49% Of New US Electricity Capacity Is From Solar, Q1 Record (Report)

A couple of big solar records were set in Q1 2013 in the US. For one, 49% of all new US electricity generation capacity came form solar, the most ever for a first quarter. Secondly, 723 MW of solar power capacity were installed and put online, again a Q1 record for the US. Let’s run down a bunch more of the facts and highlights from the Solar Energy Industries Association’s (SEIA) and GTM Research’s latest US Solar Market Insight® quarterly report.

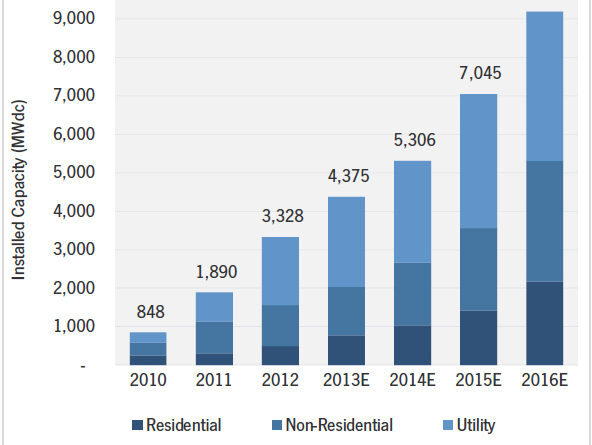

US Solar Power Installation Capacity

As you can see in the chart above, Q1 2013 was just the 4th best quarter to date for solar installation capacity. However, for various reasons, Q4 is generally the best quarter of the year and Q1 the worst, so that’s actually quite a good ranking.

Also, utility-scale projects really throw quarter-by-quarter comparisons out of wack. As SEIA writes: “As always, it is important to take the utility market out of the equation when seeking meaningful conclusions from the comparison of quarterly installation figures; the utility market is simply too volatile and dependent on individual project timelines. In that context, Q1 was quite strong in the residential market (53% year-over-year growth) and weak in the non-residential market (down 20% year-over-year). This reflects our general outlook for the year; we expect significantly stronger growth in the residential market than the non-residential market. Utility installations were down substantially from Q4 2012, but up more than 130% relative to Q1 2012. This market generally experiences a boom in the fourth quarter and we expect the same pattern to hold in 2013.”

Anyway, if you’re a fan of numbers, all in all, Q1 2013 was down 45% from Q4 2012 but up 33% from Q1 2013.

Remember that this growth is projected to continue throughout the year, with solar projected to become the #2 source of new power capacity in the US in 2013 as a whole, only behind natural gas.

In total, at the end of Q1, US solar power installation capacity stood at 7,962 MW.

Distributed Solar Revolution

SEIA highlighted utility-scale solar’s role in 2012’s record-crushing year, but it also went on to note that the future is going to be about distributed (residential and commercial) solar.

Residential solar was 53% higher in Q1 2013 than in Q1 2012, and it was actually 11% higher than Q4 2012.

Here’s more from SEIA on the revolution: “We expect that the next four years will be marked by a new solar revolution in the U.S., this time driven by the distributed generation (DG) market. Whereas residential and commercial solar markets have historically been effectively capped by the availability of state- and utility-level incentives, solar has now become cost-effective in some markets with only the federal investment tax credit (ITC), accelerated depreciation and net metering. This report highlights this shift in California, where a meaningful number of installations have been completed without California Solar Initiative incentives, which have been that market’s main driver since 2007.”

The solar revolution has been one of the concepts that seems to get people most excited, and seems to most influence the sharing of solar stories on CleanTechnica and elsewhere. It is an exciting concept. And we are clearly living in an exciting time.

Regarding California, let’s also remember that nearly 100% of new electricity generation capacity in the state in the second half of 2013 is projected to come from solar power. That’s outstanding, amazing. The revolution really seems to be starting.

Challenges To Distributed Solar

However, SEIA aptly notes that there are some huge obstacles that could slow the revolution, considerably even, and citizen as well as business and political support is needed in order to make sure they don’t (or do to as little a degree as possible). Again, from SEIA:

With the ITC currently in place through the end of 2016 and PV system prices continuing to fall each quarter, the DG market’s prospects have never been better. However, with this opportunity comes a new set of risks:

- Net metering and the debate over how to value distributed generation: As the penetration of DG has grown, a number of utilities have sought to revise, cap, or remove net metering. This issue will play out differently across geographies but will have major implications everywhere.

- Changing rate structures: Utility tariff structures can similarly impact the cost-effectiveness of solar. Changes in the details of these structures (such as how to incorporate time-of-use pricing and fixed vs. volumetric charges) can easily push solar into, or out of, economic viability. While net metering is currently a more public battleground, we anticipate that rate structures will soon follow behind.

- The availability and cost of project finance: We estimate that the distributed generation market will require $48.5 billion of investment during the 2013-2017 period, which far exceeds all project finance provided to date. Market participants and advocates are working to secure new sources of capital, adapting financing models from other industries (REITs, master limited partnerships), retail capital sources (crowdfunding, community solar), and new investors in existing structures (corporate and utility tax equity). Still, project finance could serve as a significant bottleneck to growth over the next four years.

In the absence of these limiting factors, residential and commercial PV could grow exponentially through 2016.

US Solar Power Prices

One of my favorite things about this report is the pricing information that is provided. In Q1, the “blended” installed price of solar actually went up a bit (compared to Q4 2012). However, the price for each segment of the market went down. Confused? Again, the reason is simply that utility-scale solar (which is cheaper) accounted for a much smaller percentage of solar power installations.

The blended price (or “national capacity-weighted average system price”) went up from $3.04 per watt to $3.37 per watt. However, as you can see above, everything else is down, and compared to Q1 2012, prices are way down. From SEIA:

-

From Q1 2012 to Q1 2013, residential system prices fell 15.8% percent, from $5.86/W to $4.93/W. Quarter-over-quarter, installed prices declined by 1.9% percent. Installed prices came down in most major residential markets, including California, Arizona, and New Jersey. It was not uncommon for final installed prices to be in the $4.00/W range.

-

Non-residential system prices fell 15.6% percent year-over-year, from $4.64/W to $3.92/W, while installed prices decreased by 8.1% quarter-over-quarter. Significant quarter-over-quarter price declines came in smaller state markets with relatively high installation prices in Q4 2012. Most notably, Texas dropped from $6.36/W to $3.23/W during that period, while major market states like New Jersey and Massachusetts saw their installed prices stay flat.

-

Utility system prices once again declined quarter-over-quarter and year-over-year, down from $2.90/W in Q1 2012 and $2.27/W in Q4 2012 to settle at $2.14/W in Q1 2013. This relatively small price decline is linked to the disproportionate number of smaller projects coming on-line in Q1 2013 than in Q4 2012.

Naturally, across the US, which is larger geographically than Europe, and very diverse in its solar policies and market saturation, prices varied considerably. “Common residential system prices ranged from less than $3.00/W to almost $8.00/W. Non-residential prices were as low as $2.50/W and as high as $8.00/W.”

Regarding specific solar PV components, above is a graph on key price trends.

“Pricing for polysilicon and PV components remained soft in Q1 2013 due to the persistence of the global oversupply environment that the industry has faced since early 2011. Blended polysilicon prices declined by 13% to $17/kg, while blended module average selling prices (ASPs) for Q1 2013 were down to $0.64/W, 6% below Q4 2012 levels of $0.68/W. Cells were the sole component to experience a pricing uptick in the first quarter, but as global component supply and demand begin to come back into balance, the steady downward pricing trend of the past few years could slow or stop in coming quarters.”

More Solar Facts

Here are some more facts from SEIA:

-

The non-residential market shrank 20% on both a quarterly and annual basis, which reflects slow demand across a number of major markets

-

The utility market more than doubled year-over-year, with 24 utility PV projects completed in Q1 2013

Concentrating Solar Power (CSP and CPV)

-

6 MWac of concentrating solar capacity was installed, including SunPower’s first commercial deployment of its C7 low-concentrating PV tracker technology; cumulative operating CSP and CPV capacity in the U.S. now stands at 552 MWac

-

2013 will see the most CSP commissioning in history, with more than 900 MWac expected to come on-line

-

BrightSource Energy’s Ivanpah project is on track to be completed in 2013; as of now, all units are more than 85% complete

-

Abengoa Solar and BrightSource energy signed a partnership for the construction and operation of the 500 MWac Palen Solar project

A lot more information is available in SEIA’s US Solar Market Insight® Executive Summary, and surely the report itself. Dig in if you want to learn even more.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Latest CleanTechnica.TV Video

CleanTechnica uses affiliate links. See our policy here.