Real Green Steel Progress

Support CleanTechnica's work through a Substack subscription or on Stripe.

UK think tank ReThink Energy has produced its latest report on the transition of the steel industry, Green Steel Premium, Myth or Reality. Real green steel is possible, and now probable. They look at the effects coming from the Russian invasion of Ukraine and the subsequent impact on the price of energy, as well as the impacts of the US Inflation Reduction Act.

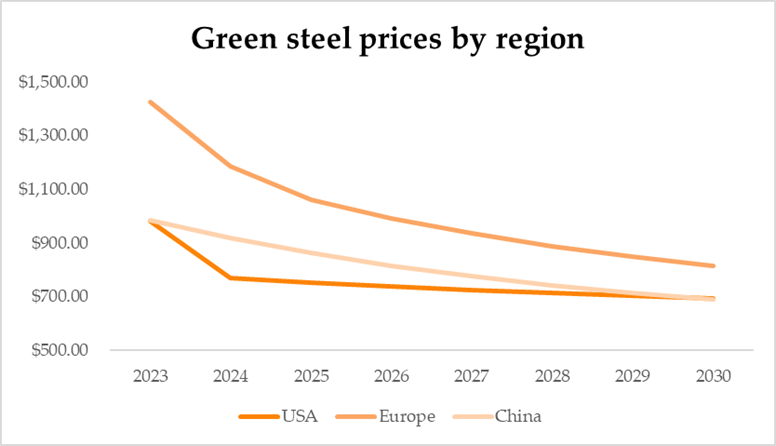

They predict the rapid electrification of the global steel industry mid next decade — see the chart above. The industry will be inconvenient to decarbonise, but not impossible thanks to green hydrogen.

Input costs of iron ore, coal, natural gas, hydrogen, and electricity dictate how cheap or expensive steel will be.

There are two main primary production methods for steel: “the BF/BOF (blast furnace/basic oxygen furnace pathway) and the DRI/EAF (direct reduction of iron/electric arc furnace) pathway.” The BF/BOF pathway “represents 69% of global output and it requires iron ore as a raw material which is reduced in a blast furnace at 1,000 degrees Celsius with the help of coking coal in the absence of air. The oxygen removed is reacting with the carbon and producing CO2 emissions. Liquid iron is the main product of a blast furnace which is then moved to a basic oxygen furnace where oxygen is blown through the liquid in order to lower its carbon content and finally produce liquid crude steel. Chromium and nickel are among many elements and compounds that can be added to crude steel — forming stainless steel in this case — to produce one of the 2,500 different grades of steel in use today.”

1.9 tons of CO2 emissions are produced per ton of steel.

In the DRI/EAF procedures, “the first stage is the direct reduction of iron which takes iron ore and reduces it with hydrogen or natural gas and carbon dioxide at 800 degrees Celsius in order to create sponge iron. This is then melted in an electric arc furnace to create liquid crude steel.”

Producing one ton of steel via the DRI/EAF pathway requires between 3.5 MWh and 5.0 MWh of total energy input. Currently, this releases 1.15 tons of CO2 per ton of steel produced. There is much greater potential to decarbonize the DRI pathway than the BF/BOF pathway by using only green hydrogen in the reduction process and renewable energy to run the electric arc furnace. It might be possible to completely eliminate emissions throughout.

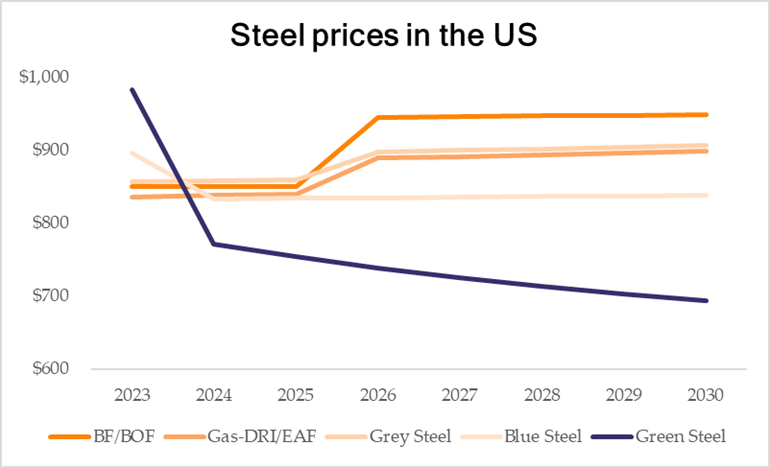

The steel would then be designated by colour, grey steel produced using hydrogen created from methane, green steel produced by using hydrogen created from electrolysis of water and powered by renewable energy.

Steel produced from the recycling of scrap is labelled secondary steel production. At the moment, this represents only 20% of production. ReThink Energy expects this percentage to grow to around 35% by 2050, as more steel is recycled.

Although iron ore is mined in about 50 countries, the bulk comes from Australia and Brazil. Shipping costs must also be factored into the cost of producing steel both for iron ore and for coal. The price of natural gas will dictate the price of steel in the short term, the price of hydrogen will do so in the long term.

With the ongoing energy crisis, the price of coal has soared. This seems to have narrowed the gap between the cost of green steel and traditional steel, bringing the time that green steel undercuts its traditional rival a bit closer.

As Europe’s carbon border tax is introduced in 2026, will steel users have to pay a premium for green steel? This may be worth it to avoid the tax and be able to say to discerning consumers that their products are sustainably produced.

ReThink Energy predicts that green steel will be the cheapest form of steel produced in the USA within the next 12 months. Hydrogen is already produced reasonably cheaply in the US. Add to that the subsidy announced in the IRA, and if there is a supply of green hydrogen, green steel will be the cheapest steel. “Currently the cheapest way of producing steel in North America is through the Gas-DRI/EAF process — $836.15.”

The European Union will likely look to North America for its ongoing steel imports. Russia was the second largest exporter of steel to the EU but is in the process of ending its commercial relationship. Other imports will continue to come from Asia and other non-EU countries. The carbon tax will come into play, moving suppliers to seek greener options for steelmaking.

ReThink Energy concludes: “The road seems to be set for green steel to not only become an attractive business proposition but to also severely undercut any rival manufacturing methods and completely transform the American share of the steel industry.”

The EU is a little more complicated. Because it has to import all raw materials, steelmaking in the EU tends to be more expensive than in the US. Plus: “The European Carbon Trading Scheme has allowed the steel industry to keep receiving free CO2 pollution permits at least until 2032, and thus European countries will be immune to the same type of tax that outside exporters will have to pay for selling to the EU.”

In the EU, green hydrogen sells for $10/kg mostly because it has to be imported from Australia. Once it can be produced in quantity closer to home, the price will fall. The EU is also considering a green hydrogen subsidy in response to the IRA. This could start affecting the industry as soon as the end of next year, at which point green steel will undercut all of the other processes except traditional BF/BOF.

“As green hydrogen will continue to become cheaper and cheaper, we predict that green steel will undercut the current cheapest BF/BOF method in 2028 when a ton of the sustainable product will cost $889.24.”

China produces 50% of global steel, and since it uses the majority of what it produces, there are no external pressures to decarbonize the industry. China’s net zero target of 2060 gives it plenty of wriggle room. RE predicts that by 2026, green steel will become cheaper than most other methods of steel production, aided by a growth in the local green hydrogen industry.

As for the economics, Europe is leading the investment race, with private investment supplemented by government grants. China and South Korea are the leaders in Asia, with green steel deals being done with German carmakers. The US only has a few R&D projects underway, whereas Canada has two full-scale green steel projects.

Here in Australia, Fortescue Metals and others are exploring production methods. There are also projects in Africa, Chile, and Brazil.

RE expects that green steel prices will fall due to a decrease in the costs of green hydrogen aided by subsidies and carbon taxes. That being the case, premium prices for green steel won’t last for long. As more and more pilot projects are put in place, it will have a positive effect on dropping the price even more. The market will move towards real green steel.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy