Solar Leasing vs $0-Down Solar Loan — Scenarios In 10 States

The competitiveness of solar leasing vs a $0-down solar loan is a question that has come up many times in my mind. It’s also a topic that comes up a lot in the comments on CleanTechnica. Using EnergySage’s cool new “Instant Solar Estimate” tool, I decided to run through comparative scenarios for homes in 10 different states. The results actually surprised me quite a bit. Check them all out in this Solar Love repost:

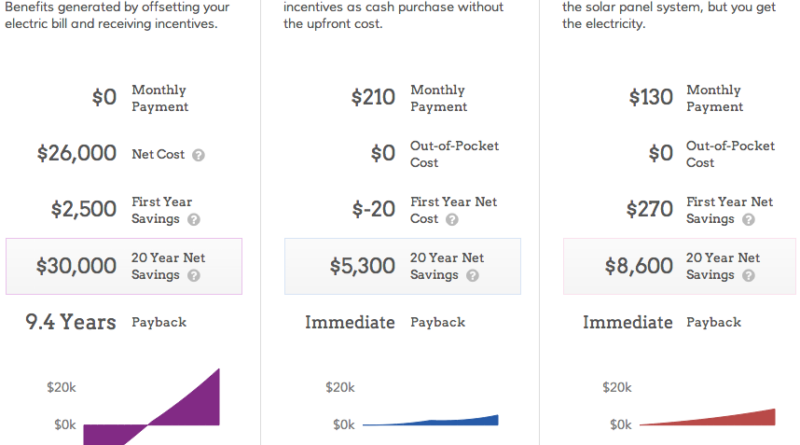

Yesterday, I wrote an article about EnergySage’s new Instant Solar Estimate tool. The tool uses proprietary market price data and “the industry’s leading tools and databases” to deliver pretty awesome solar cost and solar savings reports. One thing it does that I haven’t seen elsewhere is that it compares the financial benefit of going solar through a cash purchase, a $0-down solar loan, and a $0-down lease or PPA (where these are available). If you checked out the example screenshot shared in the article, you probably saw that solar leasing was really lame on this metric. The 20-year savings (for “Anytown, USA”) were:

- Cash purchase = $23,000

- $0-down loan = $9,900

- $0-down lease/PPA = $2,700

Yikes, $2,700 vs $9,900?

Of course, that’s just one scenario, and it seems that it’s not even for a real home. So, I decided to run some estimates for real addresses in various states where solar leasing exists in order to see what other estimates would show. I had to make a “best guess” for the electric bills, so don’t take any of this as fact (well, don’t take any such estimates as fact), but enjoy the interesting findings I came up with:

1. San Jose, California

(Address: 286 N 24th St, San Jose, CA 95116 | Monthly electric bill: $150)

In this case, solar leasing actually beat the $0-down solar loan:

2. San Diego, California

(Address: 3802 Monroe Avenue, San Diego, CA 92116 | Monthly electric bill: $50)

Here, the $0-down solar loan inches out the solar lease:

3. Phoenix, Arizona

(Address: 1019 East Hiddenview Drive, Phoenix, AZ 85048 | Monthly electric bill: $300)

The $0-down loan ends up losing you money, while the lease saves you $12,000!

4. Colorado Springs, Colorado

(Address: 7425 Julynn Road, Colorado Springs, CO 80919 | Monthly electric bill: $150)

Again, the lease wins (not counting the cash purchase, of course, which crushes it):

5. Boston, Massachusetts

(Address: 37 Edison Green, Boston, MA 02125 | Monthly electric bill: $125)

Here, the $0-down loan crushes it:

6. Baltimore, Maryland

(Address: 4408 Eldone Road, Baltimore, MD 21229 | Monthly electric bill: $125)

Neck and neck:

7. Newark, New Jersey

(Address: 541 Clinton Avenue, Newark, NJ 07108 | Monthly electric bill: $120)

$0-down solar loan is twice as good as solar lease over 20 years:

8. Tacoma, Washington

(Address: 3712 North Frace Street, Tacoma, WA 98407 | Monthly electric bill: $150)

The $0-down solar loan bombs, but the solar lease saves you money:

9. Honolulu, Hawaii

(Address: 456 Mananai Place, Honolulu, HI 96818 | Monthly electric bill: $200)

$0-down solar loan beats solar lease, but both completely crush not going solar:

10. Albany, New York

(Address: 28 Lawnridge Avenue, Albany, NY 12208 | Monthly electric bill: $200)

$0-down solar loan wins again:

Solar Leasing vs Solar Loan vs Solar Cash Conclusions

So, in my somewhat random selection of addresses, and using the best estimates for electric bills I could come up with*, it turns out that solar leasing and the $0-down solar loan option actually tied (5 to 5) for the # of times that they were the better option! Interesting, and I have to say that I wouldn’t have guessed it. Also, there was huge variation in some cases, while they were very similar in other cases.

In all the cases, you can clearly see that a cash purchase gives you the best return — that’s a given. The key questions with that option would be: 1) do you have the money for a cash purchase, and 2) where else would you potentially invest or spend that money if you didn’t use it to buy a solar system and leased or got a loan instead.

Of course, financial savings aren’t the only matter to take into consideration. Solar leasing/PPA contracts also often take care of maintenance, monitoring, and almost all the paperwork of going solar (including tax stuff). Also, the EnergySage tool assumes you can take advantage of incentives in your state. However, if your financial situation doesn’t allow that for some reason, a solar leasing/PPA company still could and could pass on those financial benefits (minus profit and company costs).

In the end, though, I think the EnergySage tool shows one thing very clearly: there can be huge financial variation using different financing options. The best thing to do is to look at all of your options, get actual quotes from different installers, and then go solar in the way that best works for you. There’s no simple solution that’s best for everyone.

*I searched out average electric bills in each city except one and then in each of those cities found homes for sale that were a similar size as the homes for which I found average electric bills.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Latest CleanTechnica.TV Video

CleanTechnica uses affiliate links. See our policy here.