SPACs Are A Problem In North American Cleantech Investing

Support CleanTechnica's work through a Substack subscription, on Patreon, or on Stripe. Help us produce all of the high-quality, original content we publish week after week despite the challenges of content-scraping AI, antisocial media, inflation, and other hurdles.

Over the past year I’ve spent a considerable amount of time scratching my head at the peak market valuations of electric air taxis like Joby, Archer and Lilium, silly gravity storage ideas like Energy Vault, and technologies with no market to speak of, like Heliogen. One clear thing emerged from the bad ideas that received far too much money: most of them were funded by SPACs.

SPAC stands for special purpose acquisition company. They are also known as blank check companies. Basically, a bunch of financial types get together, put together a public company with shares costing typically around $10, sell a bunch of the shares, and keep a bunch for themselves. There’s nothing except money and shares in the companies — they are simply shells. Then they go hunting for a startup to do a reverse takeover of. Typically they’ve told their investors the type of market they are going after, but that’s about it.

The ‘benefit’ of SPACs is that they are already public companies, already have trading shares, and have already filed their prospectuses with the SEC, all legal, above board, and compliant. As a result, when they acquire a startup, none of the normal due diligence has to apply, and none of the rules about what is permissible to say apply. They can make up complete and utter nonsense, promote the acquisition heavily, pump up the value of the stocks into the stratosphere, then make their exit with a very large paycheck in hand for themselves.

And in a lot of cases, not much of a paycheck for the startup compared to the billions floating around, and a very rapid fall back to earth for the stock, with massive losses for retail and insufficiently cautious professional investors.

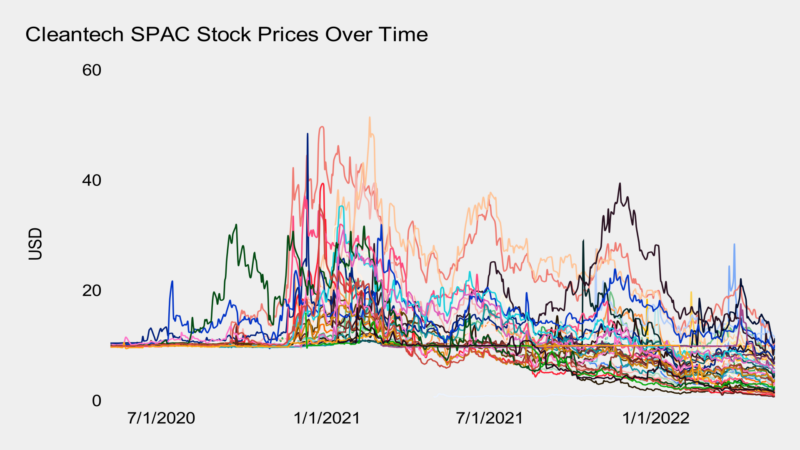

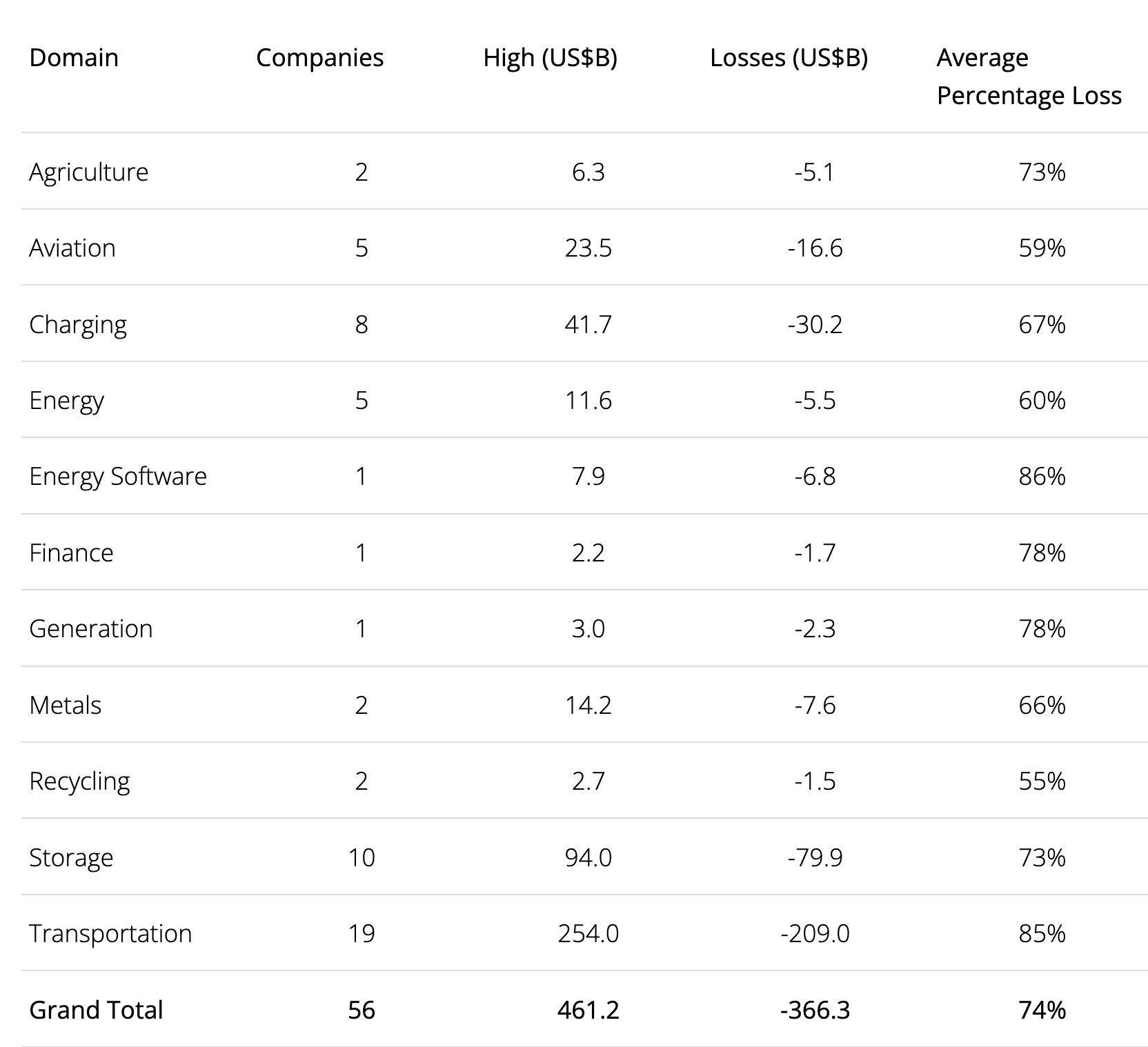

At least 56 of those SPACs were in the cleantech space. As the first chart showed, most had a period of high valuation around the point of acquisition, and then rapidly lost value.

Of course, investors aren’t happy, and class-action ambulance-chasing attorneys are salivating. 34 of these companies have investor class action suits established and in progress, many of them have 3-5 separate suits that they are dealing with, and a total of 85 separate legal actions are under way or completed. The 34 companies are, of course, the ones with the highest market caps at one point, with an average peak valuation over $11 billion, while the average for the not-currently-being-sued companies is around $3.6 billion. Some of them are aimed at the SPAC founders, as they typically are the ones who walked away with the most money and hence are the richest targets, but others are aimed at the now publicly traded companies, as some of them have money too.

Not as much money as you might think, though. One firm whose peak market valuation was in the billions was left with only $235 million, and that’s not unusual. The SPAC founders realized that they were in a buyers’ market and made the terms that they presented to desperate and/or greedy startups onerous, with the large majority of all capital raised flowing to the SPAC founders. Half a dozen proposed and publicized SPAC deals in the cleantech space have fallen through as startups walked away from deals where they would receive a small minority of raised funds.

As a note to people hoping to sell things to these companies, or hoping that they will acquire your startup themselves as your exit, they typically don’t have anywhere as much money as you think that they do, and clearly a buyout in their stock isn’t a great idea for you.

But let’s make something clear. Many of these firms are decent. I happen to have stumbled backward into my assessment of cleantech SPACs due to firms with nothing of value to offer that were clearly overly hyped. If investors had asked my opinion before putting their money into these firms, I likely would have provided more value due to timeliness, but alas by the time I heard about them the hype and stock price inflation had typically already occurred. Thankfully, several investment firms globally are starting to seek my opinion about where they should be spending their money before they spend it, not cringing afterward as my assessments cross their screens.

Proterra, for example, is working hard to deliver electric buses, a key value segment. I think that they have challenges in terms of the conditions for success, but I wish them well. The EV charging firms also have clear value propositions, and most of them even had actual revenue, something which undoubtedly contributed to them having fewer lawsuits against them than some other segments. Many of these firms have now been saddled with an external belief that they are worth billions, an internal reality that there is no world in which they can be worth that, and often the stench of inflated claims by people who they had little control or even influence over. Most cleantech startups are trying to make the world a better place, and the aftermath of a SPAC bubble and burst is going to leave them with very weird expectations, ones that they can’t possible meet.

Some of them, of course, have worse legal problems than class-action lawsuits on behalf of investors who were presented with incomplete or actively inaccurate information. Nikola is on the list, and paid a fine of $125 million to the SEC for its excesses. Nikola’s founder, former natural gas salesman Trevor Milton, is out on $100 million bail while his two fraud indictments wind their way through the courts. That said, the SPAC shielding of companies from SEC compliance concerns seems to have worked so far. There are remarkably few SEC actions against these firms, but there are many indicators that SPACs in general are going to be in for much tougher compliance and due diligence requirements.

The SEC exists in part, after all, to protect investors from penny stock pump and dumpers and the like, hence the stringent requirements on IPOs that came into being after the dot com gold rush, and the crackdown on cryptocurrency initial coin offerings (ICOs) in the past few years. Lots of people gave lots of money to strangers based on wild promises and greed, and lots of people lost that money.

This is almost entirely a US SEC problem. These firms are public almost entirely on US exchanges, the NYSE and NASDAQ, with only one firm not on those exchanges. The firms are mostly US firms as well, with a scattering of firms from other parts of the world. As one observer — whose name I didn’t keep track of, so apologies for not citing you if you read this — pointed out, this is an American problem because the rest of the world is seeing very significant governmental investment in cleantech and cleantech deployment, while the US is lagging badly. Major governmental grants and low-interest loan programs exist in most developed countries for the transformation, but the US has been mostly missing in action. The DOE keeps trying to boost perovskites and concentrating solar power, as a key indicator that the wrong people are holding the purse strings. That’s starting to change somewhat with the Biden Administrations’ efforts, but they are small and late compared to other countries.

There is one individual to call out in this, Bill Gross. That’s the former dot com guy, not the hedge fund Bill Gross, by the way. He’s still wealthy, having made a series of reasonably successful exits in the 1990s and early 2000s. He’s behind two of the 56 firms on this list, Heliogen and Energy Vault, both of which I have written scathingly about. He’s also behind Carbon Capture, a direct air capture startup which I haven’t written about specifically, but have certainly made it clear through multiple assessment and publications that the entire space is a deeply flawed idea of merit only for greenwashing for oil and gas firms. Gross really needs new climate solution advisors. The firms he’s creating and often gathering massive funding for are deeply flawed. I’m pretty sure his heart is in the right place, but his actions aren’t helping move the needle.

The takeaway here shouldn’t be that cleantech firms are high risk and over valued. The takeaway is that unscrupulous people found a way to fleece a lot of investors of a lot of money via SPACs, the latest in a line of investment structures intended to dodge oversight. Caveat emptor.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy