1st Quarter Dutch BEV Sales Above Expectations, 25.5% Market Share

Support CleanTechnica's work through a Substack subscription, on Patreon, or on Stripe. Help us produce all of the high-quality, original content we publish week after week despite the challenges of content-scraping AI, antisocial media, inflation, and other hurdles.

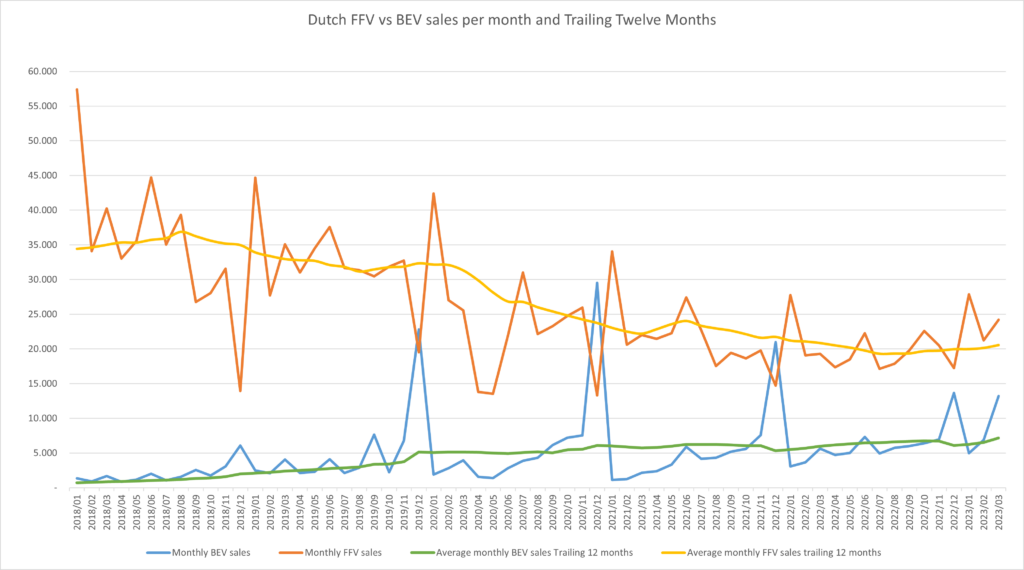

Traditionally, Dutch BEV sales show a spike in the last quarter of the year. This is followed by a trench in the first quarter. Sales of fossil fuel vehicles follow the opposite trend. Low sales in the last quarter followed by high sales in the first quarter.

The current quarter being the best quarter (rather than the last quarter being the best) is surely an indication of how well the market is growing. Fully electric cars reached a market share of 25.5% over the quarter, nicely divided into 15%, 25%, and 35% in the respective first three months of the year.

Previously, the high market share of BEVs just before year’s end was in part made possible by the fossil fuel market delaying deliveries until the new year. When one is high and the other is low, you get a brilliant ratio. But in the first quarter, fossil fuel vehicle (FFV) sales were very high, and still BEV market share was extremely high.

When looking historically, ignoring the COVID-19 years 2020 and 2021, we see growth of 119% in Q1 2019 versus Q1 2018, 44% in Q1 2022 vs. Q1 2019, and 103% in Q1 2023 vs. Q1 2022. High growth percentages are harder when market share is bigger, making the Q1 2023 growth awesome in my eyes.

By the way, this was the first Q1 in 5 years that FFV registrations grew. And it is likely only because better supply enabled carmakers to deliver orders from their large backlogs, not because of an increase in demand.

The year 2018 was the last good year for the fossil fuel car market. After that year, the decline started. Only in the last quarter of 2022 and the first quarter of this year did FFV registrations recover a bit. While the absolute numbers for fossil fuel vehicles were rising for the first time in five years in Q1, the market share of BEVs rose from 15.8% in Q1 2022 to 25.5% in Q1 2023. If anybody considers this quarter a win for the FFV portion of the market, it was a Pyrrhic victory.

Here are some nice graphs to illustrate what is happening in the market:

And now the numbers

The number of BEVs registered in Q1 was 25,101 (4,974 + 6,892 + 13,225), for 25.5% market share (15% in January, 25% in February, 35% in March). FFV registrations were 73,324 (27,871 + 21,236 + 24,217), giving a total of 98,425 vehicle registrations (32,845 + 28,128 + 37,452).

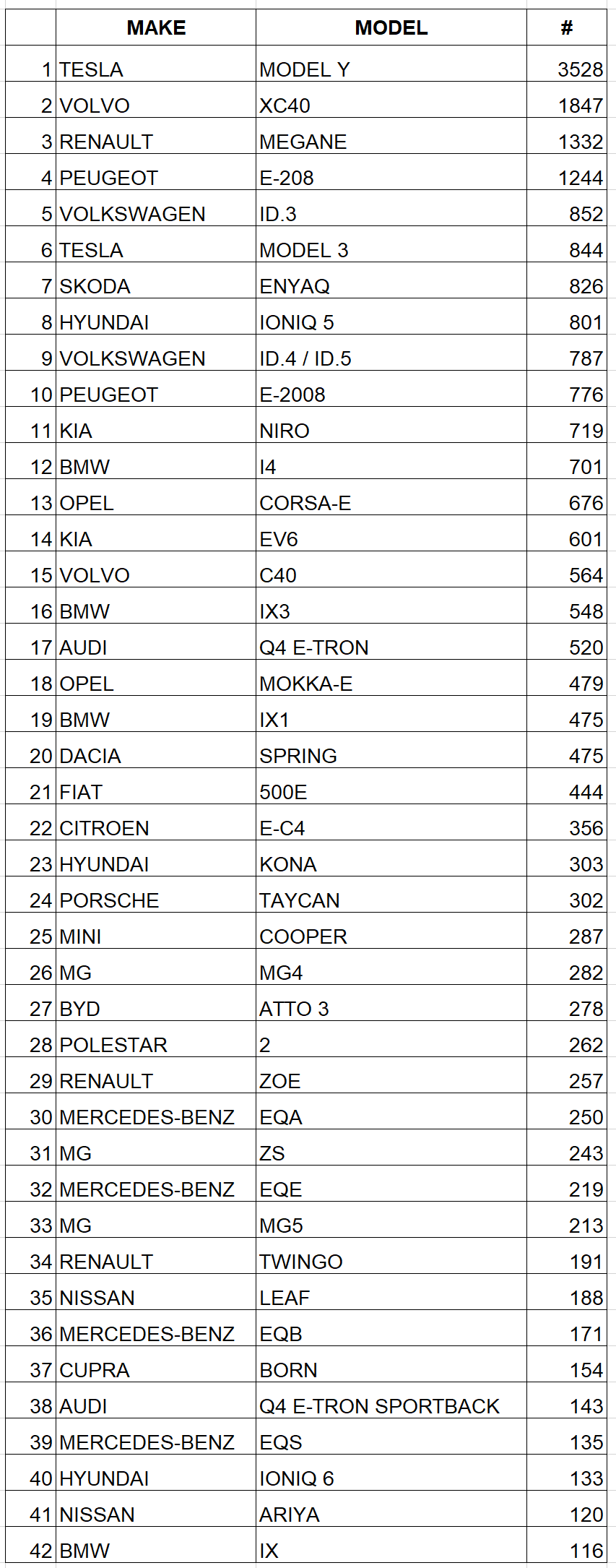

Looking at the best selling models, there are 42 models that reached over 100 vehicle registrations each. For those of you interested in the models that did not make my cut, the source of my numbers is here.

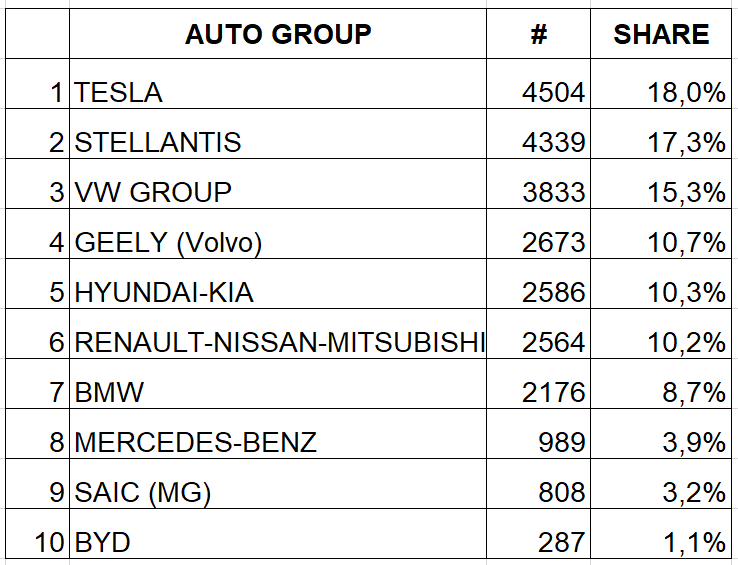

The first thing that caches the eye is the return of Tesla at the top of the list. In December 2022, the Model Y appeared out of nowhere and not only took the #1 position in the last month of the year, but with such a wide margin that it also became #1 for the whole last quarter. Now Tesla is the #1 automotive group! It’s even beating Stellantis and Volkswagen Group, the two conglomerates that normally decide who is #1 and #2. What is most exceptional about the Tesla Model Y: it was #1 in all three months, not just in the last month of the quarter, as was previously always the case.

I recently reviewed the models in second and third place (the Volvo C40, the coupe version of the XC40), and the rest in the top 10 is at least nearly two years old. There are clearly no exciting new models from well established brands, and the models from unknown brands — like BYD, NIO, Cupra, and even MG — need more time to reach a wider public.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy