DNV/FT Grid Storage Report Is A Good Snapshot of Global Thinking

Support CleanTechnica's work through a Substack subscription or on Stripe.

Several months ago, the international accredited registrar and classification society DNV and the Financial Times subsidiary FT Longitude team working on a global industry survey and report related to grid storage reached out to me to gain my perspective. Time passes, as it does, and the report, Closing the Energy Storage Gap, has hit the street.

436 senior energy professionals from around the world, 30% of them C-suite, covering core industries of electrical power, renewables, oil and gas, and industrial energy consumers, answered an extensive survey. Six industry professionals including me were interviewed in more depth on specific points to provide context and flavor.

Almost half of the surveyed group indicated that they were actively researching and/or piloting energy storage opportunities. 35% indicated that they were an energy storage technology or equipment provider. About a third were investors in energy storage projects or technologies. One interesting finding was that about a third of oil and gas firm respondents expect to own or operate energy storage assets by 2026.

Unsurprisingly, permitting and profits topped the list of barriers. Grid storage assets typically require transmission grid connections, and those are an inhibitor to the energy transition in most geographies. There’s more to this, of course, as many storage technologies shade into other complex regulatory areas, for example pumped hydro in the USA, where four different national agencies have to approve anything bigger than a duck pond if it has a dam attached.

And profits, as I’ve discussed with entrepreneurs, investment funds, and deployment firms globally, require a regulatory structure that enables revenue. For basic assets, that’s at least a capacity market and preferably day-ahead reserve markets and ancillary service markets. The emergence of sophisticated market structures covering larger geographies is patchy globally, and often involves two steps forward and one backward. Case in point, the UK, which has been a leader in grid regulatory and market innovation, for example its new inertia market, but now is striding powerfully into the past with more oil and gas extraction, backing off of its climate targets and deferring things like elimination of new gas and diesel vehicles.

Long-life assets like pumped hydro require regulatory and market structures that enable them to gain sufficient commitment for revenue to bank investments and debt financing. The UK has been almost about to put in place a cap and floor structure for a couple of years, something which would match regulated asset base inclusion of carbon capture and nuclear projects, but that’s less likely now it seems.

Lithium-ion batteries are hot right now across storage and transportation, and with the exponential curve of electric vehicle growth vs the multiple years to develop hard rock or unconventional lithium extraction and processing, there’s a timing gap. That’s a temporary problem, but it’s also indicative of where the markets are today. Other issues are utilities’ resistance to change and technology confusion.

Almost 90% of respondents from every industry group thought grid storage and long-duration storage were important for grid stability and areas which required accelerated development and deployment in the coming five years.

The graph of responses above caught my eye. It’s important to call out the three-year timeframe. It’s also important to say that while the question was clear, that doesn’t mean everyone read all the way to the end and internalized the timeframe before responding.

That said, there were some surprises in this response. Lithium-ion batteries dominating certainly wasn’t one of them. Cell-based battery systems, while not suitable for longer duration storage, are excellent for the grid requirements today of moving duck curve electricity into the evening and fast response peaking supply. Long duration storage is an end game of the decarbonization requirement, not a precursor. That said, the more we have sooner, the faster we can retire fossil fuel plants providing day-ahead storage, so there’s a bit of a horse race going on.

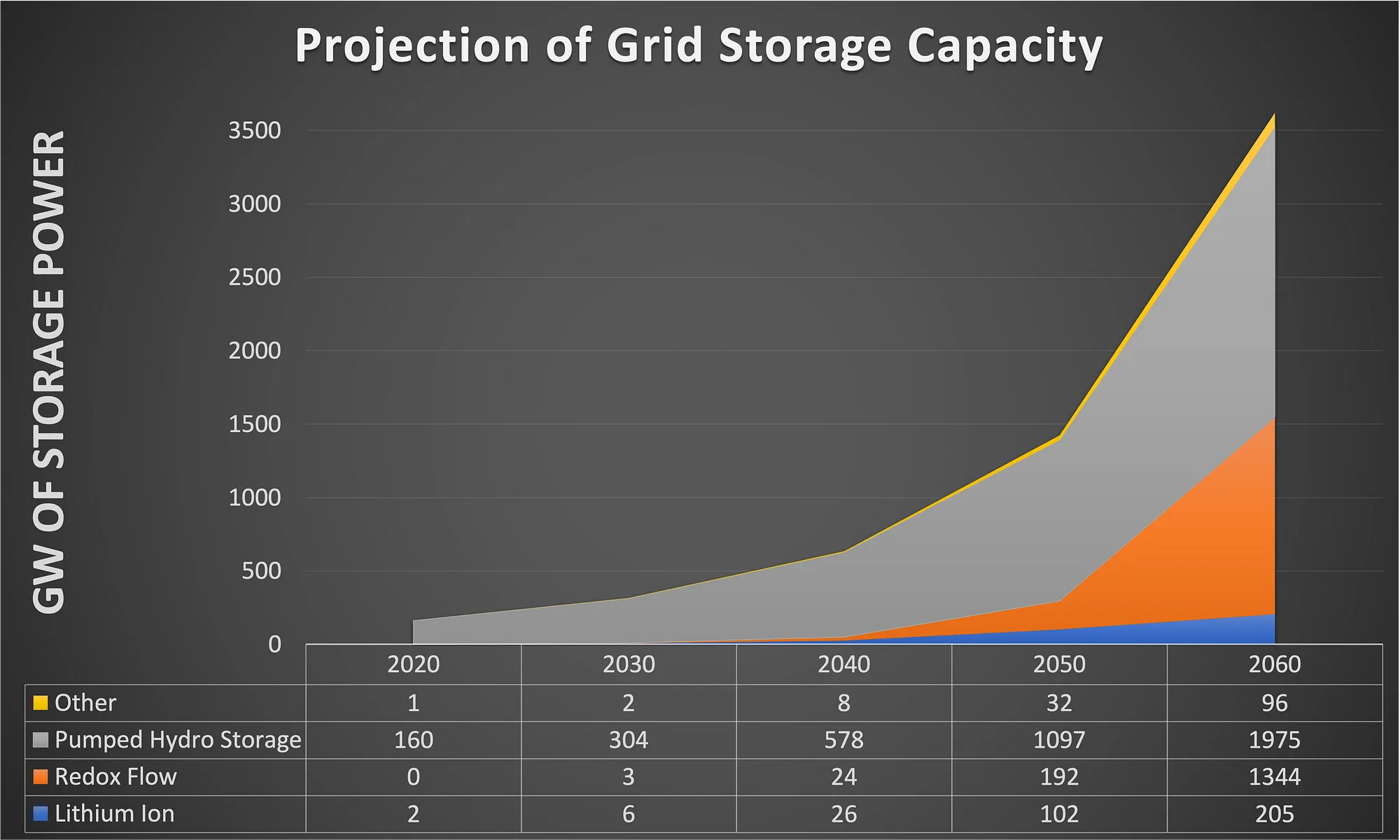

I was very pleased and somewhat surprised to see that six out of ten respondents were focused on pumped hydro. That’s indicative that they are actually focused on grid storage and have navigated through the hype and noise to what actually works. Personally, I think it’s an indicator of quality of the process of selecting professionals to respond, as so many people further from the action don’t realize that pumped hydro dominates grid storage today, dominates grid storage construction in terms of energy and power today and that it’s likely to continue to do so as we move forward.

As a reminder, closed-loop, off-river pumped hydro is my projected leading technology for all power and energy requirements for grid storage in the coming decades.

I was interested to see that fewer respondents were expecting their regions to spend time or money on green hydrogen for storage in the coming years — only five of ten. Given how much hype there is for the necessary industrial feedstock and major climate problem becoming a primary energy carrier, it’s a good sign that the hype cycle is moving through its stages toward sanity prevailing. It’s also likely that the 13% of respondents from the fossil fuel industry were all bullish on hydrogen as a store of energy due to their own biases and inflated that number.

And it’s hard to say if they meant that they were focused on green hydrogen for storage solely, or were conflating this with green hydrogen as a necessary industrial feedstock. Another table breaks out expected investments in the technologies in the next year, and green hydrogen was removed due to so many organizations investing in it for actually useful purposes, not as a store of energy.

That said, KEPCO from South Korea is very bullish on hydrogen for energy, something South Korea and Japan share as an irrational energy choice. It’s going to be problematic, as both expect to import a lot of hydrogen, and the best case scenario is that hydrogen will be five times the cost of imported natural gas, the current most expensive form of energy. Importing high-efficiency electricity through HVDC to supplement locally generated renewable energy and using it directly in electrified energy services end uses will power the economies of the future, and that’s a much, much cheaper energy pathway than any hydrogen pathway.

For very long duration grid storage, there might be an argument for green hydrogen over just using the water directly and pushing it uphill over and over instead of wasting a lot of energy turning it into a gas that really wants to escape and cause global warming. But if I were going to be storing a gas for the dunkelflaute, I’d probably divert anthropogenic biomethane into salt caverns instead. It’s much less likely to leak and we don’t have to worry about it exploding nearly as much. Much cheaper to capture and store a problematic waste gas instead of manufacturing a new and much more expensive gas, most likely.

Very long duration storage, a couple of weeks of almost complete energy backup, is a once-every-ten-years concern in the archipelago nation of the UK in its position in northern Europe, but a once in every 50 or 100 year problem on continents. Niche in any event. As others have pointed out, also not something we have to solve today, as we’ll keep burning natural gas in ever diminishing amounts year over year, but that doesn’t mean we shouldn’t keep the natural gas reserves full as a contingency.

Four of ten respondents expecting investment in redox flow batteries is interesting, because I don’t think they’ll have much of a play for the next three years. As a reminder, I was strategic advisor to Agora Energy Technologies with its CO2-based redox flow battery for a couple of years, and redox flow batteries are #2 on my list of dominant storage technologies. I know the maturity of the technologies in that segment and the scale of deployments fairly well, and my expectation is that the redox market will start taking off in 2030. But three in ten respondents expected their organizations to increase investment in redox technologies in the coming year.

After that, there are only a couple of comments. Lead acid showing up so high on this list as a grid storage technology was interesting. Perhaps because I focus on the end-game and come backward as an approach, and don’t expect that chemistry to have a play at all in 2100, I ignored it. But I just don’t think it has much of a play in grid storage today. Perhaps it’s a country-specific thing, and India has a lot of it. If someone knows, please advise.

For the next three years I expect lithium-ion to dominate sodium-ion as cell-based batteries for grid storage. In the longer term, I expect sodium-ion will dominate for this use case. We’re already starting to see significant differentiation of technologies across storage use cases, and sodium’s qualities are well suited to stationary, same-day storage applications. Lithium is excellent for almost all ground and marine vehicles, while silicon chemistries are going to start dominating aviation and longer-haul freight transportation. The respondents did pick sodium technologies as the second biggest area of increased investment in the coming year, so there’s a clear recognition of its merit. And clearly I have to update my grid storage projection to abstract lithium-ion to cell-based technologies at some point.

Thermal storage was a bit of a head-scratcher at almost five in ten respondents pointing to it. The thing is, storing electricity as heat and then extracting electricity from the heat is really inefficient. You have to go through the low efficiency steam cycle to get electricity back, and it doesn’t make much sense. Thermal storage behind-the-meter for applications that require heat make a lot of sense. Residential, commercial, and industrial heat solutions that turn electricity when it’s cheap into stored heat in low-tech solutions like well-insulated water, bricks, and sand for later use often pencil out well. But turning the heat back into electricity, which is the point of this report? I’m not seeing it. (Note: discussions in the past year have led me to believe that in some industrial applications leveraging a store of heat for heat’s sake to also generate a little electricity might pencil out, but I haven’t worked through a business case that proves that yet.)

And then there’s solid mass gravitational energy storage, aka Energy Vault and all of its either completely nonsensical or completely niche siblings. I suspect that has the same provenance as the 50% green hydrogen head-scratcher on the list, in that it’s getting a lot of hype and people just aren’t doing the math, so it was voted up despite the lack of merit. A remarkable one in ten respondents are expecting that their organizations will waste money in this space in the coming year.

The report is a useful snapshot of where pertinent global sectors are going to be spending their time and money, and where they are going to directing their bright engineers and spreadsheet jockeys to pay attention. But the 13 grid storage technologies should be five, and that’s why one of the biggest barriers to progress right now is confusion over the optimal technology to pick.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy