Peak Oil & Coal Demand Means Peak Shipping Demand Too

Support CleanTechnica's work through a Substack subscription, on Patreon, or on Stripe. Help us produce all of the high-quality, original content we publish week after week despite the challenges of content-scraping AI, antisocial media, inflation, and other hurdles.

In recent months I’ve been looking at the hard-to-decarbonize segments of the transportation industry. My assertion for years has been that all ground transportation will electrify with grid- and battery-electric, that short- and medium-haul aviation would be completely viable to electrify by 2100, and that short- and medium-haul water shipping would electrify as well.

But what did that mean for long-haul aviation and shipping? My assessment in 2017 was that roughly 3-4% of the total transportation fuel cycle would not be easy to electrify, and that other fuels would be required. I recently dove deeply enough into the former to make a projection of aviation refueling through 2100, one which makes it clear, at least to me, that hydrogen has no place, biofuels will be used extensively through 2060, but that the entire segment will be approaching 100% battery-electric by 2100.

I’ve been starting to assess shipping more directly in recent months. I wasn’t nearly as rapturous about Maersk’s methanol-ship investment as most other commenters appeared to be, pointing out that sufficient green methanol was being acquired to fuel one of the eight dual-fuel ships for half of a single journey per year, and that methanol would cost at least four times as much per journey as a fuel. And this week I looked at the fantasies that hydrogen advocates have of shipping hydrogen in tankers between sun-kissed poor nations and energy-intensive rich ones, finding that the delivered hydrogen would cost five times as much as delivered LNG in the absolute best possible scenario, making it economically non-viable compared to obvious alternatives such as HVDC.

But this triggered many questions, of course. For example, how much shipping is bound up in fossil fuels and commodities which are going to diminish in the future? And while everything must decarbonize in order to address climate change, there are no biofuels, synthetic fuels, or batteries that will ever be as cheap as readily available fossil fuels. As a result, transportation costs for the harder to electrify segments will increase until and if batteries develop to the energy density and price ratios necessary to shift to electric, and we have $20 per MWh renewable electricity widely available.

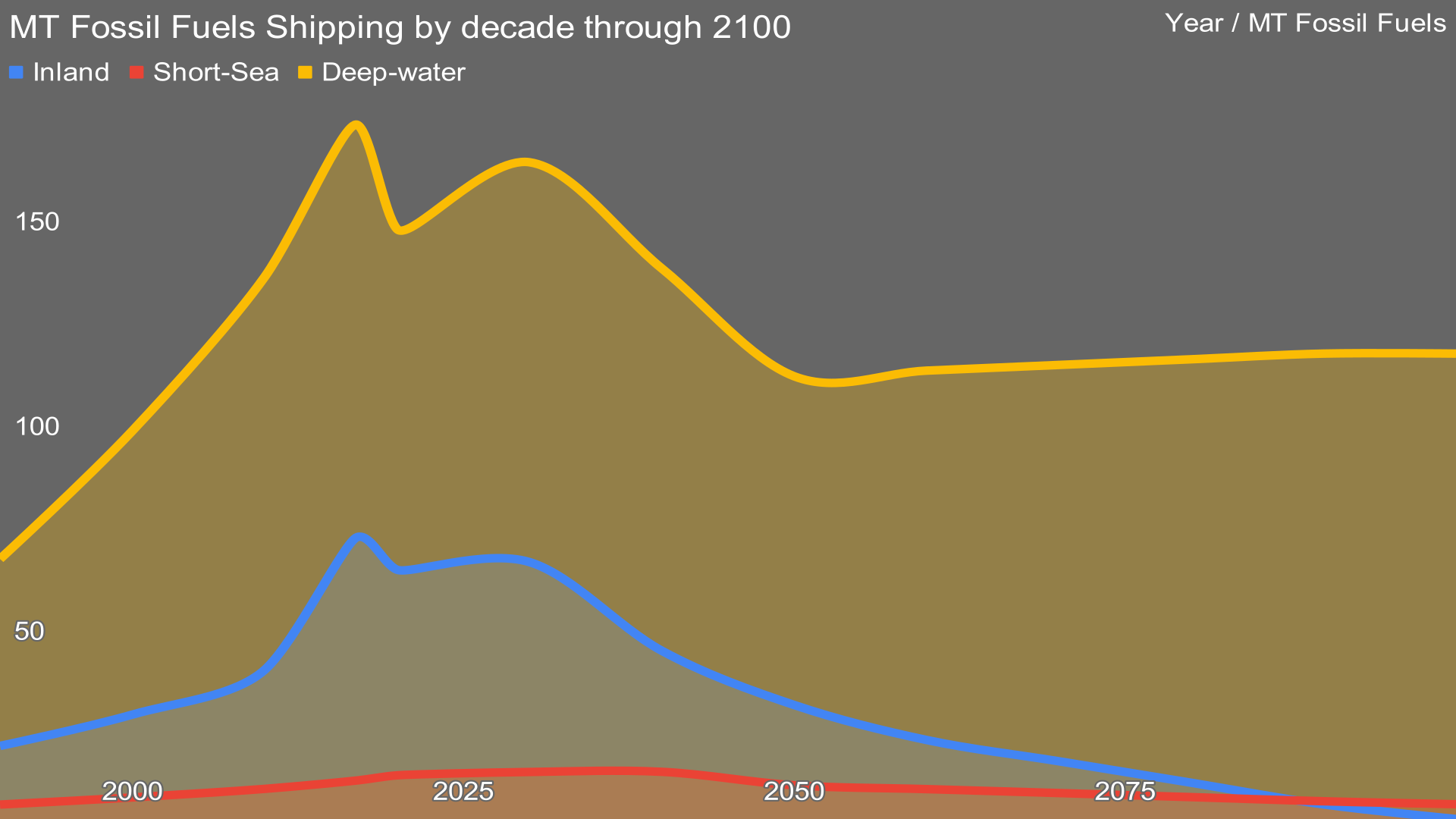

As with aviation, I have a heterodox projection of shipping. While many are excited by straight line projections from the past, I’m asserting that the world is unlikely to see a return to pre-COVID-19 levels of shipping, projecting a minor peak in roughly 2030, and then a decline before it flattens out again. As always with my projections, the explicit proviso: this is an expert opinion projecting one scenario, not a crystal ball vision which is guaranteed to come true. The error bars on this projection are large. That said, I’m comfortable that it’s more accurate than most of the projections I’ve looked at. And, as always, I welcome challenges and questions.

There are a few things to call out from this.

First, an absurd portion of the shipping industry is shipping crude oil, petroleum products including diesel, LNG, and coal. As of 2017, coal shipping was 1,200 mtons by itself. Oil, petroleum, and gas were another 3,100 mtons. Almost 40% of total shipping in 2017 was for fossil fuels. This entire segment of global shipping is going to go almost completely away, it’s just a question of when, and it’s not going to be replaced by shipping hydrogen. There will be shipping of biofuels of various types, in my opinion, through the end of the century for hard-to-electrify segments including long-haul aviation and shipping, so as oil and gas diminish, processed biofuels will take over a subset of the shipping market, but at nowhere near the volumes seen today.

With peak coal demand having been seen in 2013 globally, albeit with growth regions in Asia, and the heavy development of renewables in major coal importing countries such as China, the global coal export market will be in steep decline for the next three decades.

With peak oil demand, projected as coming at the end of this decade by McKinsey, Equinor, and others, global crude and petroleum product shipping will start to decline as well.

With global LNG shipping being a relatively minor component of the space, under 50 mtons, LNG shipping is already facing economic headwinds — barring blips like Q4 2021 — and LNG’s main use as a fuel for generating electricity will also increasingly be displaced by renewable generation, so even if LNG does increase its annual mtons, it will not change the trajectory of the curve.

The next category of main bulks to consider is iron ore, which accounted for almost 1,500 mtons in 2017, another 14% of global shipping. Once again, my projection for steel manufacturing is heterodox, as I project that the major source of steel for much of the century will be scrapping fossil fuel infrastructure and using electric mini-mills with minimal new steel to manufacture all of the steel we need with vastly lower carbon debts. New steel from other processes, whether hydrogen or electrical reduction, will be a much lower growth area, in my opinion.

As a result, I project a diminishing demand for iron ore as well. Main bulks remains relatively flat after 2050, with additional main bulk elements increasing as coal and iron ore diminish in shipping decade by decade.

That leaves the other dry cargo category. Everything that’s shipped dry that isn’t grain, oil, or coal is in this category. That includes all electronics, appliances, cars, trucks, forestry products, secondary mining products, and the like. This is the only growth category in my opinion, and insufficient to make up for the fall-off in fossil fuels and iron ore.

There are two other factors I include in my projection: higher shipping costs and peak population.

Starting with population first, the UN is projecting peak global population by roughly 2100 of about 11 billion people, while other demographics organizations are projecting a 2070 peak with much lower numbers of people. Whichever is correct, it means a significant reduction of growth in the second half of the century, and hence projections of increased demand simply due to more people are unlikely. More of those people will be affluent and there will be significant trade, but it’s not useful to project in a straight line from the past.

The increased fuel costs are a different issue. My assumption is that we have to eliminate fossil fuels from shipping in order to address climate change, and that all future fuels until complete battery electrification with $20 / MWh renewables will be more expensive than fossil fuels that are allowed to treat the atmosphere as a sewer. Further, there is no ability to build enough carbon capture and storage to offset the use of fossil fuels, something I’ve assessed multiple times, at length, and with consistent results.

As a result, shipping costs per delivered ton will increase. Fuel costs represent 50%-60% of shipping expenses, so every fuel price increase directly impacts costs of delivery. This is not a segment where automation reducing crews will have a major impact, as the ability to assert human error is a key insurance hedge and ships have already massively automated. If fuel costs double or quadruple — as the methanol assessment referenced early shows — then costs per ton delivered face significant upward pressure.

And when the cost of bulk shipping increases, the merits of shipping more heavily processed goods with higher value per ton increases. As a result, shipping iron ore is under cost pressure as well, as are other bulk commodities. This will not upend the global supply chain, but it will alter it to more local upgrading of resources in many cases.

One part of this projection is good news, which will be explored more in a subsequent shipping refueling analysis: global emissions from shipping have likely peaked and will diminish even with the continued use of fossil fuels after 2030 or so. The other part is not as good.

Long-haul shipping mostly uses bunker fuels, which are basically better grades of asphalt, the detritus of petroleum refineries. It’s the highest CO2e-emitting form of fuel after coal, and that includes a lot of black carbon with its global warming potential (GWP) of 4,470 over 20 years, and a 100-year GWP of 1,055–2,240. It’s a heavily polluting form of transportation in terms of other pollutants as well. That means that long-haul shipping, like long-haul aviation, punches above its weight as a source of CO2e emissions. Addressing it will still be necessary.

Of course, another point on that is that my 2100 projection of refinement of crude oil puts it at roughly 5% of current global volumes, specifically for the useful industrial feedstock components we get from portions of the barrel. That means that cheap global supplies of both asphalt and bunker fuel will also be drying up, and shipping will have to refuel to something less harmful regardless.

And so that’s the projection for shipping volumes through 2100. In subsequent assessments, I’ll project fuel replacements in short-, medium-, and long-haul shipping and the CO2e emissions implications of this scenario. But a key takeaway for policy makers and investors is that shipping is not nearly as likely to be a growth industry as many projections assert. COVID-19 and the climate crisis mean the coming decades are radically different than the ones leading up to 2020. Simple projections from the past do not provide useful insights.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy