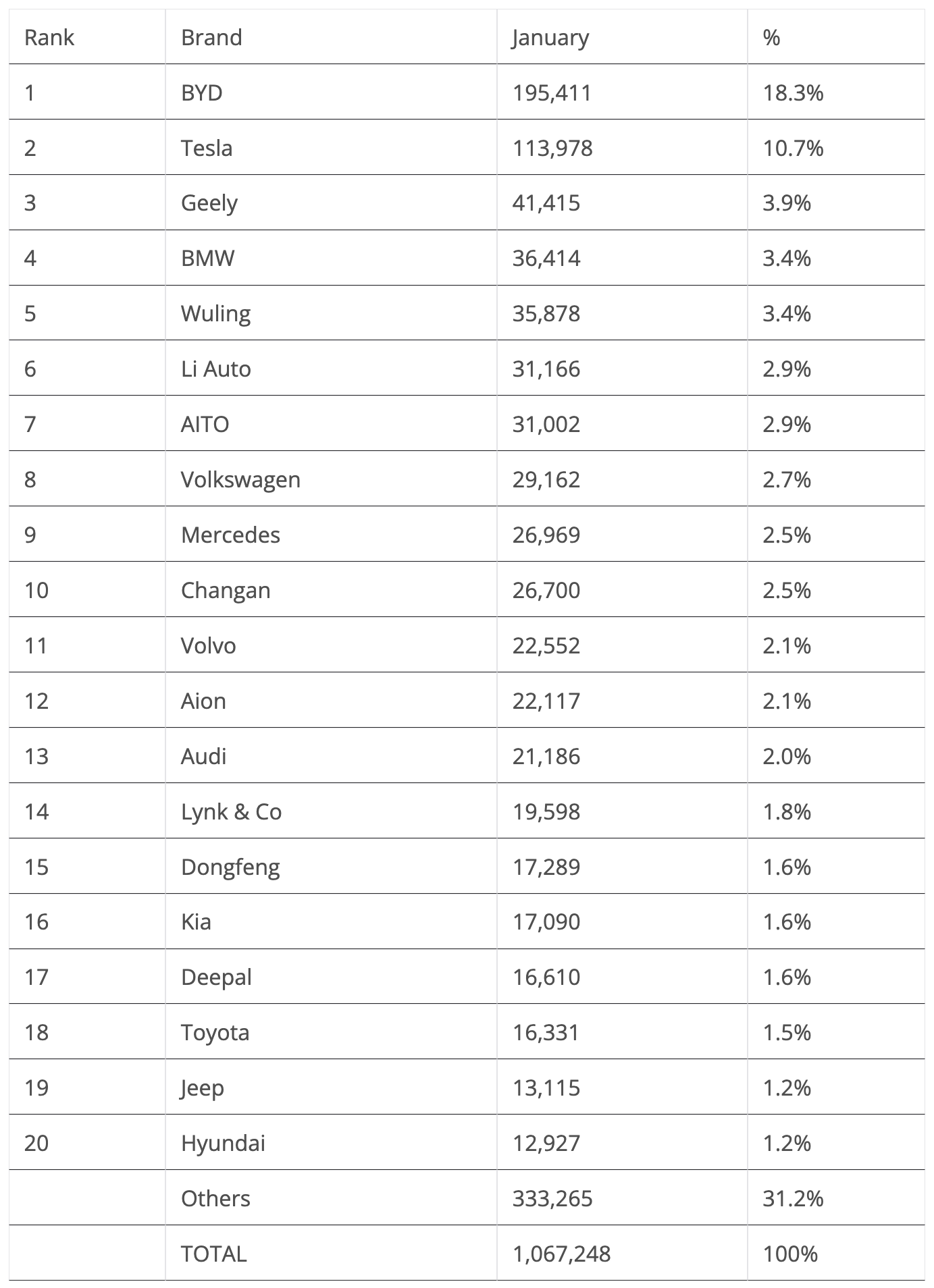

Manufacturers: BYD Starts Ahead

January saw BYD win the monthly manufacturer title, thanks to 195,000 registrations, ending with a comfortable lead of more than 80,000 units over runner-up Tesla.

But it seems the two usual galactics could have a competitor sometime in the future, in the form of … Geely.

About the aforementioned Geely. The Chinese make was the biggest surprise in January, jumping into the 3rd spot with over 40,000 registrations. This is mostly thanks to the ramp-up of the Galaxy lineup (the L6 and L7, and the introduction of the E8 flagship), which added to the sure volumes of the Panda Mini EV. The rest of the lineup will make Geely not only a strong candidate for the podium, but it could also make Geely the first automaker to try to go after the top two.

Regarding the remaining positions at the top, the biggest surprise is AITO jumping to 7th, dangerously close to arch-rival Li Auto in 6th. Both premium Chinese makes beat Mercedes (9th), but also … #8 Volkswagen?!?! Ouch…

Another brand on the rise is #14 Lynk & Co, with the Chinese make benefitting from strong sales of its 08 SUV.

Looking at legacy OEMs, the Koreans had a slow start, with #20 Hyundai inclusively being beaten by #18 Toyota(!) and #19 Jeep(!!!) — yikes! In the latter case, the US brand continues to benefit from strong results coming from the Wrangler PHEV (6,003 sales in January).

With US EV incentives being quite generous to PHEVs (one could almost say that Stellantis whispered a few words to the legislators who wrote the details of the incentives…), expect Jeep to surf the “IRA wave” and continue growing its sales significantly.

Just outside the top 20, we have another brand from the Geely galaxy shining, with Zeekr (12,719 units) ending some 200 units from #20 Hyundai. So, we could have four brands from this OEM (Geely, Volvo, Lynk & Co, and Zeekr) on the table soon.

Leap Motor (12,392 sales) is also close to the table, so the upcoming C10 SUV could pull the startup into top 20 territory.

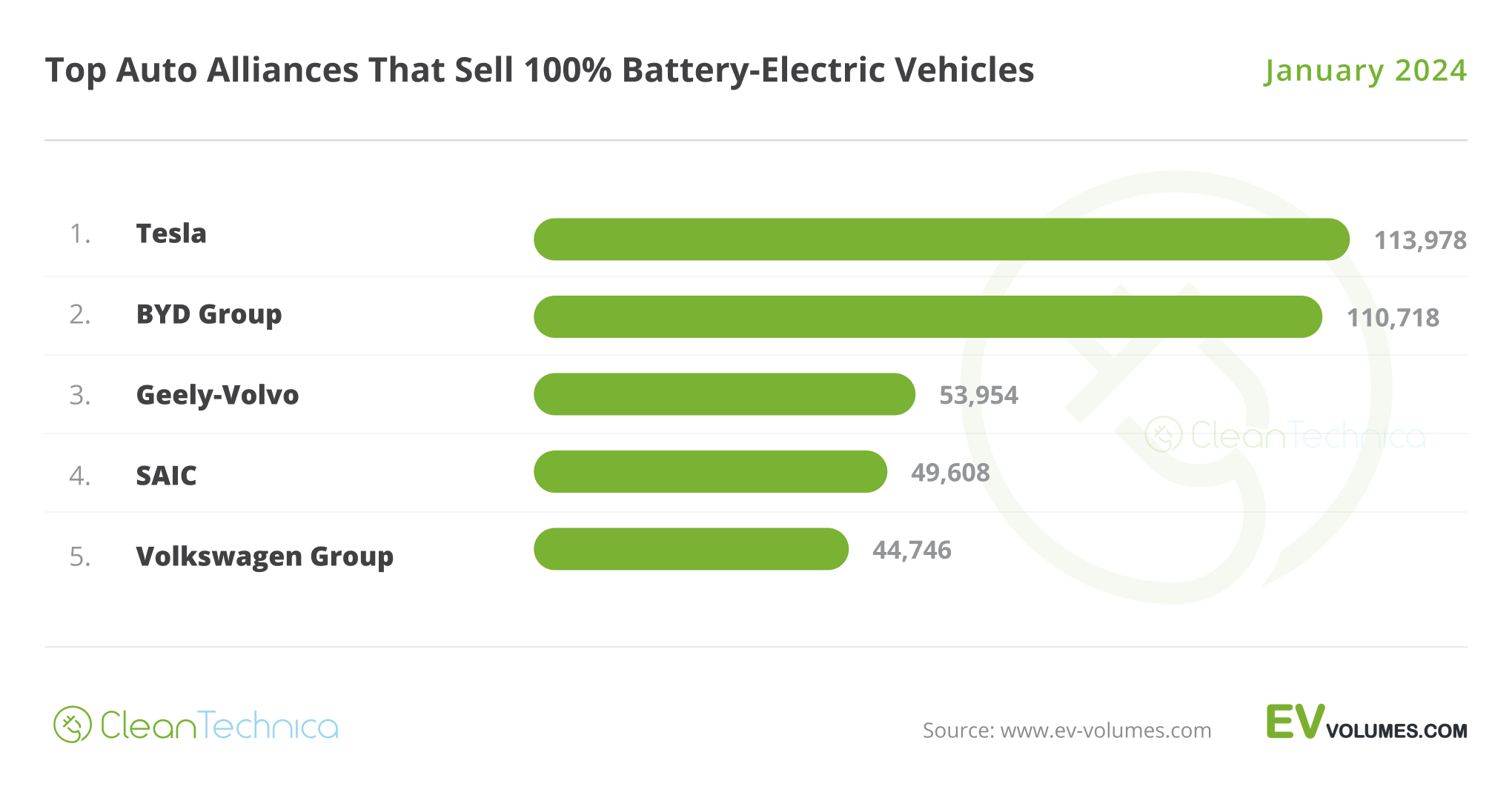

Looking at OEMs, BYD (19.8%, down from 22.7% in December 2023) is once again starting out ahead, with Tesla (10.7%, down from 15.2%) in the runner-up position. Both galactics lost share year-on-year in January. Could this be an early sign that the plugin market is becoming more balanced?

On the other hand, Geely–Volvo (9.7%, up from 5.8% a year ago) had a breakout month, reaching close to 10% share in January. We might see it have a try at reaching Tesla’s #2 position. Although, one thing is trying, another is actually getting there. … To be continued.

An ever more distant Volkswagen Group (6.2%, down from 7.5%) started the year in 4th, a place below its standing in January 2023. At this point, the best that Volkswagen Group can expect is to retain the #4 spot. Which, by the way, won’t be easy, as SAIC (6.1%, up from 5.1% share a year ago) benefited from a strong month from Wuling and IM Motors. At the same time, with SAIC making important inroads in Europe thanks to its MG brand, we could actually see the Shanghai OEM surpass Volkswagen Group soon….

Outside the top 5, Changan (4.7%) started 2024 in 6th, replacing the usual Stellantis (3.7%) in that position.

Looking just at BEVs, there were 648,115 registrations in January, or 61% of total plugin sales. Both Tesla and BYD started in the same positions they held in 2023, but more importantly, the market share between both narrowed in January, with the former dropping from 22.8% to 17.6% and the latter rising from 16.1% to 17.1%. With only 0.5% share separating the two of them, things have really gotten interesting….

With the Chinese New Year this year falling in February, expect BYD to have a slow month, allowing Tesla to gain some ground, but it will be interesting how both will behave in March. Bring on the popcorn!

… And while the top two are in their own particular race, something big happened behind them. Geely–Volvo (8.3%, up from 5.1%) jumped from 5th a year ago to its current 3rd place. Is this here to stay? And will Geely–Volvo be able to go after the top two?

On the flip side, last year’s #3, Volkswagen Group, had a slow start (6.9% vs. 7.8% in December 2023). It began 2024 in the 5th position, behind #4 SAIC (7.7% now vs. 6.9% then). So, the best selling legacy OEM in the BEV ranking is only … 5th. Interesting, uh?

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy