Grid Storage Winners Part 1: Assessing The Major Technologies

Support CleanTechnica's work through a Substack subscription or on Stripe.

As the grid decarbonizes and everything electrifies over the coming decades, a key part of the end game is electricity storage. However, it’s not a prerequisite to getting started, otherwise we wouldn’t have been building as much wind, solar and, in the case of China, hydroelectric generation as we have been for the past decade or two.

At present, there’s a lot more grid storage than most people realize, over 170 GW of deliverable power. Almost the entirety of it is pumped hydro storage, built mostly to give nuclear and coal plants something to do at night and the vast majority of the storage under development is also pumped hydro. We’ve been building it for a long time, with the first plant going live over a century ago. Pumped hydro storage dwarfs grid-scale lithium-ion storage, and will likely always do so. But while pumped storage hydro is a key technology, it has limitations and characteristics, which means it won’t be the only storage solution.

Based on my research, publications, work efforts, and conversations with experts around the world over the last three years, I expect three storage technologies to be the major providers of grid storage, and the rest to be also-rans. I base this, as always, on a multi-factorial assessment of the technologies.

Proviso: this is an informed opinion by someone who is professionally engaged in grid-scale storage (more on that in an upcoming piece), who has reviewed multiple technologies and studies, and who has spoken to many experts in the space, but it is still merely a professional opinion. That’s the lowest scale of the pyramid of evidence, and hence while more reliable than asking an Uber driver or a pseudonymous comment thread denizen for their opinion, it should be taken as a stake in the ground to create the basis for discussion and a better opinion.

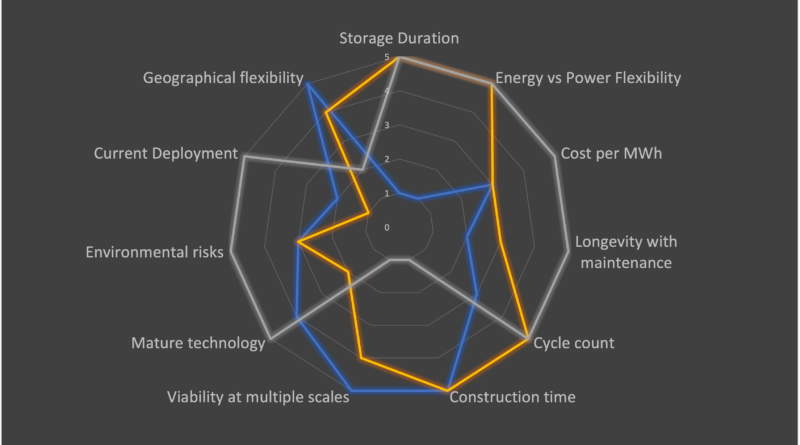

So what are the factors?

- Storage Duration – How long the form of storage can hold onto the power without significant losses, and do so economically.

- Energy vs Power Flexibility – Energy is the amount of work performed over a period of time. Power is how fast you can do the work. Lithium-ion batteries, as a primary example, have a strong and difficult to break linkage between energy and power, while other forms of generation can scale energy separately from power.

- Cost per MWh – Given reasonable assumptions, the cost to return the energy over the lifetime of the storage solution can be projected. Obviously there’s much better historical data for pumped hydro storage than for most other technologies, but the projections are reasonable. This assessment is based on both the Lazard LCOE for storage and a 2019 Pacific Northwest National Laboratory study, Energy Storage Technology and Cost Characterization Report.

- Longevity with maintenance – How long the form of storage lasts with normal maintenance cycles before it must be fully replaced.

- Cycle count – How many cycles of storage and discharge can the storage handle before it requires substantial retrofitting or replacement. This is closely correlated to the longevity metric, but is kept separate for this version of the analysis.

- Construction time – How fast is it possible to build a storage solution. This matters in part due to the cost of capital, as projects which have significant up front capital costs which also take a long time to start paying for that capital incur substantial costs to service the capital. It also matters because construction time is an indicator of higher project risks.

- Viability at multiple scales – Some storage solutions are excellent in the <100 MWh range while others must be closer to GWh range before they make sense, and some have very significant flexibility.

- Mature technology – This is a certainty factor. The more mature the technology, the greater the deployment by conservative utilities.

- Environmental risks – Nothing is perfectly clean, and grid storage is a key source of making electricity and hence all energy cleaner, but that said, some technologies come with downsides, from lithium ion’s cobalt to poorly sited pumped hydro concerns.

- Current Deployment – The more there is of something today, the more lessons learned about how to deploy and operate it quickly and safely.

- Geographical flexibility – A value proposition for storage is whether it can be deployed on the distribution side in large variance regions to provide ancillary services. Storage close to where it is needed has value.

For this analysis, each of these factors will be assessed on a 1-5 scale, with 5 being very good. As I started the discussion with pumped hydro storage, I’ll start the assessment there as well.

Pumped Hydro Storage

Pumped hydro storage may dominate grid-scale storage globally today, but it is not a perfect solution and that will limit its reach.

Let’s start with a quick definition. When I speak about this technology, I’m specifically talking about off-river, closed-loop pumped hydro storage. In this model, smaller reservoirs are placed at least 400 meters in altitude difference apart (head height). At 500 meters distance, a gigaliter of water provides a GWh of storage. The greater the head height, the more the storage due to the simple physics rules related to potential energy.

These are not on-river dams. They are not deployed on existing streams. The reservoirs are a tiny fraction of the size of hydro dams people think of. Because the reservoirs are so much smaller, they require much less concrete and they cover much less biomass which decomposes anaerobically, emitting methane and CO2, a significant concern for new on-river hydro dams. They are carbon neutral much more rapidly, do not impact fish runs, do not impact downstream silt nutrient provisioning. Because the reservoirs are small and paired, there is virtually no risk of downstream flooding in the case of dam collapses, as the at-risk reservoir can easily be emptied into the paired reservoir should a dam failure threaten. They don’t overflow because they don’t have flood waters flowing into them.

Per the Australia National University study of a couple of years ago, there are roughly 100 times the total resource capacity for this type of storage as the total global storage requirement. This is capacity that is constrained to 400 meters or more of head height, near existing transmission lines and not on protected lands, per global GIS data sets. In other words, only a fraction of the total capacity is required in order to meet our storage requirements, a seriously under-reported story.

Pumped storage hydro has the advantage that a subset of it can be devoted to deep strategic storage. Water is cheap, pumping it uphill just requires electricity and can be done in the cheapest periods with close to or below grid wholesale costs and evaporation at higher altitudes is lower. It’s pretty easy to keep a lot of it topped up to provide just-in-case levels of storage. And pumped hydro sites last a long time. Dams are 100 year+ facilities. So are the tunnels through rock. The dual-flow turbine pumps can work for decades and be replaced easily without gutting the rest of the facility.

This is one of the cheapest forms of electricity storage on a per MWh basis, something which is offset by the billion dollar capital price tag for an economically viable deployment.

And it’s the biggest form of grid storage under construction, close to 60 GW at present. 52 GW of pumped hydro projects are under development pre-construction in the USA alone.

Unsurprisingly, China is building vastly more pumped hydro storage than the rest of the world combined, just as it built as much wind and solar generation in 2020 as the rest of the world combined, has a thousand times as many electric buses on its roads as any other country, and has vastly more electrified high speed rail than any other country or continent. Also note that the Australian site under construction, Snowy 2.0, is a particularly poor example of the model. It’s entirely possible to get pumped hydro wrong.

But despite pumped hydro’s prevalence and advantages, good sites do require 400 meters of head height, so hilly or mountainous areas are required. They are typically regulated by the same federal and sub-federal bodies that regulate on-river hydroelectric, so the regulatory burden is much higher than would be expected given the characteristics. It takes years and millions of dollars to get through the accelerated regulatory process that the US Department of Energy recently introduced, as an example. It takes a decade or more to site, approve, build and commission a pumped hydro facility of this nature, equivalent to the duration of nuclear generation. It’s cheaper than nuclear, but capital costs are still $1-$3 billion for a usefully-scaled facility.

And they do have social license challenges. Hydroelectric has been under attack for the impacts it’s had on the environment for a long time, there are many now-abandoned dams in many countries and there’s a global free the rivers set of campaigns with World Wildlife Fund and Patagonia sporting goods company as obvious examples of leadership and advocacy. Many environmentalists are on principle opposed to new hydroelectric deployments due to legacy impacts, impacts which closed-loop, off-river pumped hydro storage does not have. However, convincing local people that there are few to no impacts is a lot easier said than done.

The downsides then of pumped hydro storage are geographic flexibility, viability at multiple scales, and construction time. It’s not going to be the only storage technology on the grid. My take is that this technology will be used mostly for storage of 24 hours to months, not for in day storage compared to the other technologies.

Lithium-ion Batteries

When people think batteries and grid storage these days, they automatically think lithium-ion batteries, and likely think Tesla Powerpack or Megapack if they are a bit more sophisticated.

But lithium-ion, while it gets most of the headlines when it’s deployed in California or in Australia, has significant limitations at grid scale. The big one is that due to the way they are constructed, energy and power are tightly coupled. This limits the economic value substantially and makes them unsuitable for longer duration storage. They are currently rated and used for 4-hour power movement in day, shifting mostly solar to late afternoon and early evening peak demand, and for ancillary services. They are completely fit for purpose for this, but are unlikely to be useful for more than 8 hours of storage.

They have relatively limited lifespans. While cycle times for electric vehicle lithium-ion batteries have exceeded many people’s expectations, they still see significant degradation in a decade or so. They aren’t that great on cycle count either, with the degradation linked to the number of charge and discharge cycles. Daily use means a decade of value as grid storage before complete replacement.

There are diminishing concerns about lithium-ion battery environmental impacts, but they are still present. All technologies still use cobalt, albeit in much smaller amounts, and that metal has a compromised supply chain. Lithium battery recycling is a growth industry, and electric vehicle and grid-scale quantities make it economically worthwhile compared to the tiny batteries in most of our electronic devices. There are still outstanding concerns about lithium extraction, but those too are diminishing, and may provide an alternative industry for the oil and gas regions and workers.

The good news is that lithium-ion technologies are mature and still improving, there are several vendors of them today and they are easy to deploy anywhere an electrical substation might be deployed. They also scale from very small grid requirements up to 100 MWh levels with reasonable ease.

Redox Flow Batteries

Redox flow batteries are most easily thought of as big tanks of chemicals which are pushed through a bunch of small cells in the presence or absence of electricity. The cells have ultrathin membranes between two halves of the cell, with ions passing through it from one of the chemicals in the presence of electricity to turn the low-energy chemical into a high-energy chemical.

There are multiple advantages to this approach. The first is that it separates power from energy. Make the tanks bigger and you have more energy. Put more cells between the tanks and you have more power. This is very flexible in that regard. The second is that it’s almost as easy to deploy as lithium-ion batteries. The typical chemistry of one of the tanks is bromine, a substance which is corrosive, irritating to human lungs and eyes, and in some cases toxic. This means that there are a few more hoops to jump through for placement and operation than for lithium-ion batteries, and in some cases will prevent deployment.

Many of the technologies associated with redox flow batteries are mature, some are mature with constant innovation, and others are still in development. The mechanical systems are straightforward. Tanks for liquid. Racks for the power cells hooked up with fluid, electricity and monitoring harnesses. Pumps to move liquids around. It’s a bit more complex than a Cloud server farm, but not that much. Physically, the cells are pretty much the same as proton exchange membrane (PEM) electrolysis units or fuel cells. They can be manufactured in massive numbers, mounted in pre-wired and tubed racks, and delivered to sites by the container load. So far, we’re in the realm of the very well known, manufacturable, and shippable. We start to stray somewhat with the ultrathin membrane, which has been around for a long time but which is constantly improving. It’s the most expensive single component of your average cell.

Finally there’s the actual electrolyte, one of the big points of divergence among redox flow batteries, and another source of innovation. All production redox flow batteries metals based chemistries, with vanadium and zinc as the most common forms. Bill Gates, via Energy Breakthrough Ventures, has invested in ESS, an iron-based chemistry solution, one of his investments I don’t think is misguided.

But there are innovations in the electrolyte chemistry which promise to radically change the competitiveness of this battery technology. More on that in an upcoming piece. Fair warning. It’s awesome.

Costs per MWh are trending to the same level as lithium-ion. The combination of fairly broad geographic deployment, scalable and rapid deployment, reasonable cost, energy vs power flexibility, and the serious potential for long-term storage with specific chemistries means that variants of the technology are competitive in day with lithium-ion and with pumped hydro as well. The sheer simplicity and mechanical durability of pumping water uphill is hard to beat, but in many places — more places than lithium-ion battery technology, redox flow batteries will beat it.

Also-Ran Storage Technologies

Hydrogen grid storage is currently being massively hyped as the fossil fuel industry and some countries still enamored of the slippery molecule focus on it. But its round trip efficiency of about 40% and the laws of physics mean that it is just non-competitive. Germany wants to fill salt caverns with hydrogen, and having floated across a salt lake a few hundred meters underground in a salt cavern in Germany, it’s not like they don’t exist, but it’s a significant stretch. Hydrogen loses in almost every dimension compared to the more competitive solutions. It’s telling that none of the major grid storage economic comparison bother to include hydrogen.

Compressed air storage underground in salt caverns and in porous rock formations is being studied and barely deployed. It has its enthusiasts, but it’s much more geographically limited than pumped hydro and the battery technologies. It’s vastly less deployed today despite being almost as low-tech as pumped hydro storage, which is a market indicator. It’s much less problematic in a variety of ways than hydrogen, but has serious temperature management issues. Its major advantage compared to pumped hydro storage is that no one is likely to complain about it, and that usually doesn’t make or break the case. That said, it’s the only other storage technology that gets included in major economic analyses, so it being a major player is something I don’t see, but I could be proven wrong in this regard.

Flywheels suffer from precession losses, which means that as the Earth rotates they lose a lot of power daily. Other technologies don’t even merit mentioning.

Summary Of Grid Storage

More provisos. This is a limited scale of 1-5 against a broad set of technologies and sites with widely varying characteristics. There will be many examples which contradict these broad strokes. And they are not weighted, but presented as if they all had equal weight, which is not accurate. There is much to quibble about with this assessment.

Only when all three technologies are considered do we see the full spectrum of storage requirements being met. Lithium-ion’s limitations are balanced by pumped hydro storage, just as pumped hydro storage’s challenges are balance by lithium-ion. But redox flow batteries fill up all of the gaps and more.

Which is the subject for the next assessment — given varying assessment points, maturities and the like, which technologies will have the greatest market penetration over the next 40 years. It’s somewhat crystal ball, but it’s informed and tested crystal ball. I’ve been explaining this to grid and storage experts for at least 18 months and receiving no serious pushback. So the next piece will lay it out. Stay tuned.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy