Investment In Renewable Energy Set To Triple By 2030, Costs Plunging

Support CleanTechnica's work through a Substack subscription or on Stripe.

This article originally appeared on RenewEconomy.

By Sophie Vorrath

Global annual investment in renewable energy is set to grow by anywhere from two-and-a-half times to more than four-and-a-half times between now and 2030, leading to a future energy mix that would see renewables accounting for between 69–74 per cent of new power capacity added by 2030 worldwide, according to a new report from Bloomberg New Energy Finance.

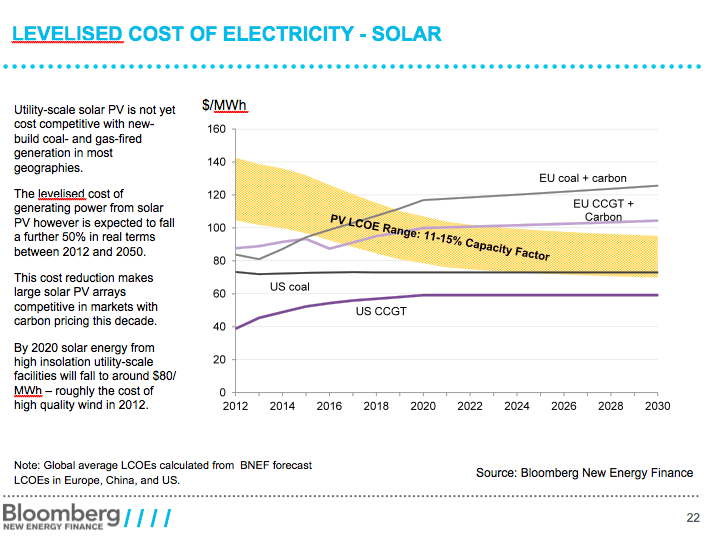

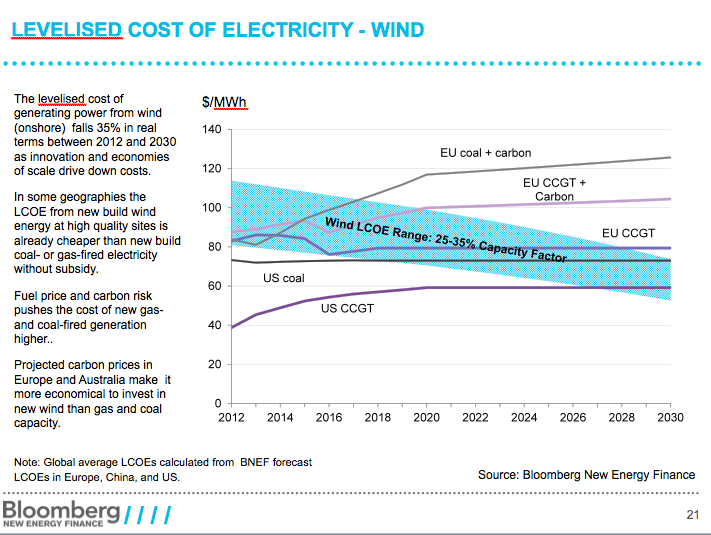

The research, published today, suggests that the most likely scenario for the renewable energy market outlook – a scenario BNEF is calling the “New Normal” – will see a jump of 230 per cent, to $630 billion per year by 2030, driven by further improvements in the cost-competitiveness of wind and solar technologies, and an increase in the roll-out of non-intermittent clean energy sources like hydro, geothermal and biomass.

The result will be renewable energy projects including wind, solar, hydro and biomass accounting for 70 per cent of new power generation capacity between 2012 and 2030, the report said. By 2030, it finds, renewables will account for half of the generation capacity worldwide, up from 28 percent last year.

“It’s a strong forecast, but it’s believable,” said Guy Turner, BNEF chief economist. “That represents compound annual growth of 6.7 percent, and many industries have grown faster than that at this stage of their development.”

The upbeat findings contrast with the picture of a market weighed down by production gluts that sent the majority of solar and wind manufacturers into unprofitable territory last year, tipping some into bankruptcy and others into record losses.

But BNEF chief executive Michael Liebreich says that, in the battle between overcapacity (as well as competition from cheap shale gas) and the falling costs of renewables and associated clean technologies, “falling costs win.”

“The apocalyptic views about what it will cost to shift the world to renewable energy simply aren’t true,” Liebreich said in an interview. “Three years ago, we thought wind and solar would be cheap as chips, and they’ve even gone below that.” What this suggests, he says, “is that we are beyond the tipping point towards a cleaner energy future.”

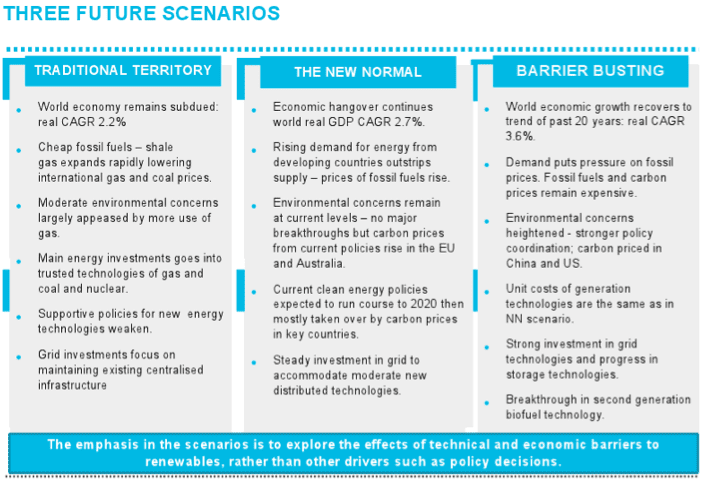

The research used BNEF’s global energy and emissions model – which factors in such variables as economic prosperity, growing demand, technology costs, policy developments, and trends in fossil fuel markets – to generate three possible future outcomes for the clean energy market: New Normal, Barrier Busting and Traditional Territory, as outlined in the chart below.

Of the three scenarios, BNEF analysts found that “New Normal” was the most likely; with an investment requirement for new clean energy assets in the year 2030 at $630 billion, more than three times the investment in the renewable energy capacity that was built in 2012.

This 2030 investment figure is 35 per cent higher than that produced in BNEF’s last global forecast a year ago, and the projection for total installed renewable energy capacity by that date is 25 per cent higher than in that previous forecast, at 3,500GW.

In the power sector, BNEF forecasts project that 70 per cent of new power generation capacity added between 2012 and 2030 will be from renewable technologies (including large hydro). Only 25 per cent will be in the form of coal, gas or oil, the remaining being nuclear.

Turner says the main driver for future growth of the renewable sector to 2030 is a shift from policy support to falling costs and natural demand. “Our work also highlights, however, the importance of planning for the integration of intermittent renewables into the grid and into power markets. This will require significant new investment in grid infrastructure, load management and storage technologies.”

The report predicts that wind and solar energy will contribute the largest shares of newly added power capacity, in terms of GW by 2030, accounting for 30 per cent and 24 per cent respectively. In terms of power produced, the share of renewables will increase from 22 per cent in 2012 to 37 per cent in 2030.

As for the other two scenarios painted in the BNEF research, according to the even more optimistic Barrier Busting assumptions, capital requirements for renewable energy could reach $880 billion by 2030 ($9.3 trillion cumulative from 2013); which would require an additional $2 trillion (22% increase) invested in supporting infrastructure, like long distance transmission systems, smart grids, storage and demand response. The Traditional Territory scenario, meanwhile, paints a more pessimistic view, with renewable energy investment requirements projected to be $470 billion by 2030 ($6.1 trillion cumulative).

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy