Support CleanTechnica's work through a Substack subscription or on Stripe.

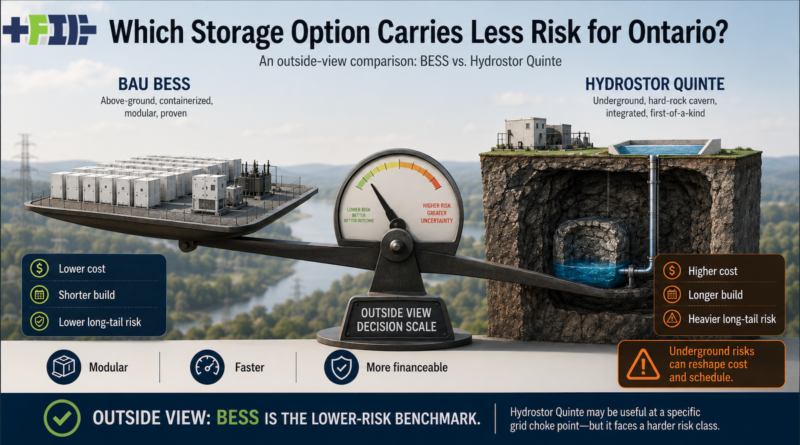

Ontario does not need another storage technology startup searching for a problem today. It needs capacity, flexibility, and reliability in specific places where the grid is constrained and where new generation and wires take years to build. That is the right way to look at Hydrostor’s proposed Quinte Energy Storage Centre. It is not just an abstract debate about compressed air versus batteries. It is a project aimed at a real grid choke point in eastern Ontario, near major transmission infrastructure, in a part of the province where dispatchable capacity and local flexibility have value.

Storage is often locational. A MWh in the wrong place is less useful than a MWh at the point where a transmission constraint, load pocket, or reliability requirement is showing up. Hydrostor’s own public framing points to eastern Ontario transmission infrastructure, including the Napanee and Lennox transformer station area, and argues that storage there could help with local and regional deliverability, capacity needs, and reliability. Storage located there can have a different value than storage added somewhere else in the province where the wires are less constrained.

There is an important fairness point. Traditional pumped hydro needs two reservoirs separated by elevation, enough land, enough water, enough geology, enough permitting room, and enough grid access. The best sites are common, but often far from where the existing grid needs storage, or they run into environmental, Indigenous, community, or land-use barriers. Eastern Ontario’s grid constraint does not come with a convenient mountain valley beside a transmission node. Hydrostor’s concept is partly an attempt to bring some of pumped hydro’s useful characteristics to a place where pumped hydro itself cannot go.

Ontario’s Independent Electricity System Operator, or IESO, is the provincial grid and market operator. It plans reliability needs, runs procurements, and contracts new resources. Quinte is being positioned for IESO’s Long Lead-Time RFP, which is aimed at resources that need more than five years of development, including hydroelectric and certain long-duration storage technologies, with successful projects potentially receiving 40-year contracts. A 40-year contract can make a high-capital infrastructure project financeable because lenders and equity investors see a long revenue runway. It can also lock ratepayers into the consequences of bad cost and performance assumptions.

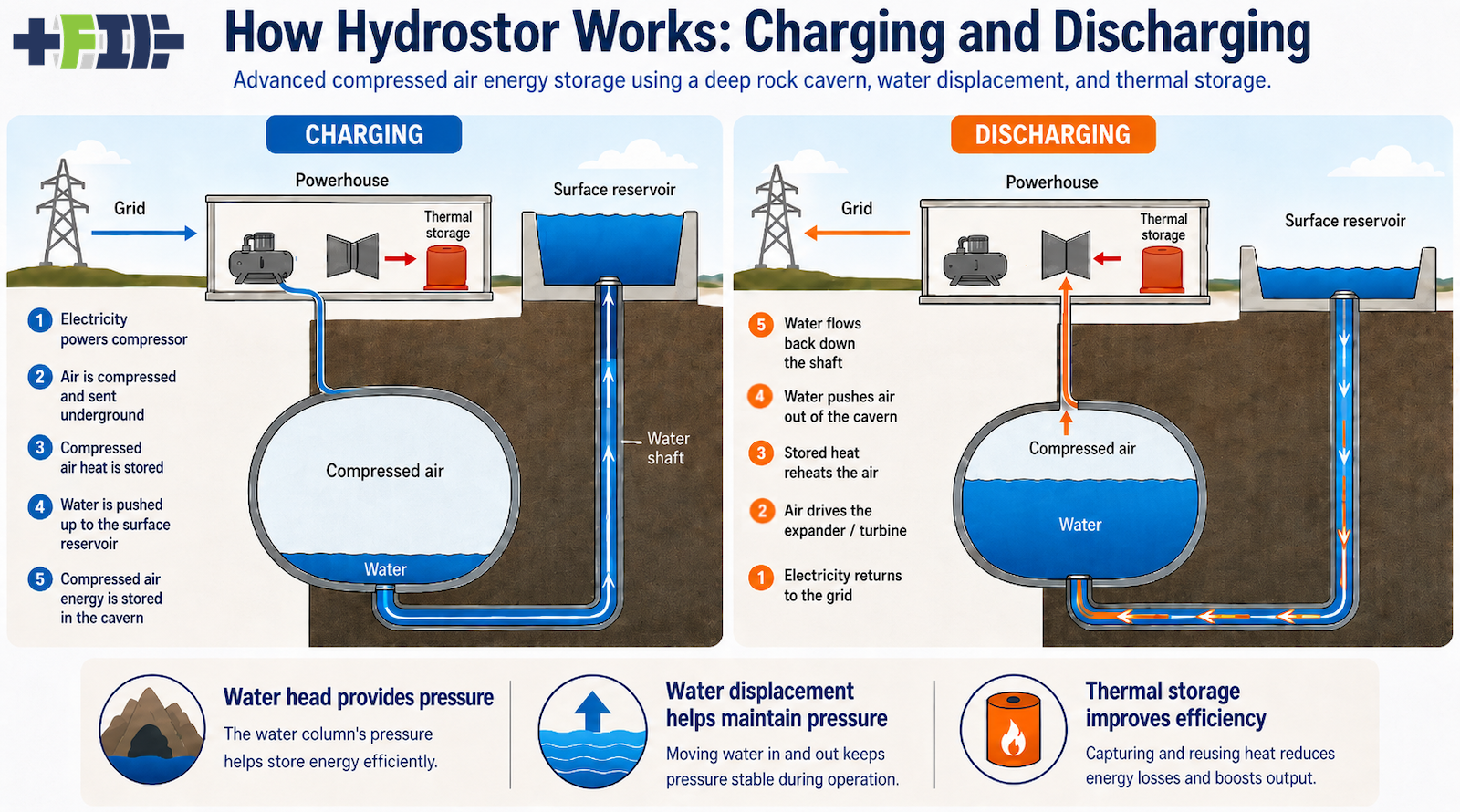

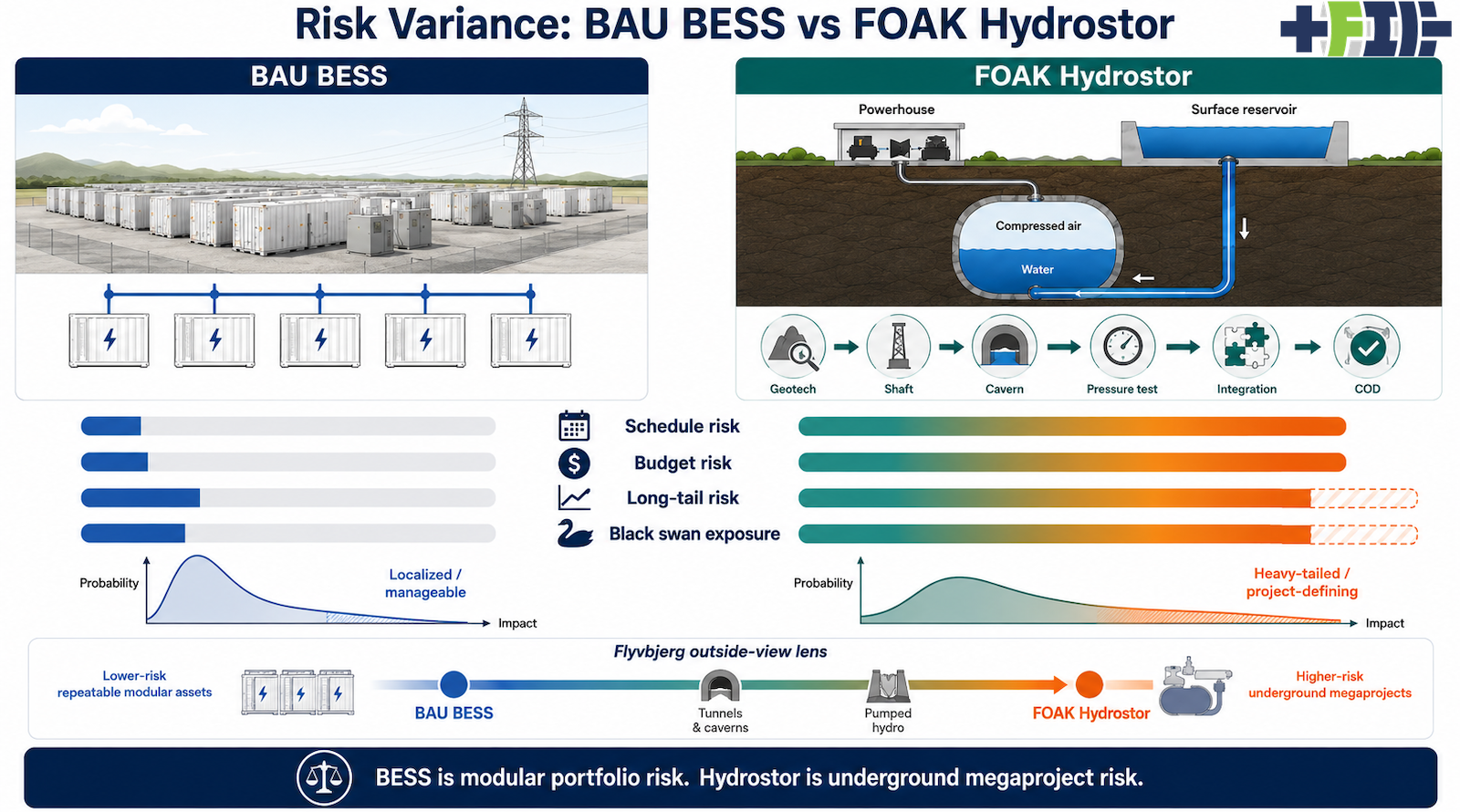

Hydrostor’s A-CAES system is not conventional compressed air energy storage of the old sort. A-CAES stands for advanced compressed air energy storage. In Hydrostor’s version, the system stores compression heat and uses water displacement in a hard-rock cavern, which separates it from older compressed air plants that burned gas to reheat expanding air. During charging, electricity drives compressors that push air underground while heat from compression is captured. During discharge, compressed air returns through the thermal system and an expander or turbine to generate electricity, while water moves back into the cavern and helps maintain pressure.

In my earlier pieces on compressed gas storage and Hydrostor’s comparison with LightSail, I argued that the physics was not the weak point. The issue was that the engineering sits between pumped hydro, compressed air, thermal storage, and underground civil works, and Quinte makes that issue concrete at 500 MW and 4 GWh scale.

One point I underlined in my earlier Hydrostor assessment is worth making explicit here: the water is not a minor accessory to the compressed air system. It is central to the design. Hydrostor’s water system is doing two jobs. The first is basic hydrostatic pressure. A water column 600 to 800 metres deep creates roughly 60 to 80 bar of pressure. That is not a small detail. It means a large part of the system’s physical logic is closer to pumped hydro than casual references to compressed air might suggest. The depth is not decorative. It is the pressure source.

The second job is pressure stabilization. In a simple compressed air vessel, pressure falls as air leaves. That makes the tail end of discharge less attractive because the turbine sees a changing pressure gradient. Hydrostor’s water displacement system acts more like a hydraulic piston. As air is released, water moves back into the cavern and helps keep pressure more stable. That improves the quality of the energy output and makes the system more useful to the grid.

This is why Hydrostor should not be dismissed as “just compressed air,” but it should also not be waved through as if it were a normal storage project. The physics is plausible. The execution is the question. Goderich, Hydrostor’s small Ontario demonstration facility, matters because it proved a version of the concept could work commercially at modest scale. But Goderich is roughly 1.75 MW and over 10 MWh, while Quinte’s first phase is proposed at 500 MW and 4 GWh. Quinte is not Goderich with a few more pipes. It is a 500 MW for eight hours infrastructure proposal.

That power and energy distinction matters. MW is the rate of delivery, like the width of the pipe. MWh is the amount of energy stored, like the size of the tank. The 4 GWh figure means the plant can deliver 500 MW for eight hours because 500 MW multiplied by eight hours equals 4,000 MWh. Because Quinte is being pitched as 500 MW for eight hours, the fair battery comparator is not a generic 4-hour battery. It is a 500 MW battery system with enough cells for 4 GWh.

The cavern volume needed for a project like this is large. Using Hydrostor’s Willow Rock project in California as the closest same-developer, same-size comparator, the implied cavern volume is about 650,000 cubic metres for 4 GWh. First-principles estimates based on 600 to 800 metres of water head point to the same range. That is a useful sanity check. The numbers are internally consistent. They also clarify the scale of the undertaking.

A 650,000 cubic metre cavern is roughly equal to a cube 87 metres on a side. It is equivalent to a 20 metre diameter tunnel more than 2 km long, or a 15 metre diameter tunnel approaching 4 km long. That is before shafts, access works, lining, water systems, pressure testing, ventilation, construction staging, spoil handling, surface works, interconnection, and commissioning. The project may be physically feasible, but it is a deep underground civil project with an energy storage plant attached.

That is where reference class forecasting becomes useful. Reference class forecasting means asking what happened to similar real-world projects, rather than relying mainly on the sponsor’s plan for this one. The inside view asks whether Hydrostor’s design can work. The outside view asks what has happened to similar projects when they moved from models, drawings, and optimistic schedules into rock, water, contractors, regulators, and commissioning. Bent Flyvbjerg’s work on megaprojects has been useful for decades because it reminds us that teams tend to believe their own project is special. Sometimes it is. Usually the reference class still wins.

For Quinte, the right reference class is not batteries. It is not even generic energy storage. It is underground caverns, tunnels, mines, shafts, pumped storage underground works, deep civil infrastructure, pressure-tested subsurface systems, and geotechnical projects where the full truth is discovered only after excavation starts. Geotechnical risk is the risk that the rock, faults, fractures, groundwater, stress, or support requirements are different from the model used to price and schedule the project. Surface projects reveal most of their conditions before construction. Underground projects reveal many of their conditions during construction, when changes are expensive.

That does not mean Hydrostor is impossible or even inappropriate. It means tidy cost and schedule claims should be treated with care. The main risks are not that air cannot be compressed, water cannot move, or turbines cannot spin. The main risks are that the integrated system has to work at 500 MW and 4 GWh scale, inside a purpose-built pressure-cycled hard-rock cavern, in a real project delivery environment.

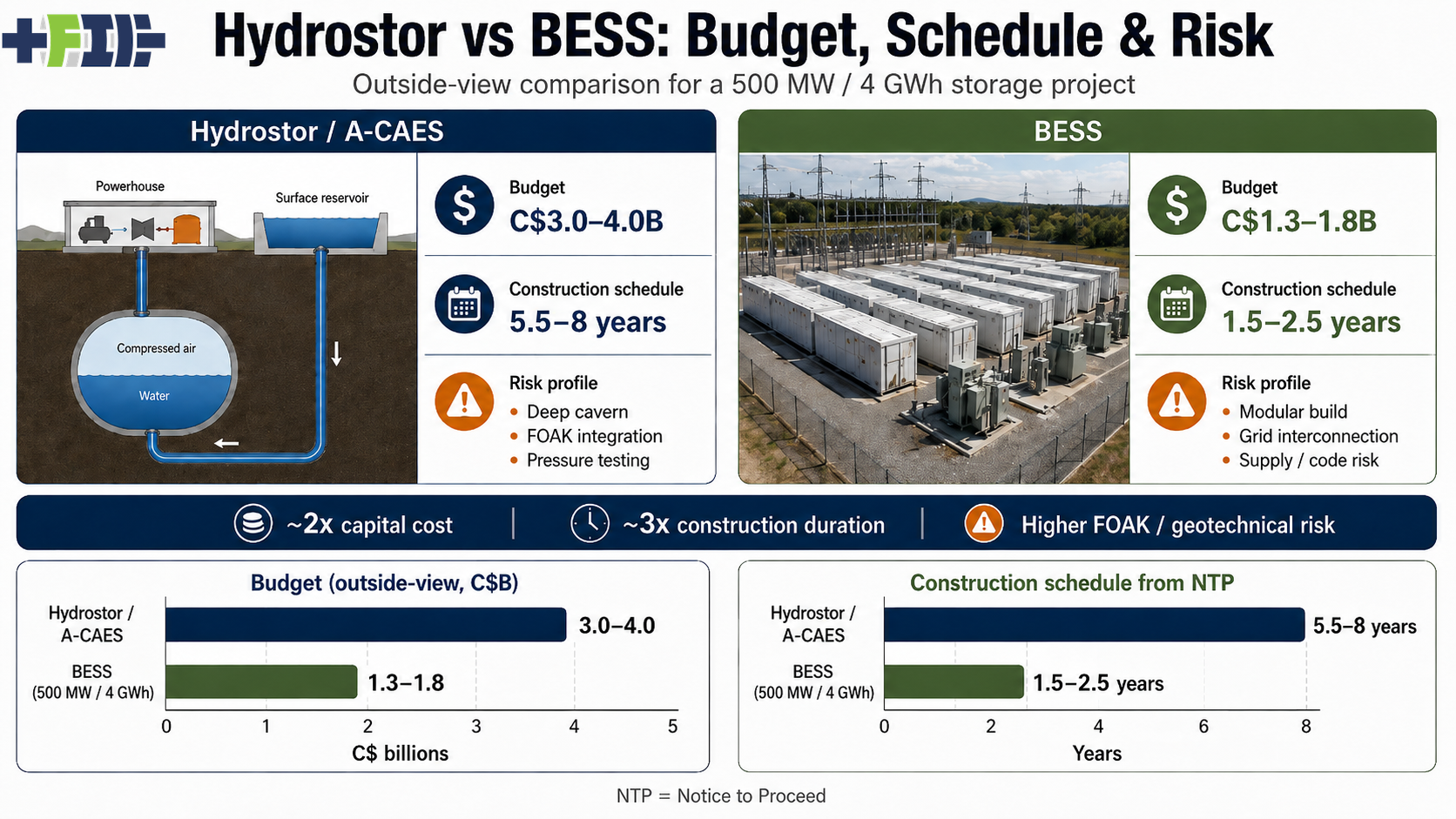

Using an outside-view planning estimate, Quinte’s first phase looks like a C$3.0 billion to C$4.0 billion construction project, with C$3.5 billion or more as a serious planning case. That is not Hydrostor’s published number. Hydrostor has not published a Quinte construction cost that I have been able to find. It is an external estimate built from comparators: Hydrostor’s Willow Rock materials, the US Department of Energy conditional loan guarantee for Willow Rock, public reporting on Silver City in Australia, underground pumped hydro projects, hard-rock civil works, and the scale of the cavern package.

Willow Rock is the most direct anchor. It is also a 500 MW and 4 GWh Hydrostor project. Public material around Willow Rock has pointed to construction costs around US$1.5 billion, and the US Department of Energy conditional loan guarantee has been up to US$1.76 billion including financing-related elements. Converted into Canadian dollars, that is already in the low C$2 billion range before a stronger reference class adjustment. The gap between that low C$2 billion anchor and a C$3.0 billion to C$4.0 billion outside-view estimate is the allowance for first-of-a-kind delivery, Ontario execution, underground contingency, owner’s costs, pressure-system validation, and the fact that the closest comparator has not yet been completed. Willow Rock is a starting point, not proof that Quinte can be built on the same number.

Silver City in Australia is a useful but lower-bound comparison because it is smaller and benefits from mine-site context. Public figures put it at 200 MW and 1.6 GWh. Scaling that toward Quinte’s 4 GWh provides one anchor, but it does not remove the Ontario hard-rock cavern problem. Underground pumped hydro projects such as Nant de Drance in Switzerland and Snowy 2.0 in Australia are not technology twins, but they are reference-class cousins because they involve deep civil works, shafts, tunnels, underground caverns, and long commissioning paths.

By contrast, a 500 MW and 4 GWh lithium-ion BESS built in North America today likely falls in the C$1.3 billion to C$1.8 billion range, with C$1.5 billion to C$1.7 billion as a reasonable central estimate. BESS means battery energy storage system, usually rows of containerized battery units, inverters, transformers, controls, fire systems, and grid connection equipment installed on a surface site. BloombergNEF’s recent turnkey BESS cost estimates, North American installed-cost data, and current market pricing all point to a much lower capital cost than a first-of-a-kind underground compressed air project.

Ontario will not get Chinese BESS pricing because it has North American labour, grid-code, fire-code, transformer, insurance, EPC, warranty, and interconnection realities. Even on a North American basis, however, a BESS looks roughly half the capital cost of the Hydrostor outside-view estimate.

The Ontario comparator is Oneida, Canada’s largest operating grid-scale battery. It is a 250 MW and 1 GWh project in Haldimand County, Ontario, led by Northland Power with Indigenous and infrastructure partners, which entered commercial operation in 2025. It came in around C$700 million according to public reporting from Northland Power. Scaling that mechanically to 4 GWh gives C$2.8 billion. But that is a weak current cost anchor because Oneida was procured and built through an earlier, higher battery cost cycle. Battery systems have dropped sharply in cost since then, and 8-hour systems spread power-related costs over more stored energy. Inverters, controls, civil works, security, some interconnection costs, and owner’s costs do not double just because the battery duration doubles from four hours to eight.

Round-trip efficiency makes the cost comparison harder for Hydrostor. Hydrostor has publicly used figures around 60% to 65% round-trip efficiency for A-CAES, while lithium-ion BESS systems are commonly in the 85% to 95% range at the DC battery level and lower but still strong at the full AC-to-AC system level after inverters, auxiliaries, thermal management, and transformers. In practical terms, if the grid needs 4 GWh delivered, a 90% efficient BESS needs about 4.4 GWh of charging energy, while a 65% efficient A-CAES plant needs about 6.2 GWh. At 60%, it needs about 6.7 GWh. That extra 1.8 to 2.3 GWh of input energy per full cycle is not fatal if the plant is soaking up low-value surplus electricity that would otherwise be curtailed, but it is a real operating-cost penalty whenever charging energy has market value. It also weakens Hydrostor’s cost case because the project already carries higher up-front capital cost, longer construction duration, and higher delivery risk than a comparable BESS. Lower efficiency means Hydrostor has to win on location, contract value, grid services, asset life, or non-battery risk reduction, not just on bulk storage economics.

Eight-hour and 4 GWh-scale batteries are no longer outside the normal range of BESS planning. In the UK, NatPower’s Teesside GigaPark has been announced as a privately financed 1 GW battery project, initially operating at four hours of storage, or 4 GWh, with the potential to expand to eight hours and 8 GWh. It has a 1 GW grid connection agreement and is targeting grid connection by 2028. Statera Energy has also secured approval for a 4 GWh, eight-hour BESS in the UK, eligible for the country’s long-duration energy storage cap-and-floor regime. In Australia, RWE’s Limondale project was selected in New South Wales’ first long-duration storage tender as an eight-hour lithium-ion BESS, at 50+ MW and 400+ MWh. Italy’s first MACSE storage auction contracted 10 GWh of utility-scale battery storage for 2028 delivery, including about 1.3 GWh of batteries with durations of eight hours or more. The point is not that every grid should use eight-hour lithium-ion batteries for every long-duration need. It is that 4 GWh and eight-hour BESS systems have moved from edge case to procurement reality. A 500 MW / 4 GWh BESS is now a serious comparator for Quinte, not a straw man.

Schedule is just as important as capital cost. Hydrostor’s public Quinte schedule points to operations in 2033 or 2034. That is already later than earlier local discussion that pointed toward 2030. The current schedule is more realistic, but it remains an inside-view schedule. A reference class view for deep underground civil works suggests 5.5 to 8 years from full notice to proceed to commercial operation. If Quinte is still in development in 2026 and has to move through procurement, permitting, financing, final design, geotechnical confirmation, excavation, pressure testing, integration, and commissioning, a central outside-view commercial operation window of 2035 to 2038 is more defensible.

That timing distinction matters. A project can be “in development” for years before notice to proceed. Notice to proceed is the point where permits, financing, contracts, engineering, and major procurement are sufficiently aligned for the main construction program to begin. Hydrostor’s 2033 or 2034 public schedule is a from-today claim. The 5.5 to 8 year estimate is a from-notice-to-proceed construction and commissioning view. By contrast, a similarly scaled BESS is a 1.5 to 2.5 year physical construction project once the site, permits, major equipment, and interconnection path are ready, even though interconnection, permitting, transformers, and procurement can still stretch the full development timeline.

The reason is simple. BESS is modular. Containers, inverters, transformers, cabling, controls, fire systems, fencing, gravel pads, and substations can be installed in parallel. A 4 GWh BESS is large, but it is made of many repeatable blocks. Hydrostor’s cavern is not repeatable in the same way. The project has to discover the rock, excavate it, support it, line or seal it as required, connect shafts and water systems, pressure test it, then integrate air, water, heat, and turbomachinery into one plant.

Risk is not one thing. Hydrostor’s risk is not the same as BESS risk, and BESS risk is not zero. Hydrostor has deep cavern risk, geotechnical discovery risk, first-of-a-kind integration risk, pressure testing risk, contractor risk allocation risk, and financing risk. BESS has interconnection risk, fire and code approval risk, transformer supply risk, degradation and augmentation risk, and procurement or tariff exposure. BESS is mature, but not magic. It is just mature in a very different way.

The shape of the risk is the difference. Hydrostor has low science risk but high underground civil execution and integration risk. BESS has mature technology risk, with supply-chain, interconnection, permitting, and lifecycle risk. One class tends to fail or succeed through subsurface execution and commissioning. The other tends to succeed or struggle through procurement, grid connection, and operational management. Those are not equal risk classes.

Hydrostor’s strongest counterargument is lifetime. A cavern-based storage asset could plausibly have a much longer physical life than a lithium-ion BESS. A 40 or 50 year asset can justify higher up-front capital if it delivers reliable capacity for decades and avoids multiple replacement cycles. That matters in an Ontario procurement context if contracts are long and if the province values durable non-lithium storage at a constrained node.

But lifetime only helps after successful completion. It does not erase first-of-a-kind completion risk. A BESS may require augmentation and likely major replacement over a 40 or 50 year comparison period, but replacement can occur in phases while the land, grid connection, transformers, controls, permits, roads, and much of the balance of plant remain in place. If a C$1.5 billion to C$1.7 billion BESS needed major augmentation and eventual replacement, the lifecycle math would still have to be compared against a C$3.0 billion to C$4.0 billion underground project with higher delivery risk. Hydrostor’s long-life case depends on the first plant arriving close to budget, close to schedule, and close to its performance claims.

That brings the analysis back to Ontario. The question is not whether batteries are cheaper in the abstract. They are. The question is whether Ontario is buying something from Hydrostor that batteries cannot provide at that specific location, and how much extra that is worth. If the province needs long-duration storage at that grid choke point, if traditional pumped hydro cannot be built there, if the project provides valuable grid services, if the contract structure can support long-term infrastructure financing, and if the geotechnical evidence is strong, Hydrostor deserves serious consideration.

But serious consideration is not the same as accepting brochure economics. Ontario should specify the grid service, duration, location, reliability value, fire-risk value, and premium over modular alternatives. If the answer is 8-hour storage, BESS can do that. If the answer is 40-year physical life, then the cost and risk of reaching year one matter. If the answer is avoiding lithium-ion fire risk, that has value, but it needs to be priced against construction and schedule risk.

For Quinte to be bankable on responsible public-interest terms, the IESO contract would need to be strong enough to support financing without quietly moving excess risk to ratepayers. The geotechnical work would need to be independently reviewed. The cavern design, excavation plan, lining or sealing strategy, water management approach, and pressure-testing regime would need to be credible. The EPC or EPCM structure would need to make clear who owns cost growth, delay, performance shortfalls, and commissioning problems. The project would benefit from evidence from Willow Rock or Silver City moving into construction and operation before Ontario assumes that full-scale A-CAES is a normal infrastructure class.

Hydrostor’s Quinte proposal sits in the awkward middle between useful ambition and difficult reference class. It is aimed at a real problem in a place where traditional pumped hydro is not available. Its core idea is more sophisticated than conventional compressed air storage, and its water displacement system addresses a real technical weakness in simple compressed air systems. But reference class forecasting pulls the project out of the technology brochure and into the world of underground megaprojects.

That is consistent with my earlier view of Hydrostor: interesting, physically plausible, and more sophisticated than most compressed air storage pitches, but still fighting a difficult reference class. Ontario should value the grid location, the lack of conventional pumped hydro options, and the potential long-duration contribution. It should also demand the discipline that underground first-of-a-kind infrastructure requires.

Quinte may be useful. It may even be worth paying more for. But it should be judged as a deep underground infrastructure megaproject competing against modular battery storage, not as a generic long-duration storage technology looking for applause.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica's Comment Policy