Solar’s Insane Cost Drop

Originally published on Renew Economy.

We’ve seen and published many dramatic graphs about the fall in solar, such as this one tracing the fall over the past 30 years and this from Citigroup, but the following graph from investment bank Sanford Bernstein is quite stunning – not just for its simplicity but because it draws attention to the potential impact of solar to the $5 trillion global energy market.

As you can see, the cost of solar panels has come from – quite literally – off the charts less than a decade ago to a point where Bernstein says solar PV is now cheaper than oil and Asian LNG (liquefied natural gas). It does its calculations on an MMBTU basis. MMBTU is the standard unit of measure for liquid fuels, often referred to as one million British thermal units.

“For these (developing Asian economies) solar is just cheap, clean, convenient, reliable energy. And since it is a technology, it will get even cheaper over time,” Bernstein writes in a newly released report.

“Fossil fuel extraction costs will keep rising. There is a massive global market for cheap energy and that market is oblivious to policy changes” in China, Japan, the EU or the US, it writes.

This has potentially massive impacts for the oil, gas and LNG markets, and therefor the massive investments in the LNG plants in Queensland, Australia, where tens of billions of dollars have been invested by Australian and international energy majors on the assumption that the demand, and the price, of LNG will rise ever upwards.

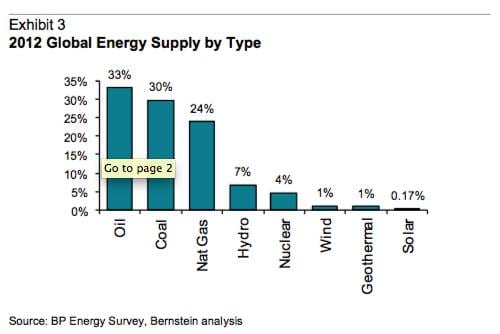

As Bernstein notes in its report, the share of solar PV in the global energy market is currently so small (see graph to the right) that “the idea that oil and gas is the “loser” in this formulation is laughable … in 2014.”

As Bernstein notes in its report, the share of solar PV in the global energy market is currently so small (see graph to the right) that “the idea that oil and gas is the “loser” in this formulation is laughable … in 2014.”

But that’s not the case a decade hence. Solar is already eating away at the margins of oil and gas demand. Bernstein says the adoption of solar in off-grid areas in developing markets means less kerosene and diesel demand. The adoption of solar in the Middle East means less oil demand. The adoption of solar in China and developed Asia means less LNG demand. And distributed solar in the US, Europe and Australia means less natural gas demand.

And then Bernstein drops this bombshell – while solar has a fractional share of the market now, within one decade, solar PV (plus battery storage) may have such a share of the market that it becomes a trigger for energy price deflation, with huge consequences for the massive fossil fuel industry that relies on continued growth.

“The behavior from here seems clear: the solar industry will expand. Retaliatory steps from distribution utilities will increase the market for cost-effective battery storage. This becomes – initially – a secondary market for battery technologies being developed for the auto sector. A failed battery technology in the auto sector (too hot, too heavy, too rigid a form factor) might well be perfect for the home energy storage market…. with an addressable end market of 2 billion backyards.

“And for some years, that will be the extent of the effect. We have previously calculated how large the solar sector would need to be in order to become a material share of incremental energy supply each year and therefore begin to displace high-cost oil and gas supply and start to depress prices.

“We estimate that the solar industry would need to be an order of magnitude larger than it is today to have this kind of impact. At the point where solar is displacing a material share of incremental oil and gas supply, global energy deflation would become inevitable: technology (with a falling cost structure) would be driving prices in the energy space. But even on an aggressive view, this could take the better part of a decade.”

But, the Bernstein analysts say, the risks are that they are being too conservative. The big oil and gas producers, and the investors that control the flow of capital, may not wait until energy prices do actually deflate, they will likely change their behaviour well before than in anticipation that it will happen.

“If the downward sloping forward curve is ever accepted as permanent, rational behavior from energy producers will guarantee it is so. Sitting on oil and gas reserves for the benefit of generations yet to come ceases to be a rational strategy if that reserve represents a depreciating rather than an appreciating asset.”

This, Bernstein says, is the hidden flaw with the idea that solar is “too small to matter”. Ultimately, it says, what may kill the energy market for equity investors is not the fact that renewable technology and battery storage will turn into behemoths, but the realisation of that future as inevitable.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Latest CleanTechnica.TV Video

CleanTechnica uses affiliate links. See our policy here.