Solar is King 2023 — 50% Global Growth Predicted

Support CleanTechnica's work through a Substack subscription or on Stripe.

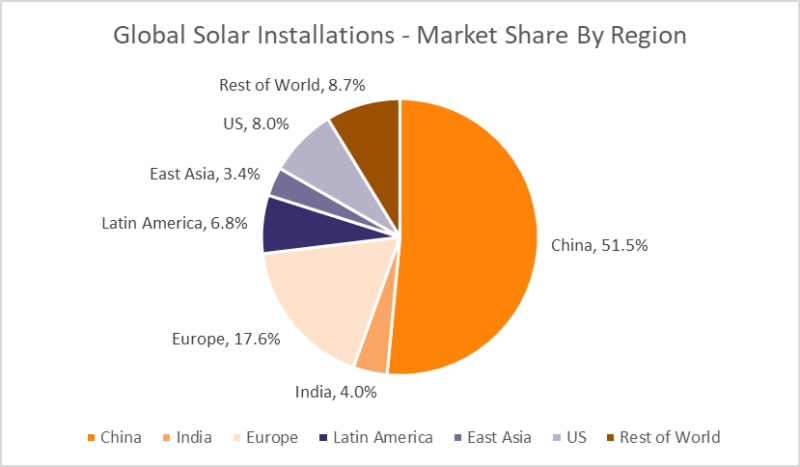

From the resources of Rethink Energy, we learn that in the second quarter of 2023 alone, approximately 92 gigawatts (GW) of solar power were installed globally. Of that, 55%, or 51 GW, was installed in China. Quarterly global solar installations appear to be growing at 50% per annum over the past three years. China has about 52% global market share.

“China’s solar industry is operating at a 93.6% annual growth rate, looked at through the 12-month rolling average – or if you compare the first six months of 2023 to H1 2022, then the pace of installations has more than doubled, accelerating 154%.”

“Since China installed 78.41 GWac (91.9 GWdc) in H1 2023, that means it will install 200 GWdc in the full year of 2023. And the rest of the world will install 160 GW — with 60 GW from Europe, 30 GW from the US, 17 GW from India, 20 GW from Latin America (mostly Brazil), 12 GW from Japan-South Korea-Taiwan, 4 GW Australia, and at least 10 GW from everywhere else.” The world is thus on track to install 360 GW of solar power in 2023.

Europe, with a 17.6% market share, had a bit of an up and down story in Europe. Germany, Italy, and the Netherlands have made good gains in installation growth, while Spain and Portugal appear to be constant, and France has reduced the number of GW installed compared with 2022. The UK has improved marginally.

The USA (with 8% market share) and Australia have made about a 20% improvement year over year (YOY). India (4% market share) appears to have slowed by about 15%.

Latin America, led primarily by Brazil, grew in market share from 6 to 8%. Brazil and Mexico doubled their amount of GW installed from 2022 to 2023. While Chile only installed half as much solar in 2023 as in 2022.

Rethink Energy believes that the 360 GW prediction may be a tad conservative considering that 312 GW have been already installed in the past 4 quarters. The second half of the year tends to be more active, especially in China, so the final figure may be closer to 380 GW. This will be more than 50% higher than total installations in 2022.

Compare this with the predictions from other forecasters, though — Wood MacKenzie is predicting that 2023 will only see 270 GW installed globally, with China maintaining similar growth to H1 and the rest of the world following suit. Wood Mackenzie predicts that Rethink Energy’s global growth target will not be reached until 2032! We won’t have long to find out who is right in the battle of the energy forecasters.

Andries Wantenaar of Rethink Energy points to ever-increasing polysilicon production in China. It is doubling year on year, to 120,000 tons in June 2023. He reports that more than 40 GW of imported solar modules are stockpiled in European warehouses. European imports of solar modules have tripled in the past 2 years. These realities point to a surge in PV installations in H2 2023. He acknowledges that there may be a slowdown in Chinese installation activity but argues that this is unlikely to come until 2024 or 2025.

“And Chinese solar will slow to ‘only’ 10% growth at worst — it’s a country with over 1,000 GW of coal capacity to replace while power consumption grows at least 4% annually. Its two big solar schemes of ‘desert base projects’ and ‘Whole County promotion,’ for utility-scale and distributed segments respectively, span the Fourteen Five-year Plan period of 2021-2025 and extend through to 2030 — they have only just taken off, and they have a total scale of hundreds of GW each.”

Despite the fact that Europe’s solar boom is running into transmission and workforce limitations, there is still a 31.5% year-on-year growth rate for H1 2023 in just 8 markets that are tracked by Rethink Energy. The untracked countries are just beginning to add solar — they are going from 0 to 1, effectively. “The overall European growth rate is 50% this year, just as it was in 2022.”

In contrast to the predictions by Wood Mackenzie, Rethink Energy asserts that the solar industry isn’t likely to have “one year of rapid growth followed by being stuck at below 400 GW through to 2030. It is growing consistently to 1,000 GW per annum by 2030, with tens of billions of dollars invested so far this year in manufacturing capacity.”

Just look at the impact of the IRA on the US market. “Since passage of the IRA, companies have announced more than $13 billion in U.S. factory investments, according to the Solar Energy Industries Association (SEIA).” Here’s just one example on CleanTechnica.

With COVID-19 shutdowns behind us and markets settling after the initial energy shock of the Russian invasion of Ukraine, it is likely that the 50% growth rate in solar installations will ease. However, there are still some growth drivers to consider: solar module prices have fallen by 30% since November 2022, quality and efficiency continue to improve, they are better supported by energy policy and storage each year, and new markets are opening up across the world. Many countries are going from 0 to 1.

“Besides China, the swiftest-growing large markets are Italy, Brazil, Germany, and Spain. … The stagnant markets are certain European and East Asian markets which are running into land use, workforce, and grid connection constraints.

“The two biggest contracting markets, the US and India, are bracing for a rapid acceleration — their decline is caused by trade interruptions and subsidies (discouraging premature development). We will see both grow rapidly in the second half of this year, then much more swiftly in 2024, and they are also both successfully on track to use domestically manufactured modules. In India’s case, this uptick may already be visible in the figure for June 20233, if it’s not random variation. Both countries have seen a modest swing towards distributed installations. In the US this has stabilized at around 50%, while India’s rooftop installs have reached over 2 GW on an annual basis, below 15% of the total.”

Rooftop installations in China have dipped back below 50%. The boom there is obviously due to “multi-GW” complexes mixing photovoltaics, wind, and energy storage, especially in the northwest of the country.

Sitting on my back deck in Brisbane, Australia, I am surrounded by rooftops decorated with solar panels. I check the NEM widget and am informed that Australia’s main grid is running on 58% renewables. Unsurprisingly, since it is near mid-day, the bulk of that is solar. As we move towards a solar-powered, low-carbon future, we can all do our part. Mitigating climate change is not a spectator sport.

Featured image via Rethink Energy

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy