India’s Phase II Batch 1 Winning Allocations Announced

Support CleanTechnica's work through a Substack subscription, on Patreon, or on Stripe. Help us produce all of the high-quality, original content we publish week after week despite the challenges of content-scraping AI, antisocial media, inflation, and other hurdles.

Originally published on Sustainability Outlook.

By Upendra Bhatt & Riddhi Gupta

After many months of almost no movement in the large-scale energy space, the announcement of Phase II Batch 1 winning allocations stimulated the market in February. Phase II will usher in solar infrastructure development at a rapid pace. However, the performance challenges associated with the solar industry, if unaddressed, will quickly leach enthusiasm from the market, and we may experience the same sorts of ‘lulls’ as seen by large scale wind and RPO/REC markets.

If we rewind a few months back to the end of 2013, the outlook for Phase II at the developers’ pre-bid meeting was grim – the likes of Welspun had stated that the VGF scheme didn’t ‘stack up’ financially due to the high cost of upfront capital. The Viability Gap Funding (VGF) capital subsidy could only be disbursed post commissioning whereas developers needed capital support upfront. The likes of Punj Lloyd, KVK Energies, Aditya Birla gave a lukewarm forecast for Phase II. In addition to high capital costs, unavailability of land and substation capacity, questionable quality and low capacity of the Indian solar manufacturing sector to produce affordable solar equipment, and volatile state policies were cited as key operational risks. However, this grim outlook was swiftly disproved when both Open and DCR categories were bid multiple times over.

So were these initial concerns still valid? Or had the underlying logic changed?

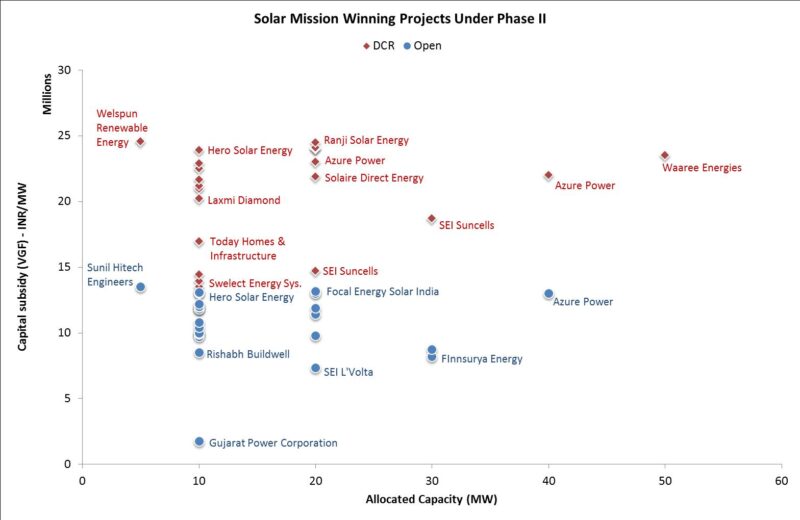

Phase II winners has seen mostly new faces compared to Phase I. Of the developers who won allocations under Phase I solar mission, only Azure Power , SEI Group, Solaire Direct have emerged strongly again under Phase II (see: full list of winners). As per the graph below, the capital subsidy requirement for DCR projects (where equipment is sourced domestically) is almost twice of projects in the ‘Open’ category (with no sourcing restrictions). This difference in capital requirement seems to be independent of the actual size of the proposed project or the location. The data is aligned with developer concerns around DCR requirements and India’s capacity to meet them in a cost friendly and resource efficient way. Indeed, enabling manufacturing capacity, putting in place technical quality and efficiency standards, and support for training programs will be required if the Indian solar manufacturing structure is to meet infrastructure demands from the National Solar Mission in a sustainable way.

Note that in the data above only, each marker represents a bid, and only bids of selected companies have been illustrated.

While most have chosen to bid multiple times using small plant sizes in order to strategically make the most of the tender process, it is interesting to note that cost dispersion of bids is significant. There is approximately Rs.10 million/MW capital requirement difference between lowest and highest bids within each category, and between categories. It is unclear if capital or location-specific costs and risks are responsible for driving this, or whether the solar market is struggling to triangulate price-points which work.

So far, the market has natural gravitated to the development of large scale solar parks and clusters. The focus on growing existing solar clusters, rather than spreading solar to new sites, makes business sense for small developers too – land parcels / surrounding wastelands exist, local village stakeholders are accustomed to solar technology, and distribution, supply & maintenance ecosystems already exist to help support a competitive bid. Further, power is injected directly into grid, for national use. Some of the hotspots under the National Solar Mission are listed below, though a range of other hotspots have emerged out of state-specific programs, large scale PPPs and private infrastructure projects.

Note that the data above only captures capacities allocated under Phase 1 and Phase 2 of the central National Solar Mission and excludes the proliferation of state-wise allocations and large solar parks which have emerged since 2011.

Of the developers we spoke to, many are still finalizing options for locations and land: Jodhpur and Jaisalmer continue to be favored in Rajasthan, while others are looking to confirm plants in Gujarat and Tamil Nadu. One MW of power typically requires 15,000m2 of land area. Land procurement currently occurs through converting wastelands / sand land into solar parks.

However, it will be interesting to monitor if Gujarat and Rajasthan continue to be the focus of development or whether the focus will shift to greenfield sites in Madhya Pradesh, Tamil Nadu and Andhra Pradesh as part of the next wave of solar clusters. The increased risk on individual developers in scoping out new sites is significant, and one can see that the impact of NSM can be broadened with proactive government support in land acquisition, community engagement and infrastructure.

Overall, large-scale solar has received a significant boost. Clean energy headlines dominated February and have spilled over to March – with the upcoming US-India Energy Dialogue and an MNRE announcement yesterday that they will invest INR 3 billion into solar pumps. On-grid rooftop solar and offshore-wind are other sectors that are gaining momentum. Clean energy appears to be retaining policy momentum as we inch forward towards elections, and we look forward to many more policy innovations to reinvigorate the sector.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy