Electrified Regional Air Mobility Will Be Disruptive & Mature Rapidly In Coming Years

Support CleanTechnica's work through a Substack subscription or on Stripe.

As one of the excellent conversations I had this week, I spent 90 minutes recording a podcast with Kevin Antcliff, aerospace engineer, formerly of NASA and now with Xwing (watch this space for the podcast). Antcliff was the coordinator and lead author of NASA’s excellent report on electric regional air mobility (RAM), where the essential ‘electric’ is inexplicably silent in the acronym. ERAM, however, sounds like a backward horse, and RAM is the commonly used acronym, so I’ll live with it.

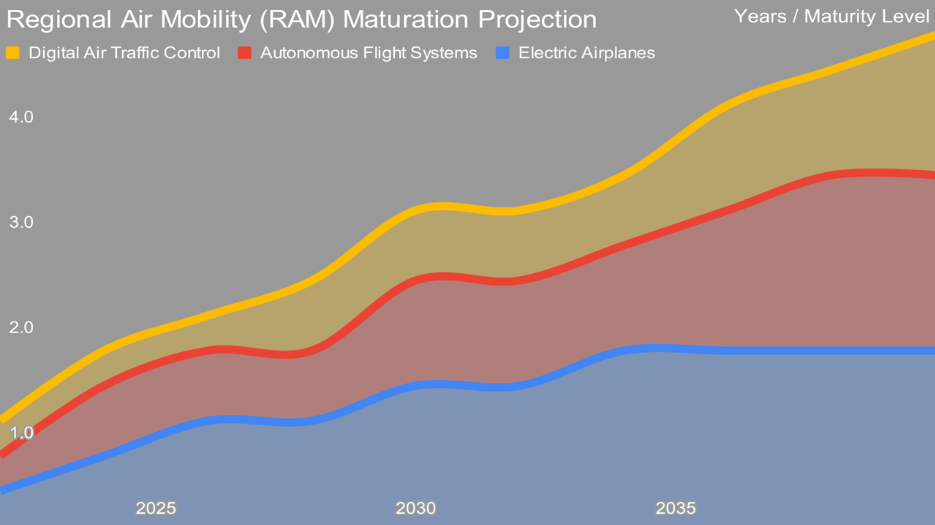

As part of that discussion, we articulated a general idea that there were 4 areas of maturation of aviation over the coming years. They were battery energy density, commercialized electric cargo and passenger airplanes, autonomous flight systems, and digital air traffic control. I realized that it was reasonable to create a projection of maturation of regional air mobility as a discussion point and to spark insights from the aerospace community on things I’m currently unaware of.

One of those factors, battery energy density, was fit for purpose for smaller conventional take-off and landing air planes suitable for regional air mobility today, and so I subsumed it in the electric airplanes factor for simplicity. As I’ve published elsewhere, electrification will win in aviation, and it will start with smaller planes and work its way up.

A commercial electric fixed-wing conventional take-off and landing airplane already exists, the Pipistrel Velis Electro. It’s an EASA-certified two-seater targeted at flight training schools. The EASA-certified part is key. That’s the European Union Aviation Safety Agency, the EU equivalent of the US Federal Aviation Administration (FAA). The certification of commercially available aircraft is taken very seriously by these organizations, and the certifications are strongly aligned, meaning that an aircraft certified under one system is recognized under the other. Many others are in development, with the Heart Aerospace ES-19, Electron Aviation Electron 5, Eviation Alice, and Bye Aerospace Electric eFlyer in various stages. (Note: I’ve communicated, often at length, with the principals of all of these companies except Eviation, and expect I’ll get around to them soon.)

Certification of electric airplanes under EASA/FAA is a process with a few things which multiply its duration and reduce its certainty. Heart Aerospace founder Anders Forslund is laser-focused on minimizing certification risk and duration by putting all of the novel components in the nacelles of a 4-motored (not engine), very standard-bodied airplane that looks like it could have been made by any of the big aerospace firms. Electron and Bye are following in Pipistrel’s footsteps, with Electron having an edge with dual-motors, and both having pre-cursor smaller flying experimental aircraft. Once novelty goes away, however, certification for conventional fixed-wing electric airplanes should be faster and less expensive than for internal combustion planes, as a major portion of certification is n x n testing of all moving components that could fail. As electric airplane drivetrains are radically simpler than internal combustion engines, pitch, and gearing systems, certification is somewhat hard to benchmark at present, and aerospace companies tend to hold this close to their chests.

Autonomous flight systems are also in development. A key point for these is that they are gate-to-gate systems that can handle taxiing, take-off, flying, landing, and taxiing under computer control. This is a place where a lot of competition exists, but a lot of the companies have military roots, which in my opinion leads to clear strategic risks for commercialization and global distribution. Investors considering these companies should consider the strategic intellectual capital and prohibited technologies distribution regulations carefully. Antcliff has moved from NASA to Xwing to be the product lead, engaging with customers and helping the product meet or exceed their needs. Others include Reliable Robotics, Kef Robotics, Forward Robotics, and most of the UAV manufacturers. A lot of people are working to be the brains of aircraft, but just as with electric airplanes, certification for use, especially out of line-of-sight, is critical.

Certification of autonomous flight systems are another level of challenge. I spoke to Grant Canary of DroneSeed last year about his heavy-lift seedling planting drone swarms, and the certification process for them. His model is five, 8-foot diameter, 100+ pound drones operating semi-autonomously with two operators. But they are doing this far from humans in burnt out areas, not over schools and roads. The drones are allowed to fly out of line of sight of the two operators, but follow prescribed routes laid out in software during planning. By the standards of flying, near-to-the-ground 100-pound drones in the wilderness is very low risk and ‘easy’ to certify, but at one point 46 FAA staff were on calls with Canary’s team as they figured out who needed to engage with what things to get certification done.

In other words, while a lot of flying is easier to automate than driving a Tesla through a busy intersection with pedestrians and bicyclists, getting an actual aircraft certified to fly a couple of hundred miles is a very different business. Right now, Xwing is flying with an observer pilot in the cockpit, with the plane operating under autonomous control, and a ground control station similar to the US military drone stations. It’s going to be a long time before humans are out of the loop, and I expect the certification process to take years.

And digital air traffic control systems are going to take even longer in certification than autonomous systems for individual aircraft. The concept is that flight control computers watch everything in the sky with radar, everything in the sky is communicating digitally with the the flight control computers providing updates on bearing, velocity, altitude, and control requests, and the flight control computers are sending waypoints in 3-dimensional space for routes that the aircraft are expected to follow, including landing paths down to the runways.

This is a vastly complex and high-risk space, and certification will take a long time. Further, airframes last decades, and as I’ve pointed out elsewhere, they are going to persist on SAF biofuels. While every aerospace startup I’ve spoken with are going to integrate autonomous sensor sets and provisions for autonomous control in their airframes to future proof them, many older airframes aren’t built to accommodate autonomous control systems and interfaces to digital traffic control, so for an extended period of time, digital air traffic control systems will overlap with current human ones. Ceding control completely to computers, even with extensive human oversight, is going to take a couple of decades.

Maturity models are usually articulated in five steps or so, but there are usually multiple factors and varying degrees of maturity of those factors. As such, I’ve created a 1-5 scale for each of the three factors, averaged them and made them additive to provide a rough idea of maturity as time goes buy out of a scale of 1-5.

As the previous discussion suggests, undergoing certification will be lengthy for autonomous systems, and lengthier still for digital air traffic control. They will lag the development of electric airplanes flown by humans talking to air traffic controllers.

That’s not an inhibitor for the start of the transformation of the market, however. Only commercial electric airplanes suitable for short-haul passenger and cargoes are necessary to start exploiting new business models in regional air mobility due to the vastly different economies provided by electric drivetrains.

Electron Aviation, for example, sees that a 4-seater, one-pilot plane can become the workhorse of a regional short-haul leisure and business travel on-demand flight service in the second half of this decade, with planes coming to a small airport near customers, who are delivered by electric Ubers at either end. The economics work out with electric airplanes where they don’t with current internal combustion planes.

For the aerospace community engaged in and following regional air mobility, the actually disruptive portion of aviation — Jetson’s evtols have no market worth the name, as I pointed out last year in my assessment of ‘urban’ air mobility –, please reach out to me to engage around this early, draft maturity model. Let’s make it better and start tracking it. Companies engaged in the space, I’d love to talk with you.

For investors and aerospace executives, focus on regional air mobility. There are a lot of great places to invest that will start returning profits this decade, and profits for the decades to come.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy