The $100,000 Mistake: Why H1-B Barriers and Policy Rollbacks Shrink America’s Future

Support CleanTechnica's work through a Substack subscription or on Stripe.

For most of the past half century, the H1-B visa program has been a conduit for global talent into the American economy. It has not been a minor contribution but a central driver of U.S. leadership in high technology. Scratch most successful firms of the last 50 years, and H1-B holders figure prominently in their intellectual capital and executive leadership.

Year after year, between 65 and 75 percent of H1-B recipients have come from India. The pattern is striking. Indian engineers, computer scientists, and mathematicians have arrived in numbers that transformed entire industries. They filled programming roles in Silicon Valley, built quantitative models on Wall Street, managed semiconductor design in Texas, and supported every stage of the IT services industry.

China has been the second largest source country, contributing engineers in chip design, material sciences, and advanced manufacturing. Canada and South Korea have provided smaller but steady flows of specialists, particularly in artificial intelligence, aerospace, and telecommunications. The Philippines has supplied healthcare professionals and technical staff. Eastern Europe has contributed in mathematics-heavy fields like cryptography and software security. The United States drew selectively and broadly from this global pool, and for decades it reinforced an innovation ecosystem that relied on constant renewal from abroad.

These workers did not settle into one narrow niche. They worked in Microsoft’s Redmond offices writing operating system code. They staffed Google’s Mountain View teams designing algorithms that underpin global search and advertising. At Tesla in Palo Alto, they worked on battery management systems and autonomous driving stacks. They joined biotech labs in Boston, research centers in Austin, and clean energy startups in Colorado and Arizona. They were critical in engineering departments of utilities modernizing their grids. They were present in almost every major R&D center run by multinationals, from automotive OEMs in Michigan to chip designers in California. Universities relied on them as postdocs and assistant professors, who in turn trained the next generation of American students. Without them, many projects would not have been possible at the speed and scale the U.S. achieved.

The $100,000 fee attached to every new H1-B application with Trump’s most recent executive order changes that foundation. Startups, which live on slim budgets and early-stage venture funding, simply cannot absorb such a surcharge. A two-person energy storage startup hoping to bring in one specialist from India would need to raise an additional $100,000 before even paying salary and benefits. Most will abandon the idea and either hire remotely abroad or leave the role vacant. Larger firms have more flexibility, but even there the calculus changes. A multinational automaker might decide to relocate a promising engineer to a German or Canadian subsidiary rather than pay $100,000 to move them to Detroit. The pipeline of foreign graduate students finishing master’s and PhD programs in the United States will find fewer opportunities to stay. They will either return home or find openings in other countries that maintain more welcoming policies.

Layered on top of this immigration barrier, the One Big Beautiful Bill strips away much of the long-term certainty created by the Inflation Reduction Act. Manufacturing credits that were designed to give a decade or more of visibility now cut off in 2027. Critical mineral credits begin phasing out, and even coal is inserted as an eligible “critical” input. Foreign entity restrictions have been tightened and paired with recapture provisions that extend for a decade, raising financing costs and legal risks for investors. Loan guarantee capacity at the Department of Energy has been rescinded. Together, these shifts make clean technology projects in the United States riskier and less attractive. Developers and manufacturers do not make multi-billion-dollar decisions without predictable policy support, and that predictability has been undercut.

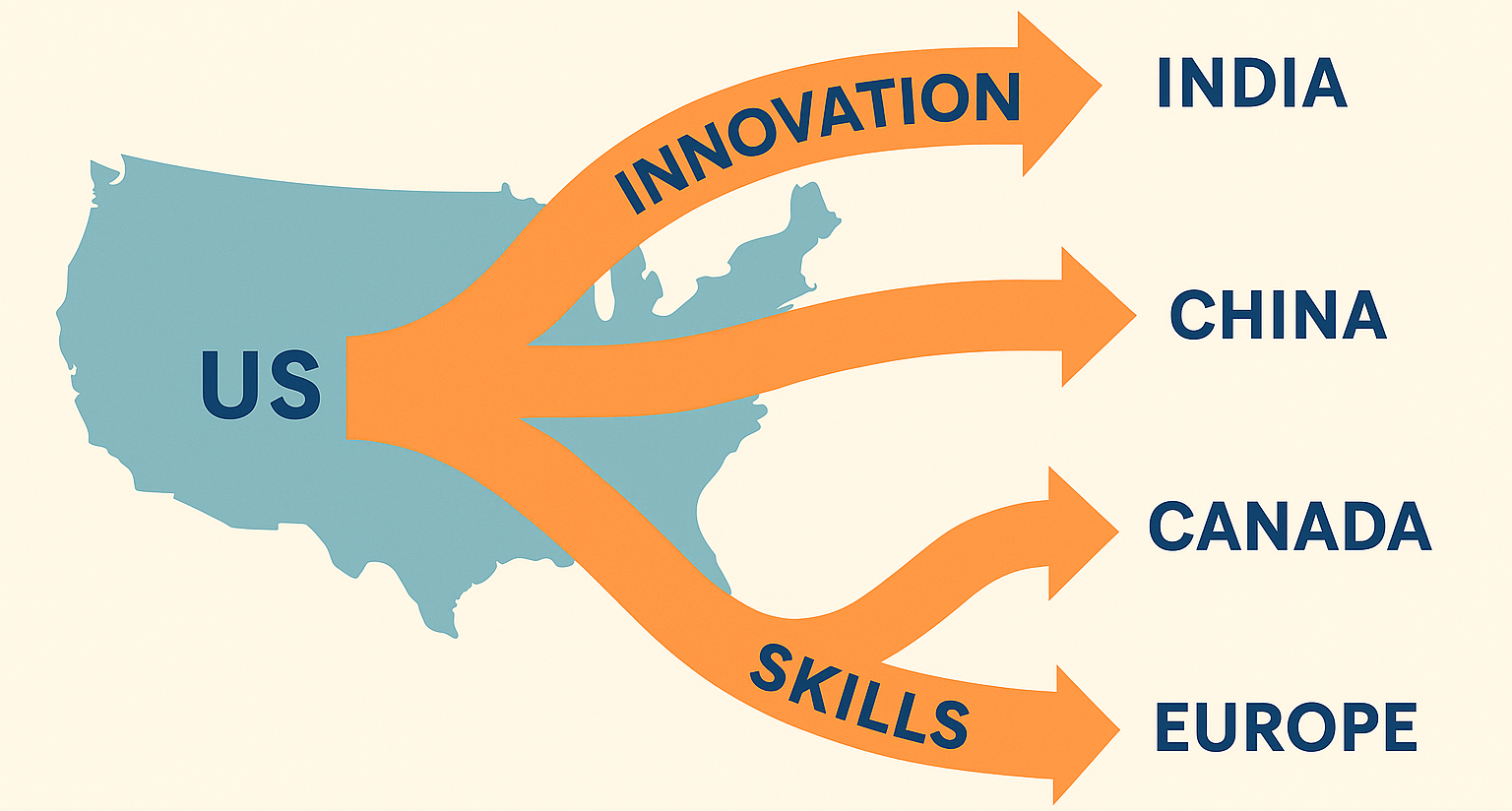

The countries that benefit most are those that were already feeding talent and supply chains into the U.S. India is first in line. With seven out of ten H1-B visas historically going to its citizens, India now retains that pool. Engineers and scientists who would have staffed U.S. offices will instead work from Bangalore or Hyderabad. Multinationals that relied on transferring staff into the U.S. will expand their Indian campuses instead. Venture capital that might have funded a Silicon Valley clean-tech startup will increasingly back Indian founders, confident the talent will remain in place. Over time, this compounds into a stronger domestic innovation ecosystem. More patents are filed in India, more startups are born there, and more global clean-tech firms build significant engineering footprints there.

China gains by virtue of its manufacturing scale. The U.S. stepping back from long-term subsidies for batteries, wind, and solar makes China’s factories more competitive. American gigafactories that were planned may stall, but Chinese exports will continue to flow. Solar supply chains that were slowly reorienting toward U.S. manufacturing under the IRA will instead remain anchored in China. The nascent battery manufacturing industry in the USA will find it very difficult to grow and for those factories that already started production, very difficult to stabilize quality. Every year of uncertainty in U.S. policy is another year of entrenchment for Chinese supply dominance.

Southeast Asia stands to pick up more of the middle links in the supply chain. Indonesia has been aggressive in attracting nickel processing and battery production, and higher U.S. visa costs and weaker incentives make that proposition more compelling for investors. Vietnam, Malaysia, and Thailand, already integrated into electronics manufacturing, will see more orders for modules, components, and subassemblies. As U.S. firms look to reduce risk and cost, they will push more of this work into these countries. Canada and Mexico, with geographic proximity and trade agreements, will also benefit as nearshore alternatives. A U.S. company that cannot afford to bring in foreign engineers may instead set up an R&D center in Toronto or Monterrey, where the visa rules are easier and the costs lower.

Artificial intelligence startups are among the most exposed to these shifts. For years they have drawn from graduate programs where the majority of students are from India, China, and other countries. Those graduates often transitioned to H1-B visas and staffed early teams in San Francisco, Boston, and New York. With a $100,000 surcharge attached to each petition, that pipeline is effectively cut off. Startups running on seed or Series A budgets cannot justify spending that much on a single hire, no matter how talented. Larger firms may still bring in a handful of foreign specialists, but the flow into the early-stage ecosystem will dry up. The result is that intellectual property that might have been created in the United States will instead be created in Bangalore, Toronto, or Berlin, where immigration pathways are open and financing confidence is higher.

The consequences ripple outward quickly. Investors back companies that can access the best people, and they will redirect capital if U.S. startups are constrained. Some American AI firms will register overseas subsidiaries to tap talent abroad, but that complicates intellectual property ownership and weakens the case for scaling in the United States. At the same time, Canada, Europe, and India will benefit from denser AI clusters, richer networks, and faster company formation. Once those ecosystems mature, they will reinforce themselves. For the U.S., the effect is a gradual erosion of relevance in a field that is central not only to economic growth but also to national security and strategic advantage.

The structural problem for the U.S. is that once these shifts occur, they are hard to reverse. Talent pools build density where they are welcomed. If India’s engineers now remain in India, they will start more companies there, join more local firms, and strengthen the ecosystem further. Manufacturing supply chains are sticky. Once a battery plant is built in Indonesia or a module assembly line is set up in Vietnam, it is not likely to move to the United States later. Investors allocate capital based on trust in long-term rules, and trust is slow to rebuild once lost. The rollback of IRA provisions signals that U.S. policy can change rapidly, and the $100,000 H1-B fee signals that the U.S. no longer values incoming talent as it once did. Together, they push money and people elsewhere.

This positions the United States for declining relevance in the industries that will define the rest of this century. Electric vehicles, batteries, wind, solar, grid storage and AI are not side projects. They are the backbone of the global energy and information transition. Countries that build and dominate them will shape trade, employment, and industrial strength for decades. By shutting down its own talent inflows and reducing its investment signals, the U.S. gives away opportunities.

Others will take them. India will grow stronger in technology and clean energy innovation. China will deepen its control of manufacturing. Both countries will end up with stronger AI ecosystems. Southeast Asia will expand its role in critical minerals and midstream processing. Canada, Mexico, and Europe will secure more design and engineering centers. The U.S. will find itself importing more technology and exporting less, a reversal of the pattern that defined its economic strength for the last century.

Reversing this trend will not be simple. Even if a future administration removes the H1-B fee and restores clean energy incentives, the intervening years will have shifted ecosystems abroad. The companies that were not formed in the U.S. will have formed elsewhere. The factories that were not built in the U.S. will already be running overseas. The trust of investors and talent will have been eroded. America can recover in part, but it will be rebuilding against competitors that have gained ground while it stepped back. The risk is not just slower growth, but a lasting decline in relevance in the technologies that matter most for the future economy. It is a choice that reshapes global competition, and one that will be very hard to undo.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy