Aviation Demand Forecasting Expert Challenges 2100 Aviation Refueling Scenario

Support CleanTechnica's work through a Substack subscription, on Patreon, or on Stripe. Help us produce all of the high-quality, original content we publish week after week despite the challenges of content-scraping AI, antisocial media, inflation, and other hurdles.

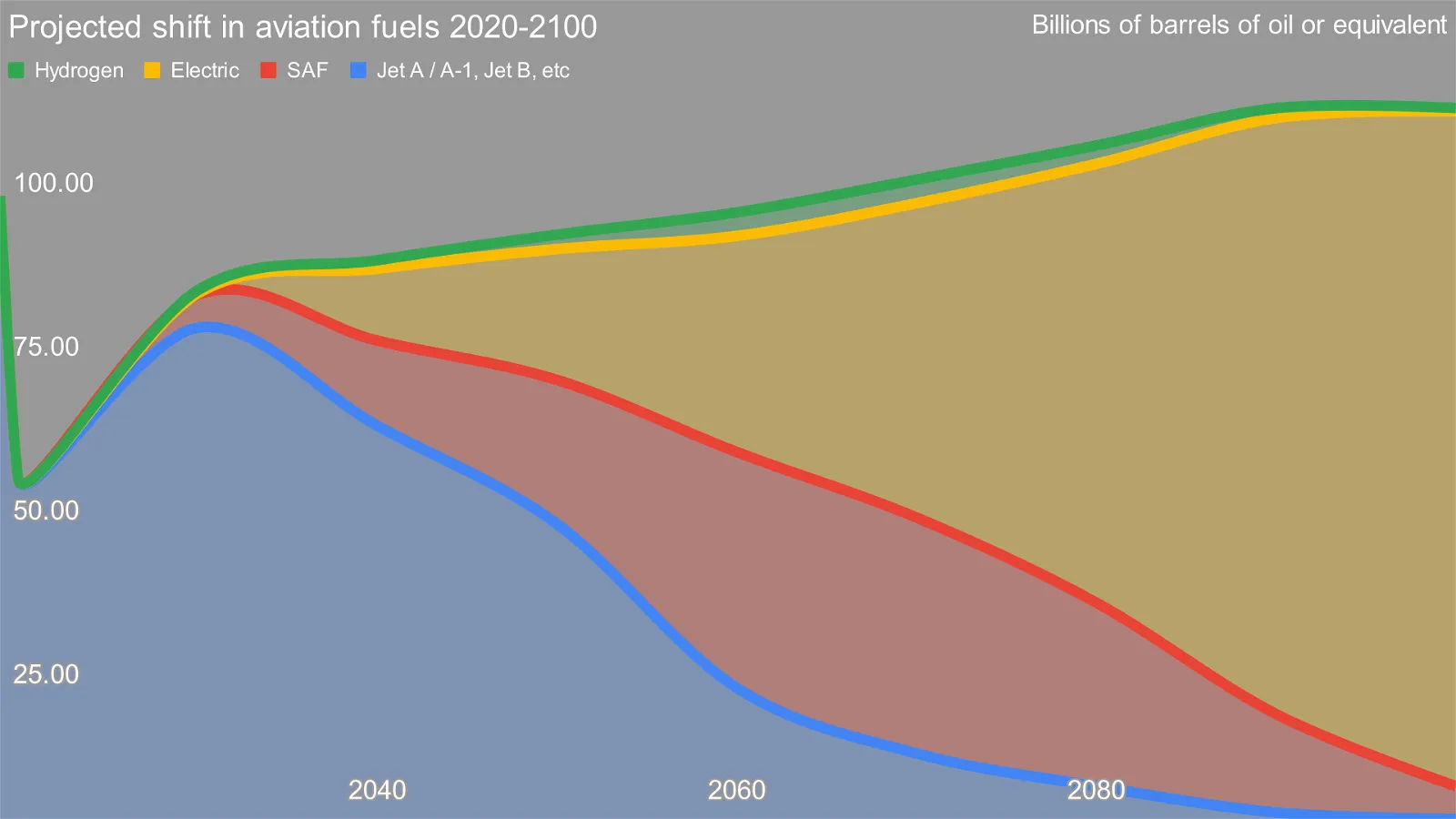

In late 2021, I published a notional decade-by-decade scenario of aviation refueling demand through 2100. It was based on multiple intersecting trends, disruptions, and technological changes. I asserted that COVID-19 was a discontinuity that fundamentally shifted aviation passenger demand, and further, that other forces would suppress demand. There would be some efficiency gains of more aerodynamic airframes and greater spread of more efficient turbofans — not initially thought of, but obvious in retrospect — that would lead to flattish aviation energy demand as the sector changed fuels. Huge error bars, and as always, I invited informed parties to help improve the thinking.

Today I had the most substantive discussion of challenges to the projection. I spent close to two hours with Wilma Suen, PhD in strategic alliances and most recently the global Vice President of Portfolio Strategy & Forecasting for GE’s airplane leasing business, until very recently the largest such organization in the world. She and her timezone-distributed team spent their days analyzing the best data that a multibillion dollar organization could buy to project flights per person per year for every material country in the world for 5, 10, and 20 years, with decreasing reliability with each increase in duration of course.

Suen and I know each other because of Volo Earth Ventures and ELECTRON Aviation. Volo is a new cleantech venture capital fund based in the US with principals with strong backgrounds with the Rocky Mountain Institute, academia, and cleantech business ventures. ELECTRON is an electric airplane business startup out of the Netherlands, whose Advisory Board I recently joined. I had introduced the founders of ELECTRON, Josef Mouris and Marc-Henry de Jong to Volo, and Volo had subsequently introduced Suen to us.

Suen and I met for coffee and a stroll along Vancouver’s Seawall this morning, including past Barge Chilling Beach where a massive, wood chip barge was blown ashore a few months ago because of a king tide and strong offshore winds. One of the subjects of conversation was her challenges to my assertion of aviation refueling. It broke down into multiple parts, and I’ll try to do justice to the arguments and counter arguments.

First off, Suen is an insider in the world of aviation, and I’m an outsider, although that’s changing. My position is not aligned with the major firms and their lobbying group, the International Air Transport Association (IATA), but that doesn’t mean that they are wrong or I am right. What it does mean is that their projections of significant growth in aviation are best understood as a potentially more rosy projection that makes their stakeholders and shareholders feel comfortable that they are part of a growth industry. My projections from outside of the industry do not have a requirement to make aviation shareholders and influencers happy, so perhaps are more clear-eyed as a result. Or I am simply less informed. I consider many market projections to be induction from priors without considering discontinuities and am comfortable with mine as a result. Suen in no way dismissed my projections due to my outsider status and welcomed them as an interesting challenge to her assumptions, but we laughed about them being likely unwelcome at industry conferences. Certainly current passenger volumes remain far below the 2019 peak.

More nuanced was the question of demographic changes by region and country, along with alternatives. The socioeconomic cutoff Suen used for a likelihood of flights per person per year is roughly $5,000 in per capita GDP, a general rule of thumb that is commonly used but doesn’t have strong academic support. Below that, and too few people in a country flew per year to be worth tracking. Above that, and interesting differences started appearing. With increases in average GDP, flights increase, unsurprisingly. A more granular, country-by-country projection isn’t something I would attempt, but it would lead to both sharper increases in some countries and decreases in others.

After the socioeconomic cutoff came average age and population growth. Europe is considered by Suen to be a flat market as the populace is not growing, and is aging and affluent. All the people who wish to fly already do so, and flygskam is sufficiently powerful to potentially reduce flights. And Europe has alternatives. It’s relatively small and dense for its population of 750 million, it’s well connected with roads for electric cars, and more importantly it’s well connected with trains, including 19,000 kilometers of high-speed, electrified rail. Europe is not likely to be a growth market for aviation demand, but that demand will shift around.

Next comes major Asian countries, which have variances of their own. China is increasing in affluence rapidly, is a large country, and has significant trade connections with the rest of the world. But it has also built 38,000 km of high-speed electrified rail since 2007, giving its citizens a fast, safe, convenient mode of transportation between major areas that is competitive in price and travel time with aviation. By contrast, India has a tradition of passenger rail, but compared to China, rail is slow, crowded, and antiquated. India also has a populace which is increasing in affluence, but doesn’t have the alternatives China does.

Then comes relatively inequity. As Suen pointed out, India’s inequity is high, so currently only the top 10% of the populace is going to have the income necessary to fly. However, as India has over a billion people, that’s still over a 100 million people with an increasing propensity to fly regularly.

Geography plays a part as well. There are two types of nations for which domestic travel is deeply challenging. The first are the Chiles and Malaysias of the world — long, thin countries. Major population centers are usually dotted along the country and travel between them has only one major route. The Pacific Northwest of North America fits into this differently, as the major highway to the west of the geographical barrier of Rockies that connects Vancouver, BC, to Seattle, San Francisco, Los Angeles, and San Diego is singular, and has multiple chokepoints along its length, many of which I’ve experienced over the years. Aviation that hops over traffic and curves for these geographically constrained regions is likely a growth market for the increasingly affluent. Second are the island nations. I’ve written about the challenges of archipelago countries such as Indonesia in the past — side note: paragliding the southern cliffs of Bali was a peak life experience — and know that its 6,000 populated islands of 17,500 in the country make many things including travel challenging.

Then there is slowing population increase. As I pointed out in the original assessment, global population growth is slowing. The work of Gro Brundtland’s UN commission that led to Toward a Sustainable Future in the 1980s was followed through with global action, much more effectively than the IPCC’s climate change efforts, sadly. The range of peak population is from 2070 through roughly 2100 and from 9.7 billion to 11 billion, depending on which demographic projections you consider most reasonable. With slowing population growth comes slowing increase in aviation demand.

But that’s challenged too. While my initial projection of COVID-19 impact was that it was a substantive discontinuity in demand for aviation, the second-order effects include significant economic impacts on emerging nations that are unequally felt by women, have left children without schooling, and are likely to impact educational trends for girls. This could easily upset the apple cart of slowing population growth. That’s the downside, and it’s too early too tell what will happen in that regard. In the near term, the just rich enough to fly segment will be flying less due to economic impacts and the current bout of higher inflation is going to impact aviation rebounds as well.

There’s also the question of business travel. Road warrior consultants — as I used to be — are mostly a thing of the past. Clients always complained about travel and living expenses, and for the past two years they received services without them. They aren’t going to return to paying them. That’s at minimum 20% of passenger aviation, and there is the collateral of air miles from those jobs that led to a lot of personal travel, something I enjoyed in the past. It’s unclear how this will play out.

In the longer term, the negative externalities of aviation will be priced and refueling will occur with low-carbon alternatives, instead of having fuel that’s barely taxed in many jurisdictions. Whether it’s carbon prices on fossil fuel-derived Jet A-1, more expensive SAF biofuels, or initial high capital costs of electric airplanes, aviation passenger kilometer or freight ton kilometer prices will rise. Classical economics gets a lot of things wrong, but the basics of increased prices suppressing demand isn’t one of them, outside of weird luxury good cases where higher prices increase purchases. My projection has electric regional aviation being cost competitive in the second half of this decade due to decreased operation and maintenance costs, but long-haul aviation won’t be cheaper than today’s flying until the second half of the century.

The discussion with Suen was nuanced and interesting. Her take was that 20-year growth was more likely to be below the 4% range projections by Boeing and Airbus, but that more growth than my flat projection was likely. I’m looking forward to data from the next couple of years to calibrate my initial guesstimate of recovery, but when I republish it, I’ll increase the rate of growth a bit, but add in the increases in efficiency. After all, my projection was of billions of barrels of oil or equivalent energy, not flights per year or revenue passenger kilometers (RPKs), key metrics in Suen’s former work and the passenger aviation industry.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy