Norway’s Vehicle Fleet Transitions To Electric — How Long Will It Take?

Support CleanTechnica's work through a Substack subscription or on Stripe.

As of the end of Q2 2022, Norway’s passenger vehicle fleet comprised 24.4% plugin vehicles (18% full electrics), up from 19.3% (13.6%) year on year. What is the trajectory of Norway’s vehicle fleet, and how long will it be before most car journeys are made on electricity?

This time a year ago, the plugin share of the fleet was 19.3% (13.6% BEV), so their share grew by 5.1% over the past 12 months. This comes as a result of 88.9% share of new sales over this 12 month period being plugin, and despite the fact that new sales have seen lower absolute volumes recently (H1 2022 was over 20% down in volume YoY).

These results suggests that, other things being equal, once plugins are regularly at or above 95% share of new sales, and the auto sales market recovers to normal volumes, a plugin fleet annual growth of around 6% should result.

A Longer View

To understand the relationship between evolving fleet composition, the relative proportion of Norway’s passenger vehicle travel made by electric power versus fossil fuel power, and the reduction in volume of fossil fuels used, we need to step back a bit and consider a few factors.

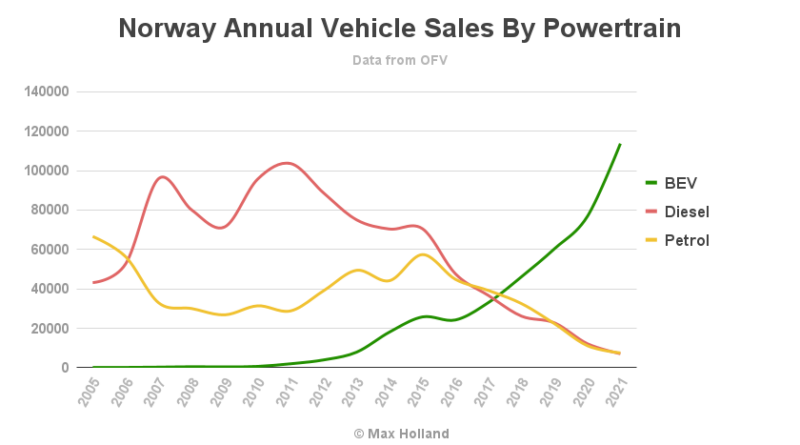

First let’s understand that the different powertrains in Norway’s passenger vehicle fleet have very different age profiles. To see this, look at this longer term (and simplified) fleet annual time series from 2005 to the end of 2021. This one is based on long term data from the SSB, rather than from the OFV (geek note — their data methodology differs). I’ve removed the thin slices of HEV and PHEV to focus on the 3 main powertrains:

The average age of vehicles retiring from Norway’s passenger vehicle fleet is currently 17 to 18 years old (they may be scrapped, or exported as used vehicles). The overall fleet profile therefore results mostly from the pattern of new vehicle sales over the past 20 years or so, and cannot quickly transition based only on what has been happening in the last handful of years.

We can clearly see from the above graph that petrol combustion vehicles (in yellow) were very dominant in Norway’s passenger fleet coming out of the late 1990s and through the early 2000s, but that diesel started to take increasing share away from petrol, especially from 2006-2007 onwards.

This was simply due to more new diesel vehicles joining the fleet than new petrol vehicles — obviously via higher new sales and registrations (graph below). But notice that — whilst diesels strongly dominated new sales from 2006 on — it wasn’t until 2016 that diesels actually overtook petrol vehicles as the dominant powertrain in the overall fleet. Fleet transitions take time.

Here’s a visualization of that period of diesel sales dominance, lasting from roughly 2006 to 2016:

Ironically, just as diesel was finally outweighing petrol in the overall fleet, diesels sales were rapidly declining back to petrol sales levels, and both were then fading fast anyway, due to BEVs starting their take over of the new car market.

Since around 2015, both combustion powertrains’ sales have been in steep decline as plugins and especially BEV options have multiplied and become ever more affordable, capable, and available. Here at CleanTechnica we’ve been reporting on these evolving trends every month for key markets, for many years.

Aging Cars Get Driven Less

What does this view of the recent history of powertrain sales and fleet share tell us? BEVs are now taking the vast majority of new sales (around 80% and growing), and are thus slowly but steadily growing in fleet share as combustion peers fail to get replaced by new combustion additions.

Importantly, the vast majority BEVs in the fleet are very young vehicles, compared to their combustion counterparts.

As of the start of 2022 BEVs represented some 16% of Norway’s overall fleet, with 455,271 passenger BEVs on Norway’s roads. But note that some 80% of those BEVs (over 330,000 of them) are 2017 vintage or newer. Put differently, only 20% are from 2016 or older.

The fleet of diesel and petrol vehicles, together over 70% of the total fleet, are on average much older vehicles. Of the 1,166,789 diesel passenger vehicles in the fleet at the start of 2022, less than 10% are vehicles sold in 2017 or later, so over 90% are more than 5 years old.

Likewise, in the petrol fleet of 911,502 vehicles (start of 2022), only around 12% are from 2017 or newer — 88% are more than 5 years old.

What’s the significance of this skewed aged profile of the combustion vehicle fleet? Older vehicles on average get driven less than newer vehicles.

As a result, the “annual vehicle km traveled” (and therefore the energy used /emissions produced) by old vehicles is less, other things being equal.

On a whole-of-fleet level, the proportion of total passenger vehicle km traveled is increasingly weighted towards the much younger BEVs, and away from the older combustion vehicles. More so than a cursory glance at the simple fleet powertrain share might suggest.

Obviously the idea that older vehicles get driven relatively less makes intuitive sense, but let’s confirm that the hard data from Norway supports this, starting with diesels:

Note how the reduction in annual km traveled for diesel passenger vehicles as they age is fairly predictable and linear. We can also see that the average (“All Ages”) diesel vehicle in the fleet drove 12,665 km in 2021, down from a peak of over 19,000 in 2007 (when most of the diesel fleet was relatively new and heavily used).

Petrol vehicles in Norway get driven less annual km than diesels. This is partly because, due to petrol ICEs being somewhat cheaper to produce than diesel ICEs (which operate at much higher pressure), petrol power is more common in the affordable compact, and subcompact, urban vehicle classes. Obviously these small vehicle classes tend to cover less annual KM than the average diesel vehicle, which is larger and more expensive. The fact that diesels have better fuel cost per km than petrol vehicles is also a factor differentiating their respective average annual km traveled.

The average petrol vehicle in the fleet traveled 8,117 km per year in 2021, down from over 12,000 km in 2007:

BEVs are a different story, because — at commercial scale — they are a new and rapidly evolving technology, with high growth rates. Notice that prior to June 2013, the few BEV models available in any volume (Nissan Leaf, Mitsubishi i-MiEV triplets, a few Think! City, and Buddy EVs) were 1st generation, lowish range vehicles, most suitable for urban and regional journeys. Only 30-something Tesla roadsters were delivered to Norway in 2012, versus over 4,000 Leafs-and-triplets.

DC charging infrastructure was also in its infancy back before 2013. These factors resulted in annual average distance traveled for BEVs in the range of 6,500 to 7,500 km, even when these vehicles were new.

However, after the Tesla Model S arrived in Norway (from June 2013), and DC fast chargers for all BEVs started to spread rapidly, the average BEV annual km traveled quickly started climbing, to almost 12,000 km by 2016.

With more and more chargers, and long-range-and-affordable BEVs available from 2017 (Chevy Bolt/Ampera-e), later Hyundai Kona and Kia Niro, and loads of Tesla Model 3s from February 2019, the annual km traveled has continued to increase.

In fact, as of the end of full year 2021, BEVs, averaging 12,772 km per year, had overtaken diesels’ 12,665 km:

With fuel cost savings being greatest for those with the highest annual driving distances, and BEVs now fully capable of regular long-distance journeys (especially thanks to Norway’s great charging infrastructure), the average km traveled of BEVs will likely increase for several more years.

Total Passenger Vehicle KM Traveled by Powertrain

Norway’s statistics bureau (SSB) also gathers data on the combined total annual km driven by the entire membership of a given powertrain. Since we know that the combustion powertrain fleets are highly skewed towards much older vehicles that tend to drive less, we should expect to see their combined total km driven declining even faster than their proportion of the fleet is declining.

Let’s first isolate the SSB’s passenger vehicle fleet data as individual powertrain volume curves:

Now, let’s check if the combined total annual km driven by combustion powertrains is declining even faster:

The visual impression is clear, both petrol and diesel fleets’ total km driven is declining at an even faster rate than their actual fleet size is declining.

From their 2008 unit volume (almost 1.6M), until the end of 2021 (just under 0.9M), the number of petrol vehicles in the fleet has decreased by 44.3%. However, their combined km driven has declined at a much steeper rate, by 60.7%.

For diesels, from their peak fleet numbers in 2017, their ranks have decreased by 6.3% to the end of 2021, but their combined KM driven have decreased by 18.1%.

In both cases, the fleet of combustion vehicles have seen a disproportionate decease in total km traveled over recent years, as the fleet ages.

Fuel Use Fade Out Rate?

As Norway’s passenger vehicle fleet steadily continues its transition from combustion to electric, and km traveled by combustion decreases, the fuel use of Norway’s passenger vehicle transport is obviously reducing.

Since petrol and diesel fuel use by passenger vehicles should closely correlate with the fleet’s km traveled, we can look for this relationship in the data.

Diesel fuel is heavily used by many other types of road vehicles than just passenger vehicles, (and used extensively in the large marine sector, and others also) so the correlation is hard to detect in the diesel fuel sales data.

For petrol fuel — for which sales tends to be very closely tied to its use in petrol passenger vehicles — the decline with the diminishing annual KM driven might be clearer.

Here’s the chart of petrol fuel deliveries over time, a derivative of the above chart. Petrol deliveries are added on, scaled and anchored to match the 2010 point of reference (2010 is the first date available for the fuel data set):

From 2010 to 2021, total petrol fleet km driven decreased by 55.3% (17,907 million km, down to 7,995 million km). Petrol fuel sales over the same period declined by just 40.3% (1625 down to 970 million liters). Here’s the link to the data, including sources for anyone who wants to dig further.

Overall, obviously the volume of petrol fuel deliveries is declining decently over time, just not quite keeping pace with the decline in fleet km traveled.

Is the petrol delivery volume being propped up by increasing vehicle size (the rise of SUVs), colder-than-normal winters, higher legal driving speeds, or some other variables? I don’t know. I would appreciate data geeks, especially those familiar with factors in Norway’s automotive landscape, jumping in to the comments and helping us understand why petrol (“motor gasoline”) fuel deliveries are not more closely matched over time with petrol vehicle km traveled.

I’ll update the article here if our community has some good insights. Update — Several commenters have suggested that fuel use may be propped up by the decrease in efficiency of the ICE powertrain as vehicles age, which could certainly be a key influence. We’ve also had the reminder that all combustion vehicles (including petrols) saw rising power outputs from the late 1990s into the 2010s, and larger vehicle sizes which — despite manufacturer claims on unrealistic consumption tests — probably consume more fuel per km than the older, smaller, less powerful vehicles which have recently retired. Please jump in the comments below if you have an other insights into why petrol consumption is not quite decreasing as the same rate as total km traveled.

Biofuel side note — petrol fuel deliveries above includes the legislated fraction of bio-petrol (“bioetanol”) within the mix. This fraction stood at around 6% at the end of 2020 and is steadily increasing. Biodiesel was over 16% fraction of auto diesel in 2020 (latest dates I have sources for). A proportion of 12.5% to 15.5% biofuel is mixed in to road traffic fuels in 2022, and will rise over time. There is also effort to increase the share of “advanced” biofuels that don’t compete with food production, nor involve deforestation.

Overall, we can conclude that the passenger vehicle fleet is steadily turning over from combustion power to plugin power, the share of km traveled is turning over even faster, and passenger vehicle fuel use is declining almost (but not quite) proportionally to km traveled. Unfortunately, we only get the SSB’s “km traveled” data annually, so we will have to wait until next year to check up on the evolving correlation between these 3 key variables.

Outlook

We get quarterly updates on Norway’s fleet composition from the OFV, via elbil.no., the latest of which appeared a few weeks ago. This time, rather than communicating the update as a short portion of Norway’s monthly EV report, I thought I would take readers through a deeper dive into some of the key variables involved.

As we saw at the top of this article, at the end of June 2022, the fleet comprised just over 18.0% BEVs and 6.4% PHEVs, for a total of 24.4% plugins. Over the past 12 months, plugins were 88.9% of new sales, and this (along with grey imports and retirement rates) mapped to fleet share of plugins growing by 5.1%, from 19.3% to 24.4%.

This 5.1% change happened even amidst H1’s auto sales volumes dropping by 20% YoY. If the new vehicle market stabilizes at seasonally average volumes, and plugin share climbs to 95% of new sales and beyond, we can expect the plugin fleet to grow by around 6% per year in the near future.

With increasing fuel prices across Europe, and BEVs getting steadily cheaper, there’s a decent chance that folks driving older combustion vehicles will also begin to bring forward their retirement from the customary 17–18 years age. To the extent that this happens, perhaps accompanied by greater imports of lightly used BEVs from neighbouring countries, the fleet plugin share may grow more quickly, perhaps by 7% annually in the coming years.

This means that, from mid-2022’s 24.4% share of the fleet, by the end of 2025 we could be looking at from 42% plugins (if 5% growth annually) to 49% plugins (if 7%). By the end of 2030, 67% plugins (if 5%) to 84% (if 7%). I will take a cautious figure of 70% as the lower bound.

Since plugless HEVs account for 5% fleet share today, and 4.4% of new sales over the past 12 months, and are newer than the average combustion vehicle, HEVs should still hold 3% to 5% (say 4%) of the fleet by 2030. These are plugless and get all their energy from combustion fuels, but are slightly more fuel efficient than the average combustion-only vehicle.

This means that only around 26% of the fleet will be combustion-only by the end of 2030, and 30% once we include plugless HEVs.

More than 80% of the plugless fleet will be over 10 years old and — as we saw in the graphs above — being driven a lot less than they used to be.

In 2010, 99.5% of the fleet were plugless vehicles, each traveling over 13,000 km per year on average. By the end of 2030, the roughly 30% of the fleet that remains plugless will be traveling likely 6,000 to 7,000 km per year on average, around half their 2010 distances.

Overall then, plugless km traveled will therefore be roughly 15% of what it was in 2010, before the EV transition had really started. Fuel demand for these km should be in the range of 15% to 20% of what is was in 2010.

However, recall that biofuels are already 12.5% to 15.5% of the road transport fuel volume delivered today. If biofuel volume just keeps stable (or modestly increasing) as overall demand for combustion fuels declines to 15% to 20% of previous levels, the fossil fuel proportion of this residual road fuel demand could be just half (or less) by the end of 2030. This would then represent perhaps just 7.5% to 10% of the 2010 fossil fuel volume, for passenger vehicles.

There are plenty of other categories of use of fossil fuels in Norway, but passenger vehicles are the largest, and the other categories (especially commercial road transport categories) are also now quickly turning to electrification.

What are your thoughts on Norway’s passenger fleet transition and overall decline in road transport fuel demand? Please join in the discussion below.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy